Change your life by

managing your money better.

Subscribe to our free weekly newsletter by entering your email address below.

Subscribe to our free weekly newsletter by entering your email address below.

Are your investments in the right accounts? Are you just getting started and need a simple solution that lets you start maximizing your army of dollar bills? We explain the three types of investment accounts, which assets should live where to maximize tax efficiency, and why where you invest can be just as important as what you invest in.

We break down the surprising asset location strategy that could keep more of your growth tax-free and share why you want to make every dollar count. Plus, we share a one-fund solution for those just getting started that provides broad diversification, automatic rebalancing, and simplicity that far outweighs constant optimization.

For more about how investing helps build financial independence, read our ultimate guide How to Invest: Complete Guide to Building Wealth. And as always, keep building towards your great big beautiful tomorrow.

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

Brian: Are your investments in the right accounts? If not, it could be costing you big time. Often times, people want to know what to invest in, but they don’t give as much thought to where those investments will be optimized. So, today we’re going to walk you through the three different types of investment accounts and how you can maximize each one for your financial future. With that, let’s jump right in.

Brian: First up, let’s talk about those tax-free accounts. Kind of our favorite child of the three. These include Roth IRAs, Roth 401(k)s, and health savings accounts. With these accounts, you contribute after-tax dollars, except for the HSAs, of course. They’re kind of unique, meaning the money going in has already been taxed. The real magic happens during the growth phase and when you make qualified withdrawals. Both are completely tax-free. You heard that right, tax-free. And because tax-free accounts have contribution limits, the space inside them is limited and highly valuable. So you want to make every dollar count. When it comes to choosing the investments for these tax-free accounts, it’s a good idea to focus on assets that have the highest long-term expected growth potential. Since no one knows what tax rates will look like in 20, 30, or even 40 years, it makes sense to protect your high growth assets from any possible future tax increases. And by sheltering these investments in a Roth, you’re maximizing the tax-free benefit of that account.

Brian: So, what are the best assets to hold in tax-free Roth accounts? The short answer, indexed equity funds. This would represent large cap, mid-cap, small cap, or even international holdings. You can access these through broad equity ETFs, or even index mutual funds. These asset classes historically have higher growth potential, making them ideal candidates for tax-free growth and compounding. The underlying principle is simple. The more an asset is expected to grow over time, the more valuable it becomes to shelter that growth inside of a Roth account because you’ll never pay taxes on those gains. Can you imagine what it’s like to be a seven-figure millionaire with no taxes due? We love sticking it to Uncle Sam legally through tax-free growth and good account structure. It’s actually highly encouraged by our government based on how they keep expanding what qualifies for these Roth accounts.

Brian: Next, we have tax-deferred accounts, which include traditional 401(k)s and traditional IRAs. Contributions are made with pre-tax dollars, giving you an immediate tax deduction. The money grows tax-deferred. No taxes on dividends, interest, or capital gains as they accumulate. However, withdrawals in retirement are going to be taxed as ordinary income. These accounts are subject to required minimum distributions, also known as RMDs. So, you’re forced to start taking money out at a certain age to avoid a penalty. The ideal investments for these type of accounts are assets that generate regular taxable income. By sheltering this income inside a tax-deferred account, you avoid annual tax drag and allow your investments to compound more effectively. The trade-off is that you eventually have to pay ordinary income taxes on these accounts as you take withdrawals, but deferring taxes for decades can result in significant long-term growth opportunities.

Brian: The optimal assets for tax-deferred accounts can include many of your more conservative holdings like your bonds, also known as fixed income, whose interest is taxed annually at ordinary income tax rates if held in a taxable brokerage account. Most of their return comes from the interest income taxed every year at those higher ordinary income tax rates. So, they’re also an ideal type of investment for these tax-deferred accounts.

Brian: The third type of account we want to cover today is your taxable brokerage account. You invest with after-tax dollars and pay taxes on dividends, interest, and capital gains each year. But taxable accounts do have some advantages. Long-term capital gains are taxed at lower rates than ordinary income. Qualified dividends from companies are also subject to lower tax rates. These accounts also provide easy liquidity and access with no contribution limits, no required minimum distributions, and no early withdrawal penalties. Assets you might want to choose for these taxable accounts include equities that will have favorable both capital gains or dividend tax rates. It’s also a good place for those liquid assets like your cash, your CDs, your treasuries, or even safe assets with tax benefits like muni bonds. This could make sense if you plan to need access to your investments for an early retirement or upcoming investment needs.

Brian: Your ideal asset location may look a little different based on your unique needs and goals. Let’s face it, personal finance is personal, but the information we’re discussing here is based on historical long-term data. And generally speaking, it’s a solid strategy to hold higher growth assets in Roth accounts, income-producing assets in tax-deferred accounts, and very tax-efficient investments and cash in brokerage accounts. That math just works. But there is a huge trade-off we can’t ignore. Complexity. A mathematically optimal strategy isn’t useful if it’s too difficult to execute. Fortunately, there are practical options to help ease the complexities or to help navigate these decisions in the just getting started years.

Brian: The first is index target retirement funds. They may not maximize every variable, but they do solve the execution part. These funds provide broad diversification, automatic rebalancing, and have a built-in glide path. For many investors, simplicity far outweighs the constant optimization. These are especially great if you have more of a desire to just do something and you can answer these two easy questions. Number one, how much can you save? And number two, when will you need these assets? If you know those two things, you can let index target retirement funds do the rest of the heavy lifting. And you can watch as your army of dollars catch traction to build past both the boiling point and then even reach critical mass, typically around the $500,000 mark.

Brian: Reach that point and you’re likely ready to graduate and to take your relationship to the next level with the Money Guy Show and Abound Wealth. A lot of what I’ve covered today is brushing up against when good simple advice starts to become unfortunately complex, as you discover the personal nature of personal finance and you’re going to quickly realize this is your first retirement and you just don’t know where your blind spots are or how to maximize all opportunities. But there is some good news is that you don’t have to have all this figured out. We have literally done this a thousand times. An advisor can design a strategy tailored to your income, your tax bracket, your timeline, and even your goals. They’ll handle asset location complexity, optimize for taxes, and ensure your portfolio stays aligned through rebalancing. You get a personalized strategy without managing it by yourself. Because ultimately, the best plan is one that lets you focus less on managing your investments and more on what truly matters to you. Own your time.

Brian: Bottom line, where you invest can be just as important as what you invest in. So, now that we’ve talked about asset location, I want you to click right here to learn more about asset allocation. And as always, keep building towards your great big beautiful tomorrow.

Free Resources

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

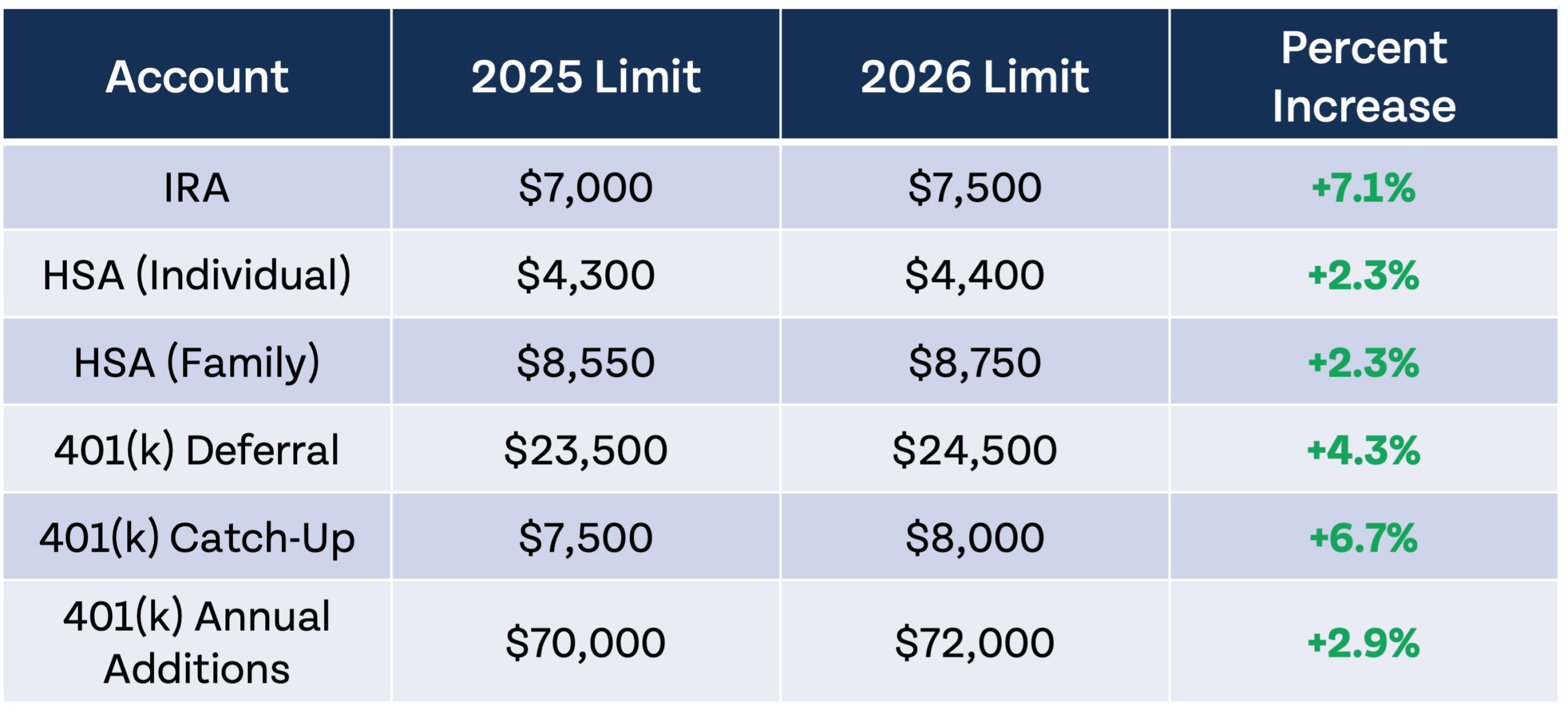

Each year, the IRS adjusts retirement account contribution limits, standard deductions, marginal tax rate brackets, and more for inflation. I’m happy to announce that it...

Articles

Over longer periods of time, index funds tend to outperform actively managed funds in most categories. Recently, total assets in index funds have surpassed the...

Articles

The S&P 500 is down nearly 15% from its highs earlier this year, inching closer to bear market territory. While it may not be wise...

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

Are you financing too much car? We break down the 20/3/8 rule, reveal which car brands pass our Money Guy test for dependability and value,...

Episodes

Jonah and Caroline earn $420,000 and built an $820,000 net worth by age 29, but they're carrying a $49,000 401(k) loan, recovering from a $75,000...

Episodes

Does the Financial Order of Operations really work in every situation? Meet FOO Following Freddie, our hypothetical case study showing how the Financial Order of...

Subscribe to our free weekly newsletter by entering your email address below.