Last Updated

March 24, 2026

Read Time

Share

Is Becoming an Entrepreneur Right For Me?

Becoming an entrepreneur is an enticing and attractive path to making a living and building wealth. The glossy brochure promises ownership of your time, full autonomy over your labor, and the possibility to grow your income to a level beyond what you could ever earn working for someone else. That isn’t a far-fetched dream for the millions of Americans that own small businesses, but a reality that they are working towards every day.

While the possibilities of entrepreneurship are exciting, there’s a reason why not everyone is cut out to work for themselves. According to Bureau of Labor Statistics data, approximately one-third of private sector businesses survive for a decade. Working for someone else is often a much safer decision that provides greater financial stability, but the spoils of entrepreneurship are too captivating for many to ignore. If you’ve caught the entrepreneurship bug and are willing to dedicate your time, energy, and brainpower towards making your dream a reality, this guide will help increase your odds of success and make the leap to business ownership with confidence.

Should I Start a Business?

Copy link to this section: Should I Start a Business?

Copied the URL to your clipboard!

At its core, starting a business is an investment in yourself. You are betting on your ideas, on your labor, and on your ability to make others see your vision. This investment is not a safe one. It may be more likely than not that it will go to $0, but the potential returns could be astronomical. If your business does survive and produce income, it may not do so for several years.

Not everyone should be an entrepreneur. You are no better or worse than someone else because you do or do not own a business. It’s a very personal decision that comes down to your own tolerance for risk, what stage of life you are at, how highly you value your autonomy at work, and whether or not you are self-motivated. If you have something you are good at, that you love to do, that is also something there is a need for and you can get paid to do, you may have something you could successfully do for a living (and be happy doing it).

Share image

Working for an employer typically provides a steady income, health insurance, retirement benefits, and a defined role. Your business could provide that for you eventually, but it will take a vast investment of your time, money, and labor – and there is no guarantee of success. Building a successful business starts with a solid foundation. Here are some signs that you may have that foundation in place.

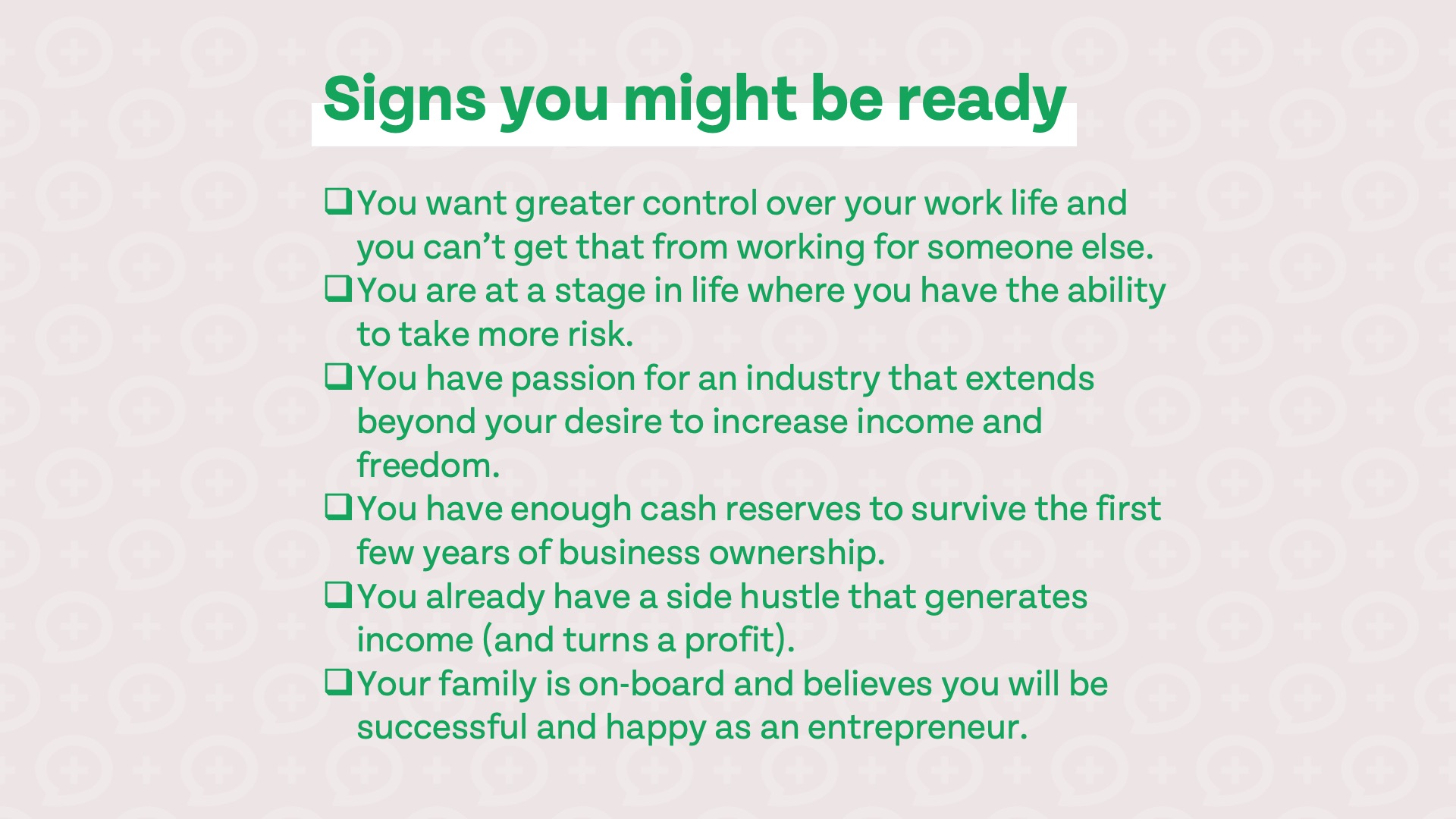

Signs you might be ready to start your own business

There are tangible and intangible signs that you are ready to start a business; let’s start with the intangible signs first:

- You strongly desire greater control and ownership over your work life, and you are unable to get that by working for someone else.

- You are at a stage in life where you have the ability to take more risk. This means other areas of your financial life wouldn’t be at risk if you pursued business ownership (i.e., you wouldn’t risk losing your home and your family would be taken care of).

- You have passion for an industry that extends beyond the desire to increase your income and freedom.

Now here are some tangible signs that you may be ready to start your own business:

- You have enough cash reserves to survive the first few years of business ownership until your business becomes profitable (or, if you are not successful, until you find a different job).

- You already have a side-hustle that generates income and dedicating more time and money towards it would allow you to grow your business.

- Your family members are on-board and believe you will be successful and happier as an entrepreneur.

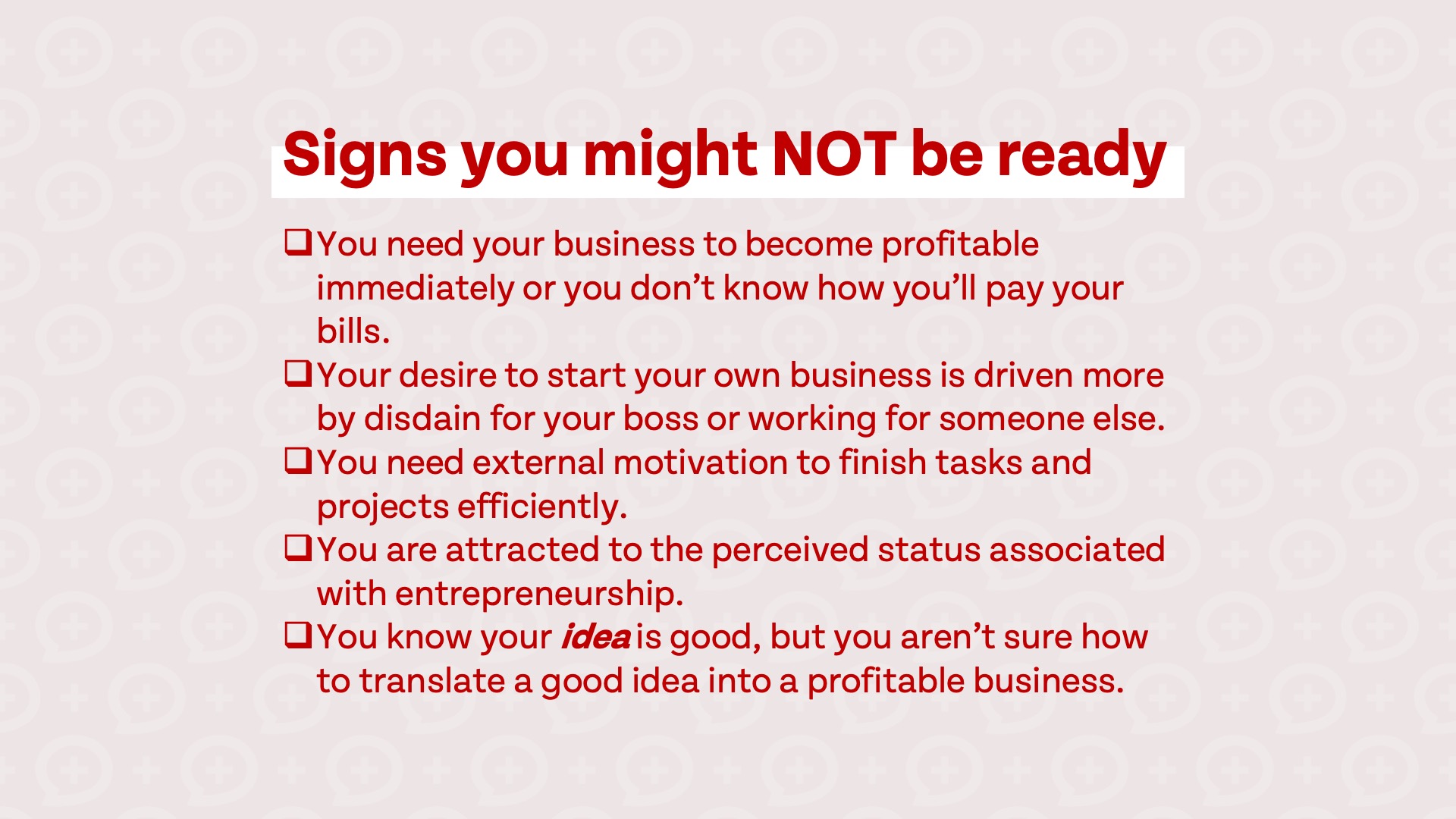

Signs you’re NOT ready

Just like there are signs you are ready to go out on your own, there are signs that it may not be the right time to start a business:

- You don’t have adequate cash savings to get you through the first few years that may not be profitable.

- Your desire to start your own business is driven more by disdain for having a boss than genuine passion for your chosen industry.

- You find you need external motivation to finish tasks and projects efficiently.

- You are attracted to the perceived status that is associated with being an entrepreneur.

- You expect to become successful quickly and are planning on living off of the business within a short period of time.

Use the scorecard below to determine if you may be ready to take the leap into entrepreneurship and quit your job!

Ready-to-Quit Scorecard

Instructions: Start at 0. Add 2 points for every check in “Signs you might be ready.” Subtract 2 points for every check in “Signs you’re NOT ready.” A score of 10+ indicates you may be ready to quit.

Share image

Share image

How Does The FOO Change When I'm Self-Employed?

Copy link to this section: How Does The FOO Change When I'm Self-Employed?

Copied the URL to your clipboard!

The Financial Order of Operations was created to work for anyone, regardless of whether you work a traditional job or own a business. However, some steps of the FOO are more important when you are an entrepreneur and some are a little bit different than they are for those with a typical job. Here is how the FOO changes, and stays the same, when you are self-employed.

Step-by-step FOO for the self-employed

Step 1 – Deductibles Covered

Covering your insurance deductibles is a must for anyone to have a solid financial foundation and it’s even more important if you are self-employed. You may have additional insurance deductibles to cover, like liability insurance and property insurance. Health insurance may be more expensive than it was when you worked for an employer and you may no longer have access to work benefits like life or disability insurance. You need to have the funds to cover your insurance deductibles before you even consider starting a business.

Step 2 – Employer Match

There are self-employed retirement plans, but you no longer have an employer to provide matching funds to your retirement. If you are self-employed, skip this step and move on to step 3.

Step 3 – High-Interest Debt

It should go without saying, but any high-interest debt should be eliminated before starting your business. If you have high-interest debt and a business, it will act as an anchor weighing you down and will make success nearly impossible. Sometimes it can make sense to use debt in your business, like to purchase a property for your office, but high-interest debt should be avoided at all costs.

Step 4 – Emergency Fund

A larger emergency fund is required if you own a business. It’s especially important to have at least two to three years of living expenses on hand when you start your business – don’t expect to be profitable on day one. Even if you own an established and profitable business, you should still maintain a larger-than-normal emergency fund to get you through any tough times. One of the biggest reasons why businesses fail is because they don’t have access to cash to keep the business running when times are bad, such as during a recession or black swan event like the pandemic.

Share image

Maintain separate emergency funds for your family and your business (to pay operating expenses, employees, buy inventory, etc.). Some industries are more recession-proof than others. If your business is seasonal, affected by the economy, or in a specialized industry, consider maintaining an even larger emergency fund.

Step 5 – Roth IRA & HSA

Roth IRAs and HSAs are great retirement savings accounts for the self-employed and this step is the same regardless of if you are self-employed or have a boss. If your income is higher than the Roth IRA limits, consider using the backdoor Roth strategy to contribute if you can. You are now the employer and have full control over your health insurance, so consider choosing an HSA-eligible plan if it makes sense for your situation.

Step 6 – Max Employer Plans → Solo 401(k) or SEP-IRA

This step is drastically different if you are self-employed. You should still maximize employer retirement accounts at this step, but since you are the employer, you have a great deal of control over which retirement plan you use and your retirement plan custodian. For those without other employees, solo 401(k) plans are generally the all-around best retirement plan for the self-employed. They have generous contribution limits and are available at low-cost providers like Fidelity, Charles Schwab, and Vanguard.

If you do have employees, there are many low-cost retirement plan options you can offer your workers and you don’t need to be a large business to have a good retirement plan.

Step 7 – Hyperaccumulation

Hyperaccumulation may look a little different if you are self-employed. Normally this step involves contributing to a taxable brokerage account to reach the 25%+ retirement savings rate and that is still the goal for entrepreneurs. However, you realistically may not reach this step in the early years of your business. For those with a successful business, it can be a better investment to put money back in the company rather than a taxable account. There’s nothing wrong with investing back in the business, but you should still be investing 25% for retirement outside of your business.

Step 8 – Prepay Future Expenses

Like Step 7, prepaying future expenses may not happen in the early years of starting a business and is more likely once you own a successful and profitable company. While the goals at this step are important, they should not be prioritized over your own financial health and the health of your company. Consider revisiting this step once your business is generating a stable amount of income.

Step 9 – Low-Interest Debt

The goal to be debt-free by retirement doesn’t change if you own a business, but business debt is a little different than debt you are personally responsible for. Prioritize your own personal debt before you begin paying down any business debt that you may have.

The Solo 401(k) advantage

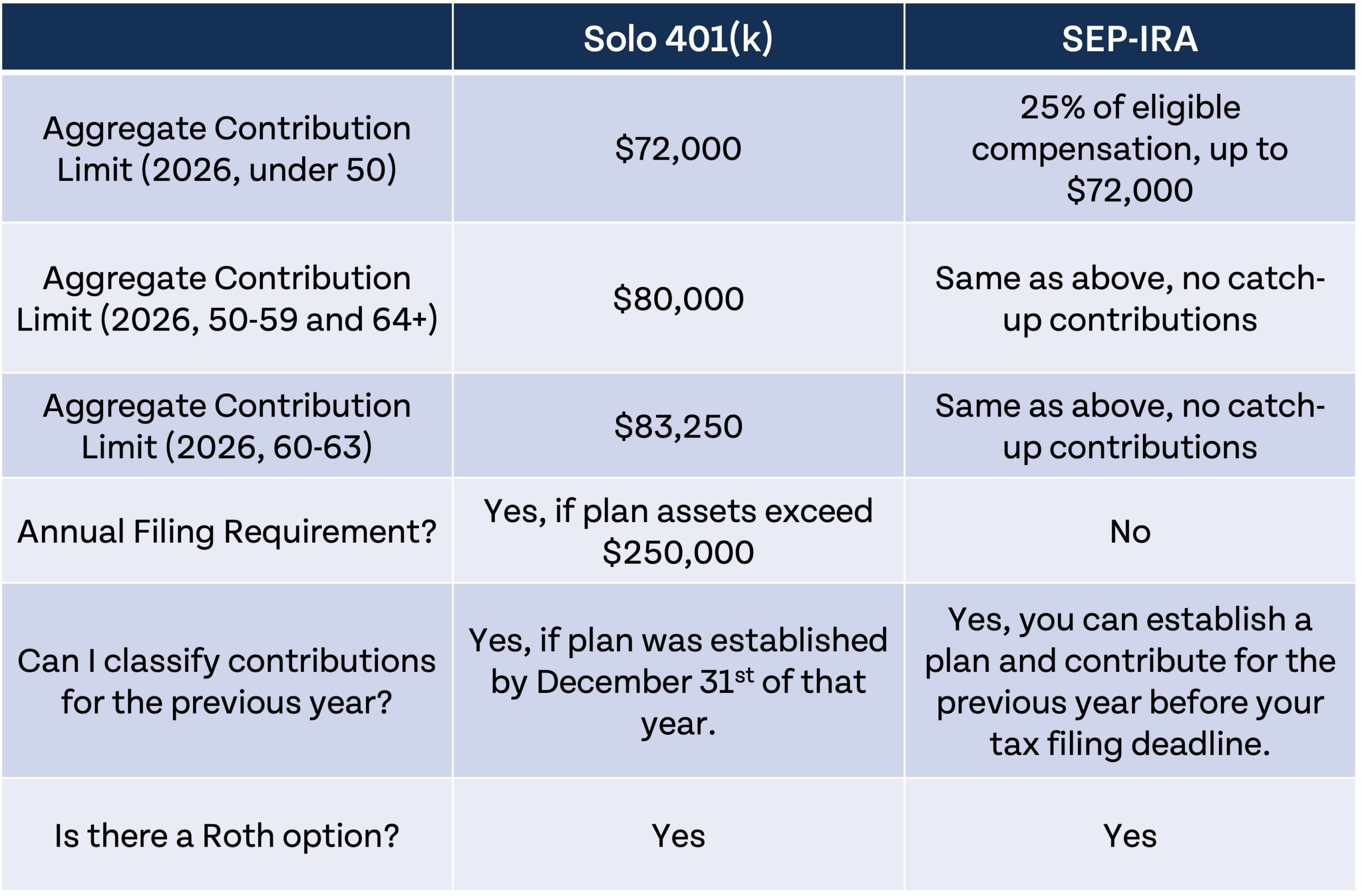

Like we mentioned earlier, solo 401(k) plans are generally the best type of retirement plans for business owners with no employees. One of the main reasons why it is considered superior are the higher contribution limits compared to other self-employed retirement plans. In 2026, aggregate solo 401(k) contributions (including contributions made as the employee and employer) can be up to $72,000 for those under 50. Many solo 401(k) plan providers offer Roth options in addition to pre-tax accounts, which not all self-employed retirement plans offer.

There are a couple minor downsides to solo 401(k)s. In order to make contributions in a certain year, you must have established the plan by December 31st. Some other plans allow you to establish plans and make contributions for the prior year. Additionally, once your solo 401(k) crosses the $250,000 threshold, you are required to file Form 5500-EZ with the IRS annually.

What Is The 3D Plan?

Copy link to this section: What Is The 3D Plan?

Copied the URL to your clipboard!

Before you make the enormous decision to start your own business, we believe you should plan for the best-case scenario, worst-case scenario, and most likely scenario. We like to call this the 3D plan.

Share image

- Dream scenario: This is the best-case scenario for your business and the most enjoyable to imagine. How does your business look if everything goes according to plan and your business is highly successful? It is not always easy to plan for success. A growing business means hiring employees, expanding, and keeping up with customer demand. You must be prepared for your business to experience rapid growth.

- Down-to-Earth scenario: What does the most realistic case scenario look like for your business? If this happens, your business will experience slow but moderate growth. As this is the most likely scenario, you should make sure it is worth quitting your job and taking all the risk that comes along with starting a business before you make the leap.

- Doo-Doo scenario: This is the worst case scenario. If your business fails, how will you recover? How long will you spend trying to make it work before you give up and work for someone else? Do you have the cash reserves to survive a failed business? It is extremely important to consider the worst case scenario. Hopefully it will never come to fruition, but it does for many entrepreneurs, and how you handle this failure could impact your finances for the rest of your life.

Calculating your personal “quit number”

How much money do you need saved before you consider quitting your job and starting your own business? You need enough savings to provide for your own expenses and cash to invest in your business. If you don’t have adequate savings built up when starting a business, you are destined to fail. Here are some important numbers you need to calculate to determine how much cash savings you need.

- How much income can we live off of every month?

- This is the minimum amount of money required to pay your bills and living expenses every month. Be prepared to reduce your expenses to this number if your business needs a longer runway for success.

- How much will it take to run the business every month?

- Depending on what type of business you start, it may take very little or quite a lot of money to run your business.

- How long will it be before the business can pay for our living expenses?

- Do your market research and determine how long it takes for successful businesses in your industry to start generating enough income to live on.

- If your business doesn’t become profitable within this timeframe, think about how long you are willing to invest in it and when you would consider giving up.

Quick Money Guy math example:

- Monthly living expenses: $5,000

- 12-month runway needed: $60,000 personal savings

- Projected monthly business expenses: $2,000

- 6-month business fund: $12,000

- Total cash savings to fund two years of living expenses and the business: $144,000

The Self-Employment Tax Wake-up Call

Copy link to this section: The Self-Employment Tax Wake-up Call

Copied the URL to your clipboard!

Handling your own taxes and withholding can be a major hurdle on your self-employment journey. With a traditional job, your employer withholds payroll taxes (Social Security and Medicare tax) and federal and state income taxes. When you are self-employed, you are personally responsible for withholding your own taxes. This can seem daunting at first, but once you familiarize yourself with how the tax system works for those who are self-employed, it’s actually quite simple.

You will likely need to make quarterly estimated tax payments to the federal government and your state (if you live in a state with an income tax). You must pay enough in taxes to meet the safe harbor threshold, which means paying at least 90% of your current year’s tax liability or 100% of the previous year’s tax liability (this increases to 110% for higher income earners). If you do not meet the safe harbor threshold, you may be subject to underpayment penalties.

The amount you will owe in tax varies, but it’s generally a good idea to set aside at least 25% of your pre-tax income for taxes. Adjust this percentage up or down as you get a better idea of what you owe in taxes.

Health Insurance in 2026

Copy link to this section: Health Insurance in 2026

Copied the URL to your clipboard!

How you handle health insurance will likely change when you become self-employed, especially if you previously were on a plan through your employer. Health insurance is often more expensive if you are self-employed; the average monthly health insurance premium in the US is now a whopping $752 for an individual. Enhanced Affordable Care Act tax credits expired at the end of 2025, which has made health insurance even less affordable.

We believe health insurance is a necessary expense. The cost of going without could be hundreds of thousands of dollars if you happened to experience a major medical event like being diagnosed with cancer. There isn’t any way around getting health insurance, but there may be ways you can lower the price you pay for health insurance.

If you are self-employed and your spouse is working, getting on your spouse’s health insurance plan may be the best and most affordable option. Coverage may be more expensive for you than it is for them, but could still be significantly less than purchasing your own coverage.

There are still ACA subsidies available for those with lower incomes, so if you are eligible for tax credits, a marketplace plan could be a cost-effective option. If you aren’t eligible for any tax credit, compare options available on the marketplace and from private insurers and choose a plan that meets your anticipated healthcare needs. For example, if you are in great health and don’t anticipate any big medical expenses, a plan with a lower premium but higher deductible may be more appropriate.

COBRA coverage is available for those leaving their jobs with health insurance, but is normally too expensive to consider. However, you can use what’s known as the COBRA loophole to elect coverage after you need it as long as it’s within 60 days from the date you lost coverage.

Losing benefits you didn’t realize you had

Taxes and health insurance aren’t the only things that change once you leave your job. You need to calculate the value of any other benefits you may receive to determine if self-employment is worth it for you. This includes retirement plan contributions, paid time off, sick leave, and disability or life insurance offered through your employer.

It may not be difficult to imagine replacing your income from your 9-5 job, but earning enough to replace all of your benefits can be a different story entirely. Make sure you aren’t overlooking any hidden employer benefits when determining if it is worth it to consider self-employment.

Your First 1-2 Years of Business

Copy link to this section: Your First 1-2 Years of Business

Copied the URL to your clipboard!

Separate personal and business finances immediately

You don’t have to be on the level of a professional bookkeeper when you start your own business, but it’s vital to get the basics right from the beginning. Maintaining separate credit cards and bank accounts for your business is a must. Trying to parse through commingled accounts to determine which transactions are personal and which are business-related is a nightmare. At the very least, start using spreadsheet software to track all of your business income and expenditures. Consider using accounting software to make tax time even easier.

When (and how much) to pay yourself

Don’t expect to replace your full-time income immediately unless you’ve been building your business on the side while being employed full-time. New businesses typically take at least two to three years to become profitable, and even when you become profitable, you may not be making enough to maintain your preferred standard of living.

Plan in advance exactly what threshold you want to hit before taking income from the business and how much you plan to reinvest in the business vs. take as income. This can be a difficult balancing act; if you are able to invest more back in the business, the business can grow more quickly and provide greater income in the future. However, taking profit out earlier can keep you from going back to your previous line of work.

The ultimate goal is to create a predictable and reliable stream of income from a business that can have irregular revenue. To achieve this, you may need to save money when times are good to prepare for down times.

Building a business emergency fund

Just like some households live paycheck-to-paycheck, businesses are no different. As we saw during the pandemic, many businesses don’t have enough cash on hand to survive for a month without any new revenue. This is no way to run a business and is not a recipe for long-term success. You should maintain a business emergency fund at all times of at least 3 to 6 months of all business expenses (payroll, rent, software, etc.). If your industry is subject to wild swings in revenue, consider maintaining an even larger emergency fund.

Insurance for the self-employed

In addition to health insurance, you may require other types of insurance when you are self-employed. Disability insurance is crucial. Depending on the type of policy you choose, any occupation or own occupation, your policy will replace a percentage of your income if you are unable to work any job or your own job. For those who wouldn’t easily be able to find another line of work that provides the same level of income, consider purchasing an own occupation policy.

Different businesses have different levels of potential liability to their customers. It is worth purchasing liability insurance to protect yourself against harm your business may cause to others. If you previously had life insurance coverage through your employer, consider increasing your coverage once you become self-employed if necessary.

Don’t scale costs before revenue

It can be tempting and really easy to spend large (and unnecessary) amounts of money on your business. Especially in the early days, run your operations as lean as reasonably possible so you have more to invest in what really matters, like customer acquisition. Instead of renting a fancy office space, work out of your home if possible. If your business needs equipment, consider purchasing second-hand units from businesses that no longer need them. Every potential expense should be carefully evaluated.

Assessing Success - Am I on Track?

Copy link to this section: Assessing Success - Am I on Track?

Copied the URL to your clipboard!

Metrics that matter

There are a few important metrics to keep an eye on when evaluating how successful your own business is.

Profit margin

It can be tempting to just focus on top-line revenue instead of profit margin, but having a large amount of money coming into your business does not mean your business is successful. If you are “making” $1,000,000 a year but have $950,000 in annual expenses, your profit is just $50,000 per year. Focus on how much you are making after all expenses, not your gross revenue.

Months of runway remaining

Is your business self-sustaining? If not, how long do you have until you run out of money? In the early days of your business, keep a close eye on how quickly your business is burning through cash and make changes as necessary to increase your odds of success.

Personal savings rate

It’s a big milestone when your business is able to completely provide for all of your living expenses, but it isn’t the final goal. You should be investing 25% or more of your income for retirement, and if you don’t make enough from your business to save for retirement, consider how you can make that change.

Client/revenue concentration

If your business is highly successful but your revenue is largely sustained by a handful of customers or clients, consider what would happen if those clients left and how you can reduce the impact a handful of customers have on your bottom line.

When to pivot vs. persist

Not all businesses are successful, and that’s okay. Sometimes it is better to give up rather than continue investing time and money in a failed business. Here are some signs it could make sense to pivot to a different venture.

Your business is 2-3 years old and you don’t have a clear path to profitability

Your business’s profit margin is the #1 indicator it could be time to try something else. If you’ve been in business a couple years and are making a small amount of money or aren’t even turning a profit, do you have a clear path to profitability? How realistic is it? What will be different in the next few years? If your business is not close to replacing your income and you don’t anticipate that changing anytime soon, it could be time to shift your focus to something different.

You don’t enjoy working for yourself as much as you thought you would

Self-employment isn’t for everyone. Even if your business is doing well and providing more than enough income, are you happier than you were working a regular job? The added stress and responsibilities of owning a small business can burn you out. Don’t continue your business venture if you are miserable and unhappy.

The future doesn’t look bright

Industries are constantly changing, and your business model may not look as rosy after a few years as it did when you first started your company. If the outlook for your future success has changed, it might be time to consider pivoting to a different venture.

If your business is struggling, the decision isn’t always “give up” or “keep going.” There are often middle grounds to choose from. Consider making changes to your business that allow you to keep operating instead of abandoning the business entirely.

When to go back to a W-2 (and why that’s okay)

There is no shame in returning to full-time employment if your business doesn’t work out. Even if you aren’t successful, you likely gained valuable experience that will make you an attractive higher to a future employer. It is better to have given entrepreneurship a shot and failed rather than never attempting it and never knowing if you could have been a successful small business owner.

There are often different options available rather than just completely giving up on your business and going back to full-time employment. Perhaps you maintain a side business and part-time employment. Diversifying your income sources can be especially valuable in tight job markets when you are at greater risk of losing a source of income.

The Entrepreneur Mindset

Copy link to this section: The Entrepreneur Mindset

Copied the URL to your clipboard!

Your psychology under pressure

Owning a small business can not only be hard on your finances, it can be hard on you mentally and emotionally. Operating a small business is often a balancing act between maintaining your own mental health and prioritizing the financial health of your business. Would it be better for your business for you to work 80 hour weeks? Sure. Is it better for you to work shorter weeks when possible, take vacations, give yourself breaks when you are feeling burnt out, and take time off when sick? Definitely.

You need to know yourself and what you are capable of. Don’t push yourself too hard, but be prepared to extend yourself to your limits. You will likely work long hours and be “on the clock” at odd times of the day.

Spouse and family alignment

If you are younger and single, you don’t necessarily need buy-in from anyone else to start your own business. But if you have a family, they must be on-board for your business to be successful. Even if they are not going to be involved in the day-to-day operations of the business, it’s important that they understand the risks involved with the business, the anticipated timeline for milestones like profitability, what failure looks like and how it will be handled, and how your lifestyle will be different during the early phase of your business.

Avoiding burnout

While you will almost certainly be working longer hours during the early days of your business, it’s still important to give yourself breaks and plan vacations and time away. It is not sustainable to work 80+ hour weeks with no time off. You will burn yourself out and your business will not be successful. Your emotional and mental wellbeing is just as vital to the success of your business as your financial health.

The comparison trap

The reality of owning a business is significantly different than what you see on social media. It doesn’t mean driving fancy cars, vacationing in exotic locations, and experiencing immediate financial success. Business ownership is simply an alternative career path for those who prefer greater control over a large portion of their lives. Owning a business does not make you better or more successful than someone with a traditional job.

Comparison is important as a business owner. You need to know how your business is doing relative to your peers. However, compare your business to other entrepreneurs you know personally, not what you see on social media, which are only the success stories.

Common Mistakes and Regrets

Copy link to this section: Common Mistakes and Regrets

Copied the URL to your clipboard!

Not validating the idea first

Having a great business idea is a requirement if you are going to be an entrepreneur, but a great idea does not guarantee success. You need to test and validate your idea to ensure it has the potential to become a successful business before you dive in. If there aren’t any competitors in your market, it could be because they tried and failed and are no longer in business.

If you know you have a great idea that has the potential to become a profitable business, how do you plan to obtain your customers and market your business? Plenty of failed businesses withered away due to lack of awareness. There are many critical factors that build a successful business, and an idea is just the starting point.

Confusing revenue with profit

It is easy to confuse revenue with profit if you have only ever worked a traditional job. Everything you make from working for someone else is effectively “profit”: you don’t have to pay for inventory, the software you use at work, or customer acquisition. When you own a business, though, you are responsible for all business expenses. If you aren’t careful, it can seem like your business is doing really well on paper. It is much easier to develop six or seven figures of revenue, but turning that into profit is far more difficult. Revenue looks exciting, but profit pays the bills.

Partnering with friends or family

Involving friends and family in your business is extremely common. 75% of entrepreneurs report working with their family in their business to some degree. While it isn’t always a bad idea to work with friends and family, it has the potential to ruin relationships and your business. If you do choose to work with those close to you, make sure they are the most qualified person for the job and aren’t being hired because of their relationship with you. Keep the relationship at work professional and make it clear from day one that they will be treated like any other employee or business partner.

Scaling too fast

The ultimate goal of a business is obviously to grow it and expand, but growing too fast has the potential to cause more harm than good. Early in your entrepreneurship journey, all spending should be carefully considered and have a near-immediate return on investment. For example, it may not make sense to purchase a property for your business in the first year even if you can afford it on paper. This decision could pay off in the long-run, but your focus should be on more immediate returns in your first year, like customer acquisition, inventory, and employees.

It is a delicate balance between being a frugal business owner and a cheapskate. Software, tools, and subscriptions can drain your cash flow, but there may be some that are necessary to run your business. Whenever possible, especially early in your entrepreneurship journey, aim to save money as long as it doesn’t hurt your business.

2026 Economic Considerations

Copy link to this section: 2026 Economic Considerations

Copied the URL to your clipboard!

Tailwinds for entrepreneurs

Owning a small business has changed significantly over the last decade. AI tools have the potential to reduce your operating costs, save you time, and help grow your business faster. At the same time, employees in some industries have new expectations of what the workplace will look like. It may be more difficult to hire in-person employees in some fields, but you can now recruit worldwide for many roles and significantly expand your talent pool (and often lower labor costs). Adapting to the changing world of business ownership is crucial to your success. Those who can adapt and change quickly will survive and grow, while those who fail to change may not stay in business much longer.

Headwinds to watch

Not all changes in the business world have been positive. Borrowing costs have risen significantly over the last several years, which means it could be harder to get a loan for your business and the costs may be higher. Enhanced ACA subsidies expired at the end of 2025, so health insurance could be a larger cost now than it was in the past. Tariffs are still impacting many industries, and higher costs are impacting around 70% of small businesses. If your business isn’t successful, it could be harder to get your old job back. Labor conditions are significantly tighter, especially in industries more impacted by AI like tech.

Building cash reserves as a defensive measure

As you navigate the ever-changing world of entrepreneurship, building a substantial amount of cash reserves can give you a buffer to protect you when times are tough. Shockingly, 39% of small businesses have less than one month of cash on hand. Businesses with little or no cash on hand will be the first to fail when the economy gets worse. Aim to keep at least 3 to 6 months of expenses in cash, and possibly more depending on how prone your industry is to fluctuations.

FAQs

Copy link to this section: FAQs

Copied the URL to your clipboard!

Does the FOO apply if I’m self-employed?

The Financial Order of Operations still applies to those who are self-employed, but it does look a little different. Step 2, employer match, obviously doesn’t apply if you don’t have an employer. Your emergency fund at Step 4 should include not only your personal emergency fund, but your business emergency fund. Maximizing your retirement accounts at Step 6 may include different accounts like a solo 401(k) or SEP-IRA instead of a traditional employer 401(k).

How much runway do I really need before quitting?

The more money you have saved before quitting your job, the longer you will have to make your business work and the greater your odds of success. At a minimum you should have your living expenses covered for 6 to 12 months. Many businesses take several years to become profitable, and if your business is in an industry where that may be the case, you should have enough cash reserves to cover your living expenses until profitability.

Should I quit my job before my side hustle is profitable?

If your side hustle isn’t profitable while you have a full-time job, what will change once you quit your job? Building a profitable side hustle while working full-time can be a great on-ramp to entrepreneurship, but whenever possible, you should have proof of concept (profitability) before making the jump. If you are already replacing a significant portion of your income, your odds of success will be much higher when you quit your job.

Solo 401(k) vs. SEP-IRA – which is better?

Solo 401(k) plans are best for most entrepreneurs. They have higher contribution limits for many small business owners since the contribution limit isn’t tied to eligible compensation like with SEP-IRAs. SEP-IRAs are easier to set up and have fewer reporting requirements. Check out the table below to compare the differences between solo 401(k)s and SEP-IRAs.

Share image

How do I handle health insurance when I leave my job?

There are three main options for health insurance if you leave your job. If you can be covered under your spouse’s employer plan, that may be the best and most affordable option. The ACA marketplace and private insurance options are available to those who aren’t able to be covered under a spouse’s plan. COBRA coverage can provide a temporary bridge after you leave your job and allow you to temporarily keep your old coverage, but it is typically very expensive so should only be used if absolutely necessary. There are many variables that determine how much health insurance will cost, and it could range from a few hundred dollars per month to several thousand dollars per month.

What if my business fails – can I recover?

Absolutely. If you’ve followed the framework – maintained your emergency fund, kept investing for retirement, and didn’t take on crushing debt – a failed business is a setback, not a catastrophe. Many successful entrepreneurs have failures in their past.

Should I form an LLC or S-Corp?

This guide doesn’t provide legal or entity-structure advice. Consult with a CPA and/or attorney based on your specific situation. Generally, entity structure matters more as income grows.

Conclusion

Copy link to this section: Conclusion

Copied the URL to your clipboard!

Entrepreneurship can accelerate your path to owning your time – or it can set you back years. The difference isn’t luck; it’s preparation.

The Financial Order of Operations is your guardrail. The “Ready to Quit” rule keeps you grounded. And the mindset of treating your business as what it is – a concentrated, risky investment – ensures you don’t bet everything on a single outcome.

Build your army of dollar bills while you build your business. That’s how you create a more beautiful tomorrow without destroying today.