Alright, now let’s shift gears. Let’s talk a little bit about the next decade. Let’s talk about the ’40s because in the ’40s, a lot of stuff can happen. I don’t want to say necessarily it’s a turning point, but I think realistically for a lot of folks, it is a turning point. It’s the point where you say, “Uh-oh,” or one of those two things. Yeah, it’s definitely if you’ve actually been practicing this, you’ve been a financial mutant for several decades now. This is where you might get to take your foot off the accelerator and actually look and enjoy, starting to feel like you’re getting into step eight of the abundance goals and prepaid future expenses of the Financial Order of Operations.

But I do think there are a lot of people who get in their 40s and there’s still that rudderless ship. This is the point, and there’s no way to say it: no pain, no gain in this decade because you’ve got to play catch-up. You’ve got to figure out your direction, your purpose. I also see this as the stage where decisions that, in the moment, might feel okay could be extremely detrimental to your future, not only emotionally but also financially. We know for a fact that there are a lot of divorces that occur in your 40s, and divorces don’t just happen when you announce or decide you’re getting divorced. It builds up over the two years even before. It’s not uncommon to see the stat that divorcing families lose 77% of their wealth. I love it. It’s this idea that short-term decisions or short-term comfort can lead to very long-term pain, long-term detrimental decisions in your financial life.

So one of the things you have to figure out is, okay, in my 40s, if I’m going to try to catch up, if I’m going to try not to be a rudderless ship, and I want to have direction and purpose, what are some things that I can do? What are some things that I can put into place? The first thing we said is to isolate those things that are inside your control versus those things that are outside your control. Now, we’re going to talk about the financial parts that are inside your control, but there are other things that are bigger and existential in your 40s. Brian, again, I’ve got to give you so much credit for this. You said everyone has this. There’s a voice inside your head that lives there, and that voice is either going to be an optimist or a pessimist. You get to choose it. No matter what situation you’re facing, no matter what life thing you’re walking through, you have to figure out: are you letting negative thoughts into your mind that cause you to devolve and spiral, or are you figuring out how to turn those negative thoughts into positive thoughts that allow you to move forward? Controlling that voice in your head is one of the things that you can control, and if you ignore it, don’t pay attention to it, or worry, it will force you to continue to be a rudderless ship in your 40s.

Yeah, and that’s why, I mean, I want you to get that voice under control and hopefully have the pep talk to turn it into an optimist. It is a time when, that’s what I like about isolating, getting away from all the noise and thinking about exactly what you can control. There are really two components that are going to help you out in your wealth-building journey: how do you spend less money so that you can play catch-up, or how do you go out there and make more money? Because spending less money is going to have limits. You’re only going to be able to cut so much. But you know what? Making more money can actually be limitless if you really put your mind to it, get creative in the processes. I know it’s so much easier said than done, but it is the reality of the situation. Isolate what you can control and then go become the best version of yourself.

I love it, and Brian, you say this all the time: in your 40s, you can refocus on your why, your actual goals. I think one of the things you did great, Brian, is at 24 or 25 years old, you said, “You know what? At 50, I’m going to retire.” At 50, I’m going to check out. What I love is, I’ve got to believe that it was 40-year-old Brian that said, “You know what? I’m kind of liking this thing that I get to do. It’s pretty exciting.” I imagine at some point along that journey, you did refocus that why and said, “Hey, my goal might not be an age 50 retirement. My goal might be to get more financial information out there, take care of more people, travel with my family, grow an enterprise, whatever those things are.” In your 40s, if you can refocus that why and make sure the decisions you’re making are aligned with that why, there’s a much better chance you’re not going to be a rudderless ship, but you will be a ship on course towards a specific destination.

Yeah, I’ve talked about this a lot. Money is just a tool. There’s a lot of things that we do in life that I think a lot of people are going after a false promise financially. Meaning, they think if I get to a million dollars, my life’s going to be so much easier. If it’s $2 million, that’s just not the way money and success have traditionally worked. As I’ve gotten there and experienced things and even helped clients with it, you better really spend some time on the exercise of knowing what’s your why. What is it that begins with the end in mind? What does my best retirement look like? What will I be doing not just financially, but also so I wake up every morning feeling like I have purpose and that I’m actually making the world a little bit better? Spend some exercises on that. How are you going to pay for college for the kids? All these things are interconnected, and that’s what I want you to do in this 40 phase. Because you do recognize, believe me, I’m about to exit this decade, and you get very sentimental, very reflective. So take advantage of all that special focus that you have in this decade to figure out how do you get where you want to be.

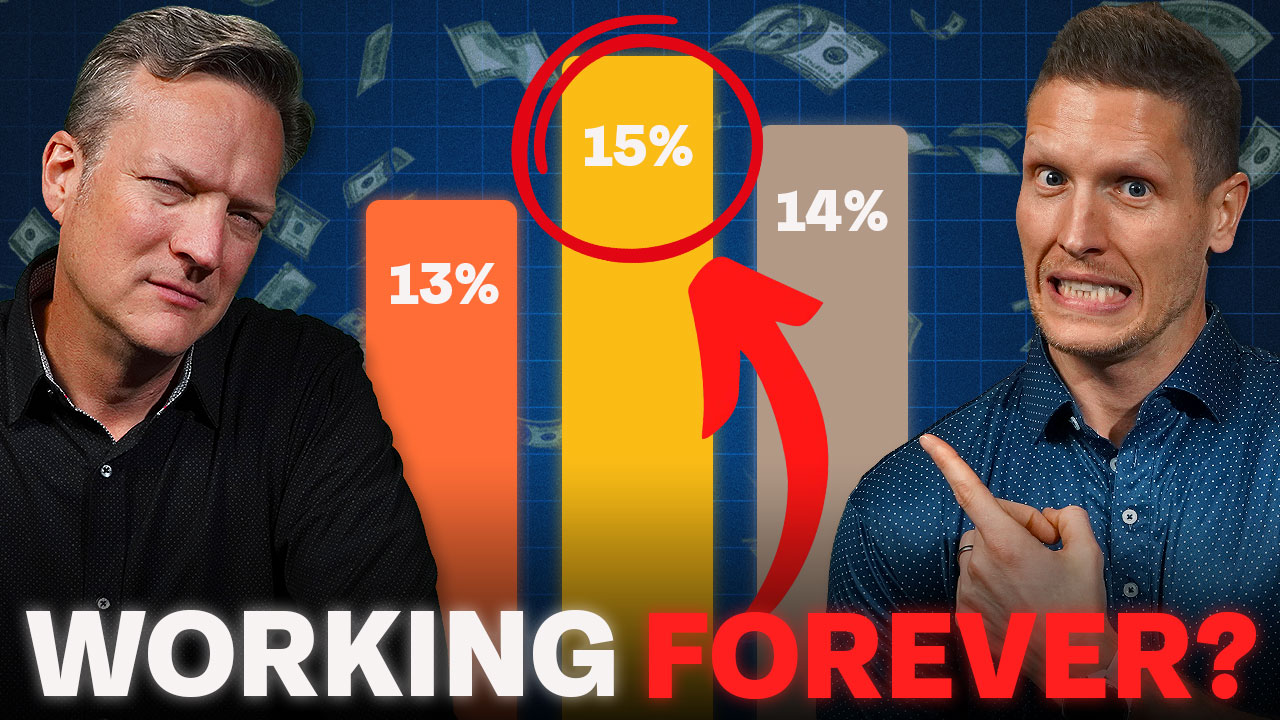

Now, what I love, Brian, is in your 40s, in our 20s and 30s, we’re talking about incremental changes. Okay, if I can just save 1% more, 1% more. I would argue if you’ve not been doing what you were supposed to be doing in the prior decades, and you found that you’re behind, you’re not where you ought to be from a saving and financial wealth-building standpoint, then at 40, or in your 40s, it doesn’t become so much of an option of, “Okay, well, how do I make incremental decisions?” It’s kind of like, “How do I fix this? How do I right this?” Because if you can do that in your 40s, reaching a 25% savings rate can still do remarkable things for you over the next 20 to 30 years. We actually ran the mathematics on this. Let’s say that you’re a 40-year-old and you’ve not saved anything thus far. If you start saving 25% of your gross income, starting at zero at age 40, there’s still a good chance that by the time you get to 69, not even 70 years old yet, you would be able to build up a pot of money that could replace 80% of your pre-retirement income. Now, perhaps the situation looks better. Maybe you have a pension. Maybe Social Security will be a big part of your retirement income. Maybe you’re able to downsize your life and decrease your expenses as you enter into retirement.

It’s not too late in your 40s, but you better take it seriously because now it’s a half to, not a might want to. Well, I don’t mind being even a little harder because when I look at these numbers, 40 to 60, meaning if you save 25%, you can retire at 69. If you’re starting out right at 40, 4574, I’ll be Sergeant Slaughter. I’ll be the one that looks you in the eyes and says, “Look, if you don’t like these numbers, if they scare you, save more, invest more. What’s wrong with you?” I know it’s because it’s tough. Look, you’ve got to make some hard decisions while you still have decades in the future because if you keep letting time slip through your hands, the opportunity and the option to fix this and isolate what you can control is going to leave you behind. Let’s figure out, hey, wake up call. How do you actually focus on the discipline of creating margin and money in your life so you still have decades of time to let this money grow upon itself? Maybe you need to be saving 30, 40. Do what you have to do, make the heavy decisions today so you have a better tomorrow in the future. For more information, check out our free resources.