Change your life by

managing your money better.

Subscribe to our free weekly newsletter by entering your email address below.

Subscribe to our free weekly newsletter by entering your email address below.

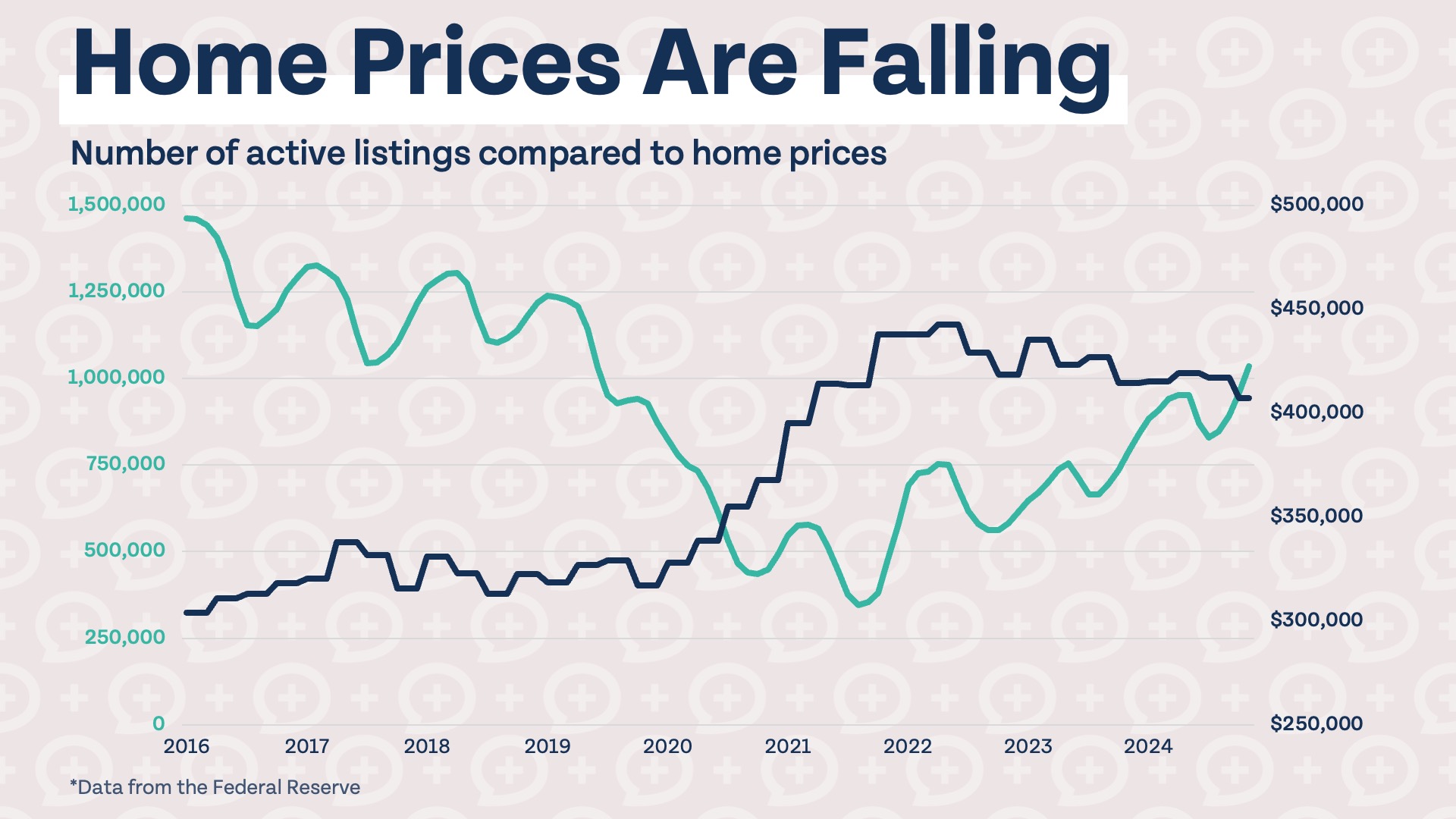

Since 1990, the median sales price of homes in the United States has increased 244%, according to the most recent Federal Reserve data. Meanwhile, median household income has only risen by about 180% in that same time. With home prices outpacing income growth, rising mortgage rates, and a national housing shortage of nearly five million homes (according to the U.S. Chamber of Commerce), it’s fair to ask: Is buying a house still worth it?

Even those who can afford the down payment often find themselves stretched thin once they factor in closing costs, maintenance, and unexpected home expenses.

To find out whether renting or buying makes more sense in today’s market, The Money Guy Show used a Rent vs. Buy Calculator (like this one from the New York Times or NerdWallet’s version).

According to Apartments.com, the national average rent for a two-bedroom apartment is about $1,900 per month. This varies by location, but it gives a solid baseline.

Using The Money Guy Home Buying Calculator, the following assumptions were made:

Based on these figures, a household could afford a home priced around $380,000, which aligns closely with the current U.S. median home price of roughly $440,000.

Over a 10-year period, assuming an 8% average annual investment return:

This analysis considers:

While $120,000 may not sound life-changing, in your 30s or 40s, this difference could meaningfully accelerate your path to financial independence through compound growth.

The analysis above assumes today’s rates (~6%). If mortgage rates dropped to around 3.5%, buying would again become financially superior to renting in this scenario.

That’s because interest rates dramatically affect:

At 6%, a buyer would only pay down about $58,000 of principal over a decade — the rest goes toward interest.

Numbers aren’t the whole story. Homeownership offers benefits that calculators can’t capture:

However, there’s a key downside — illiquidity. Unless you sell and downsize, your home equity remains tied up. Many homeowners are “house rich, life poor,” meaning their wealth looks good on paper but they have little flexibility for saving, investing, or enjoying life.

The rent vs. buy decision isn’t purely financial — it’s also about lifestyle and personal goals. Consider:

For some, renting provides freedom and peace of mind. For others, owning a home brings stability and pride.

The key is to make the decision intentionally, not just because conventional wisdom says it’s what you “should” do.

Bottom Line:

We’re at a fascinating crossroads where traditional financial wisdom meets today’s economic reality. The right choice isn’t universal — it’s personal. By understanding the math, risks, and emotional factors, you can align your living situation with the life you want to build as you move toward your great big beautiful tomorrow.

Related Resources from The Money Guy Show:

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

244% — that’s the increase in the median sales price of homes sold since 1990, according to the most recent FRED data. It makes you wonder if buying a house is even worth it for most folks with the state of the current housing market. This decision can make or break your financial life, especially if you’re making it early on. Today, we’re walking through how to know whether you should buy or rent in the current market and the tradeoffs that come with each choice.

The median sales price of homes in the U.S. has increased 244% since 1990, while median household income has only risen by 180%. Despite recent construction booms, the U.S. still faces a significant housing shortage — nearly five million homes short, according to a U.S. Chamber of Commerce report. Add to that some of the highest mortgage rates we’ve seen since the early 2000s, and it’s having a massive effect on young Americans’ ability to buy.

The average age of a first-time homebuyer in the U.S. is now 38 years old, up from 28 in 1990. Homeownership has long been considered a seminal stepping stone in the financial lives of young Americans, but that goal seems to be drifting further away. Many are now stretching just to make a down payment — not to mention closing costs and the unforeseen expenses of ownership. So, is it even worth it?

To answer that, we need to do a rent vs. buy calculation. This exercise can help determine which path may be best for your situation. For this video, The Money Guy team used the New York Times rent vs. buy calculator, but there are plenty of free options out there — NerdWallet’s rent vs. buy calculator is a good one.

According to Apartments.com, the national average rent for a two-bedroom apartment is around $1,900 per month. While this varies by location (major metro areas are much higher and rural areas lower), we’ll use the national average for this example.

To assess the buying side, we need to determine how much house a typical American household can afford today. Using the Money Guy Home Buying Calculator, we need three key variables: income, down payment, and interest rate.

Fidelity’s analysis of the Bureau of Labor Statistics’ Current Population Survey found that median weekly earnings in Q1 2025 were just under $1,200 — or about $62,000 annually for individual earners, and $125,000 for a dual-earning household. Assuming a $20,000 down payment and a 6% mortgage rate, plus private mortgage insurance (PMI), this household could afford a $380,000 home. That’s roughly in line with the current median home price of about $440,000.

Now, let’s compare renting vs. buying over a 10-year period, since the average American moves every 7–10 years. Using $380,000 for the home price and a 6% mortgage rate, the results are eye-opening. Assuming an 8% average annual investment return, renting actually comes out ahead by about $120,000 over the decade.

Neither Brian nor Bo have any vested interest in promoting renting — they simply follow the math. The calculation accounts for home appreciation, rent increases, inflation, tax benefits of homeownership, and the opportunity cost of tying up capital in a down payment instead of investing it.

While $120,000 may not seem monumental, in your 30s or 40s it can significantly accelerate your path to financial independence through the power of compound growth. This outcome is heavily influenced by today’s high interest rates — if rates fell to around 3.5%, buying would once again become the better financial choice.

At 6% interest, you’ll have paid off only about $58,000 in principal after 10 years. That highlights how crucial interest rates are in this equation — a factor many overlook when focusing solely on purchase price.

However, math isn’t the whole story. Homeownership offers several advantages not easily captured in a calculator. Homeowners enjoy protection against inflation, since fixed-rate mortgage payments remain steady while rents rise. They also build equity over time as property values appreciate — though this wealth is illiquid unless you sell or downsize.

If housing costs consume too much of your income, you risk becoming house rich and life poor — impressive on paper, but constrained in reality. The Money Guy team recommends keeping housing costs below 25% of gross income to preserve the ability to save, invest, and enjoy life.

Beyond finances, homeownership also offers intangible benefits: establishing roots, customizing your space, and gaining emotional stability. These quality-of-life factors can outweigh the purely financial calculations. The rent vs. buy decision is as much a lifestyle choice as it is a financial one.

What’s right for one person might be completely wrong for another — even with identical financial profiles. In navigating today’s housing market, traditional wisdom collides with modern economic realities. The decision ultimately depends on your timeline, local market conditions, and personal priorities.

Some value the freedom of renting; others seek the stability and long-term wealth potential of owning. What matters most is making the decision intentionally, not by default. By understanding the true costs and benefits of both paths, you can choose the option that fits both your financial goals and the life you want to build.

For more tools and insights, explore these Money Guy resources:

Free Resources

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

The Trump administration recently proposed offering homebuyers the option to choose a 50-year term for their mortgage, which they said would be a “complete game...

Articles

As mortgage rates have held relatively steady over the past few years, with average fixed 30-year rates between 6% and 8% since September of 2022,...

Articles

After a brief reprieve from 7% mortgage rates in August and September, 30-year fixed rates have surged back above 7%. We first hit 7% rates...

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

Think $1 million is enough to retire? Bo reveals what that number actually buys you, and how Social Security and inflation can change everything.

Episodes

Could the biggest factors in a fulfilling retirement have less to do with your savings than you think? We break down the mindset shifts, habits,...

Episodes

We react to the internet's wildest financial takes, from gas tank wealth hacks to meme stock luck and Rolex investments, separating ridiculous advice from a...

Subscribe to our free weekly newsletter by entering your email address below.