Last Updated

May 19, 2026

Read Time

Share

Which types of insurance do you really need, and which ones can wait? Whether you’re protecting your income, your health, or your growing family’s future, this Money Guy Ultimate Guide to Insurance expands on the crucial first step of our Financial Order of Operations (FOO).

Insurance is Step 1 of the FOO!

What are the nine steps of Money Guy’s Financial Order of Operations (FOO)? Download this free guide to the FOO to get started.

Brian Preston’s book Millionaire Mission, a guide to the nine steps of the Financial Order of Operations, is available now.

Insurance and the Financial Order of Operations (FOO)

Copy link to this section: Insurance and the Financial Order of Operations (FOO)

Copied the URL to your clipboard!

Copy link to this section: Insurance and the Financial Order of Operations (FOO)

Copied the URL to your clipboard!

There are many different types of insurance and not all are created equal. Some are required, like car insurance, while others are optional. And, some may even be harmful to your financial life. Insurance is a double-edged sword. It can be a valuable tool to reduce risk in your financial life, but when used improperly, it can hinder or halt your financial growth.

Making sure you are properly insured isn’t a single step in the Financial Order of Operations, but a pre-requirement for beginning your journey. Step One of the FOO is covering your insurance deductibles, which implies you already have the proper insurance policies in place and have enough saved to cover your deductibles if you needed to utilize your policy.

So, How Does Insurance Work?

Copy link to this section: So, How Does Insurance Work?

Copied the URL to your clipboard!

Copy link to this section: So, How Does Insurance Work?

Copied the URL to your clipboard!

Insurance in the United States is a regulated industry, and states are the primary regulators of that industry. This means depending on which state you live in, the insurance industry may look a little different.

No types of insurance are mandated by the government, but you may be required to carry insurance to operate a motor vehicle. If you purchase a home with a mortgage, your lender will almost always require you to carry homeowners insurance. Although there is no longer a federal penalty for not having health insurance, some states collect tax penalties from those that go without health insurance.

Beyond different types of insurance that may be a requirement to hold, if you have a mortgage and drive a car, it may be a smart idea to carry other types of coverage.

Share image

Share image

Are Insurance Companies a Scam?

Copy link to this section: Are Insurance Companies a Scam?

Copied the URL to your clipboard!

Copy link to this section: Are Insurance Companies a Scam?

Copied the URL to your clipboard!

Although insurance is a very regulated industry, sometimes paying for insurance can feel a little bit like a scam. You can pay into insurance for years or even decades without seeing any financial benefit. If you do need to use your insurance benefits, the insurance company may then raise your rates. For insurance to work, the policyholders must pay, in aggregate, more than they collect in payouts. This means most people will naturally feel like insurance isn’t a good value, or that they aren’t getting their money’s worth.

Those that do get their money’s worth aren’t likely to be very happy about it. If you collect from insurance, it likely means something catastrophic has happened in your life. It could be a major car accident, a fire that destroyed your home, or an unexpected medical diagnosis. Insurance is not an investment or something that you should expect to get a lot of money from one day. It is a safety net that is there to protect you against uncontrollable and unpredictable events.

“We believe that insurance plays an important role in managing risk and protecting you and your family from unforeseen events. However, we also believe that some salespeople take advantage of the unsuspecting public through difficult to comprehend policies that aren’t always in the best interest of the consumer. One of the more popular concepts is called “infinite banking” or “bank on yourself.” Is infinite banking a good investment?”

Are There Insurance Alternatives?

Copy link to this section: Are There Insurance Alternatives?

Copied the URL to your clipboard!

Copy link to this section: Are There Insurance Alternatives?

Copied the URL to your clipboard!

Perhaps due to the rising costs of insurance, alternatives to traditional insurance have risen in popularity over the last several years. There’s no getting around carrying car insurance if you drive or homeowners insurance since your mortgage lender requires it, but healthcare sharing plans or discount plans have become popular alternatives to health insurance.

While the cheaper cost of health share plans may be attractive, there are some big drawbacks when compared to real health insurance. Health share plans are not subject to insurance industry regulation. They do not need to cover pre-existing conditions or cap out-of-pocket costs. They are not even legally required to pay out claims. Your experience may be good with a health share plan, but the risk is substantial and could be catastrophic to your financial life.

Self-insuring is a viable alternative to certain types of insurance if your financial situation can handle it. What does that mean? Well, at a certain point, you may have enough in assets to cover certain risks, like an untimely death.

What Types of Insurance Do You Need?

Copy link to this section: What Types of Insurance Do You Need?

Copied the URL to your clipboard!

Copy link to this section: What Types of Insurance Do You Need?

Copied the URL to your clipboard!

There are certain types of insurance you shouldn’t go without and others that you may not need. Home insurance and car insurance are likely required by your state or lender and are no-brainers to carry. Health insurance is not required, but since nobody can predict medical expenses with 100% certainty, health insurance is a must to protect your finances.

Life insurance is not always necessary. The general rule for life insurance is if someone else is dependent on your income, it may be a good idea to have coverage if you are not able to self-insure. If you are single and don’t have any dependents? You may not need life insurance. Disability insurance could be a good idea if a disability would make it difficult for you to earn a living or impossible to continue doing what you do. Disabilities are extremely common, with one in four adults in the US living with disabilities, and if a disability could affect your financial life, it may be a good idea to carry disability insurance.

Some other types of insurance may or may not be a good idea depending on your risk tolerance and ability to self-insure. One example is pet insurance. Some find it extremely valuable and well worth it, while others would rather take their chances and self-insure against any potential illness or vet bills.

How Much Coverage Do You Need?

Copy link to this section: How Much Coverage Do You Need?

Copied the URL to your clipboard!

Copy link to this section: How Much Coverage Do You Need?

Copied the URL to your clipboard!

The amount of insurance coverage you need depends on your risk. If you are not in great health or have a family history of medical conditions, it may make sense to carry more health insurance. If you have a large amount of financial assets to protect, more umbrella insurance could make sense. A fee-only financial advisor can help determine how much insurance coverage your particular financial situation warrants.

Types of Insurance You Probably Need

Copy link to this section: Types of Insurance You Probably Need

Copied the URL to your clipboard!

Copy link to this section: Types of Insurance You Probably Need

Copied the URL to your clipboard!

Homeowners Insurance

Homeowners insurance can protect your home and belongings against loss, damage, and other events. It may be required by your lender if you have a mortgage on your home.

- Where do you get it?

- You can obtain coverage online or through a licensed insurance broker or agent. If you live in an area with an extremely high risk of natural disaster, your options for homeowners insurance may be limited.

- How much coverage do you need?

- The amount of insurance you need does not depend on the market value or appraisal of your home, but the estimated cost to rebuild your home from the ground up. This could be drastically different than what your home is worth as construction costs have risen significantly in recent years. In addition to the cost to rebuild your home, you can choose to add extra liability coverage and to pay more monthly for a lower deductible.

- How much does it cost?

- The cost of coverage is generally tied to the risk of your home being destroyed or damaged, or in other words, the likelihood that you will need to file a claim. In Vermont, a state with little risk of natural disasters like hurricanes, tornadoes, or floods, the average annual premium is $816. In Nebraska, a state with a significant amount of tornadoes, the average annual premium is $6,366.

Money Guy’s Take:

Homeowners insurance can protect your home and belongings and the cost to self-insure is very steep. For almost everyone, it is a good idea to have homeowners insurance.

Related videos, articles, and FAQs

- Buying a House – Money Guy’s Ultimate Guide To Your Biggest Purchase

- What Types of Insurance Do You Need?

- Homeowners Insurance 101

Life Insurance

There are many different types of life insurance and they all work a little differently. At its core, life insurance is meant to protect you or a loved one against an unexpected death.

- Where do you get it?

- You can obtain coverage online or through a licensed insurance broker or agent. To get the best rates, you usually will need to undergo a medical exam, especially with a larger policy.

- How much coverage do you need?

- Not everyone needs life insurance. If you are single with no liabilities, it may not make sense to get life insurance. However, you should consider your need for life insurance if your death would cause financial strain for loved ones, like parents, your spouse, or children. The amount of coverage you need depends on how you would like to provide for your loved ones in the event of your death.

- How much does it cost?

- Term life insurance is very affordable and the cost depends on your age, health, and sex. A 40-year-old female in average health can expect to pay about $46 per month for a $500,000 20-year term life policy.

Money Guy’s Take:

We love the protection that term life insurance offers, but we don’t believe life insurance makes a great financial investment. You may only need term life insurance if someone else depends on your income to live.

Related videos, articles, and FAQs

- Do I Need Life Insurance? What’s the Difference Between Whole Life and Term?

- Is It a Good Idea to Use Permanent Life Insurance for Long-Term Care Expenses?

- At What Net Worth Should You Cancel Your Life Insurance?

- Life Insurance 101: What You Need (and What You Don’t)

Health Insurance

Healthcare costs in the United States are unpredictable and potentially very expensive. Even a simple medical issue could lead to a five-figure medical bill if you don’t have insurance.

- Where do you get it?

- About 60% of Americans under 65 have health insurance through their employer. If your employer doesn’t offer health insurance, or you don’t like their options, you can also shop on the Health Insurance Marketplace or get quotes from private insurance companies. Medicaid may be available depending on your income, and Medicare is available to those 65 and older.

- How much coverage do you need?

- If you have chronic health issues or are older, it may be a good idea to pay a higher monthly premium in exchange for better coverage. If you are young and in good health, you may be able to choose a cheaper plan with lesser coverage.

- How much does it cost?

- Health insurance can range in cost drastically. Some employers pay for their employees’ coverage as a benefit and their workers pay nothing for coverage. With Affordable Care Act subsidies expiring, many Americans will suddenly find themselves paying thousands of dollars per month more for health insurance.

Money Guy’s Take:

You should probably carry health insurance even if you are in good health. While it can be extremely expensive, nobody can predict when they may have large, unexpected medical bills.

Related videos, articles, and FAQs

- What is an HSA and Should I Contribute to One?

- HSAs, FSAs, and More, Oh My!

- HRA, HSA, and a Little History of Insurance

Disability Insurance

If a disability would impact your ability to make a living, it is a good idea to carry disability insurance. Many people are covered through their employer but additional disability insurance may be necessary depending on your profession or level of income.

- Where do you get it?

- Social Security Disability Insurance, or SSDI, offers some coverage in the event of disability, but may not be adequate coverage for your profession. If you are in a labor union, check to see if they offer plans at negotiated rates to members. You can also purchase coverage from a licensed disability insurance broker or agent.

- How much coverage do you need?

- The amount of coverage you need depends on how much you make and how difficult it would be to make a similar amount if you became disabled. Some professions, such as surgeons, would find it very difficult to obtain a similar job if they became disabled and may need more coverage.

- How much does it cost?

- Disability insurance typically ranges in cost between 1% and 3% of your annual salary. The more coverage you need, the higher the cost.

Money Guy’s Take:

You have a higher chance of becoming disabled than dying at any given time, so it’s probably a good idea to have disability insurance. Your workplace policy may not be enough coverage for you.

Related videos, articles, and FAQs

Auto Insurance

Car insurance is likely required if you drive, but there are still different levels of coverage to consider. Although it may not be required, it is usually a good idea to carry uninsured motorist coverage.

- Where do you get it?

- You can obtain coverage online or through a licensed insurance broker or agent. If you have a poor driving history, some insurers may refuse to cover you or charge you significantly more.

- How much coverage do you need?

- Your car insurance policy is not just for you, but for all other drivers on the road you may interact with. Even if you are fine with paying for repairs to your vehicle out-of-pocket, you need to ensure you have adequate coverage in case you were to cause an accident that impacts others.

- How much does it cost?

- Car insurance varies drastically in price and depends on the amount of coverage, what type of car you drive, your driving history, age, and sex. The average cost in the US for full coverage is $223 per month and $67 for minimum coverage.

Money Guy’s Take:

You probably don’t need full coverage if your car is older, but we always recommend carrying uninsured motorist coverage if you can afford it.

Related videos, articles, and FAQs

- Comprehensive vs. Liability Car Insurance: Which Should You Buy?

- Year End Taxes & Investments, Auto Insurance Savings, & Variable Annuities

- 9 Ways to Lower Your Auto Insurance Bill

Pet Insurance

Pet insurance is not required, but if your pet could require expensive surgery or vet bills, pet insurance may be a good idea.

- Where do you get it?

- Not all insurers offer pet insurance while some specialize in it. Ask your vet if they have any pet insurance they recommend. Unlike human health insurance, you can typically go anywhere for services with pet insurance.

- How much coverage do you need?

- Many pet insurance policies offer add-ons for other potential issues that may not be included with standard insurance. If you’d rather have coverage in case your pet has more medical issues, you may want to select the appropriate add-ons.

- How much does it cost?

- Coverage is more expensive for dogs than for cats, and depending on the amount of coverage you choose, prices range from around $10 to $50 per month on average.

Money Guy’s Take:

Pet insurance may or may not be worth it, depending on the age and health of your pet and your risk tolerance. Many pet owners swear by pet insurance and find it very valuable.

Umbrella Insurance

Umbrella insurance provides additional liability coverage above the limits of your homeowners or auto insurance policies. It is often affordable and can be a good idea if you have substantial assets to protect.

- Where do you get it?

- You can obtain coverage online or through a licensed insurance broker or agent. You may be able to get cheaper rates if you bundle it with your homeowners, life, or car insurance policies.

- How much coverage do you need?

- Umbrella insurance serves to protect your assets, so the amount of coverage you need depends on your net worth, including your home equity, investment accounts, and other assets.

- How much does it cost?

- You can expect to pay around $150 to $300 for $1 million in coverage.

Money Guy’s Take:

If you have substantial assets, we recommend umbrella insurance.

Related videos, articles, and FAQs

Self Insurance

Self-insurance refers to the practice of setting aside money to cover potential risks instead of purchasing an insurance policy. This is usually only a viable option for those with significant assets.

Money Guy’s Take:

We generally recommend insurance over self-insurance for most risks. However, if you have substantial assets and can handle the risk, self-insuring can be a way to save money on premiums.

Travel Insurance

Travel insurance can cover unexpected costs that arise when traveling, such as trip cancellations, lost luggage, or medical emergencies.

Money Guy’s Take:

Travel insurance can be a good idea if your trip is expensive or involves potential risks, like international travel. However, if your trip is relatively low-cost or you can absorb the risk, it is usually not be necessary.

Related videos, articles, and FAQs

Renter’s Insurance

Renter’s insurance provides coverage for personal property and liability for renters.

- Where do you get it?

- You can get renter’s insurance through a traditional agent or broker or online. Some landlords may require coverage from a specific carrier.

- How much coverage do you need?

- Renter’s insurance can cover not only damage to the property you’re living in, but damage or loss of your belongings as well. Your landlord may have a minimum amount of coverage they require, but you can always opt for greater coverage.

- How much does it cost?

- The average cost of renter’s insurance is about $15 per month.

Money Guy’s Take:

Renter’s insurance is usually affordable and provides valuable protection, so we generally recommend it for renters.

Related videos, articles, and FAQs

Long-Term Care Insurance

Long-term care insurance covers costs associated with long-term care, such as in a nursing home or with in-home care services.

- Where do you get it?

- You can obtain coverage online or through a licensed insurance broker or agent.

- How much coverage do you need?

- Long-term care insurance policies can vary significantly in benefit amount, duration of coverage, covered medical conditions, and more. You may choose to opt for more coverage if you have a family history of illness at older ages or are generally in poor health yourself.

- How much does it cost?

- Long-term care insurance gets more expensive with age. Average costs can range from around $1,000 per year to over $12,000 per year.

Money Guy’s Take:

We recommend looking into long-term care insurance if you are in your 50s or 60s, as the costs of long-term care can be very high and Medicaid may not cover everything you need.

Related videos, articles, and FAQs

Identity Theft Insurance

Identity theft insurance covers the cost of restoring your identity if it’s stolen, including legal fees and lost wages.

Money Guy’s Take:

Identity theft insurance can be a good idea if you are at risk, but you may be able to get similar protection through other services or strategies, such as credit monitoring and freezing your credit.

Related videos, articles, and FAQs

Flood Insurance

Flood insurance covers damage caused by flooding, which is not typically covered by standard homeowners insurance policies.

Money Guy’s Take:

If you live in a flood-prone area, flood insurance is essential. Even if you don’t live in a high-risk area, it may be worth considering.

Is Insurance a Good Investment?

Copy link to this section: Is Insurance a Good Investment?

Copied the URL to your clipboard!

Copy link to this section: Is Insurance a Good Investment?

Copied the URL to your clipboard!

There is no shortage of people wondering if a permanent life insurance policy could offer tax benefits in retirement and provide for your family when you’re gone. As with nearly every great debate, there are three different camps: those who believe permanent life insurance makes a great investment, those who are strongly opposed to the idea of life insurance as an investment, and those who aren’t sure what to believe.

Life Insurance as an Investment

23% of Americans who purchase life insurance use it to build cash value and save for retirement. In other words, nearly a quarter of Americans with life insurance purchased a permanent policy because they were led to believe it is a good investment or a good way to save for retirement.

Is this true? Permanent life insurance can come with front-loaded sales charges, surrender charges, much higher premiums, and other fees and expenses. Permanent policies are often over 20x more expensive than comparable term life policies. Consumer Reports has estimated the annual rate of return for whole life insurance at 1.5%. Different insurance products with a component that “tracks the market” seem more exciting, but policies typically have participation rates, caps on returns, and fees.

Participation rates, or the amount of the “return” that you get to keep, are typically around 80%, with top-end caps that are normally in the high single digits, and expenses can vary greatly depending on administrative charges, fees, commissions, and surrender charges.

In a case study comparing the S&P 500 to a hypothetical indexed universal life insurance policy, with an 8% rate cap, 0% floor, 80% participation rate, and total expenses and fees of 1%, it underperformed the S&P 500 by nearly 8% annually over the last 40 years (the S&P 500 has annualized 12.01% over that period while the hypothetical IUL policy returned 4.22%). The selling point of these types of policies is that you can never lose money, unlike with the stock market, but they often fail to capture the majority of the upside of the market due to participation rates and caps on returns.

Why Do So Many Invest in Life Insurance?

In the financial services industry, most products can be categorized in one of two categories: those that sell themselves and those that require a great deal of work and persuasion to be sold. We fortunately have our fair share of financial investments that don’t require much, if any, work to be “sold” to consumers.

Index funds are low-cost investments with a long track record of positive returns, and an easy way to participate in ongoing economic expansion and innovation. Often all people need to be convinced to invest in a Roth IRA and/or low-cost index funds is education about how it works and the benefits it can provide in retirement. The historical returns, low fees and expenses, and long track record of performance speaks for itself.

On the other hand, there are some financial products that require a great deal of work to be “sold” to a customer. These products may not be in the best financial interest of the person being “sold” (but usually work out pretty well for the seller, with lucrative commissions and sales loads).

It is very difficult to get concrete historical returns for different life insurance policies, for good reason. The nicknames of products being sold change almost too frequently to keep up with (an “investment engine with death benefits” sounds a lot better than a permanent life insurance policy).

To put it frankly, some financial products continue being sold not because of the benefit to the consumer, but because of the benefit to the seller.

We’ve seen a countless number of influencers on social media that promote financial products that promise to lead their followers to financial abundance, but in reality exist to further enrich the seller of the product. These products are not limited to any single area of finance, and can be found in insurance, cryptocurrency, mutual funds, ETFs, and more.

Do I Need Life Insurance?

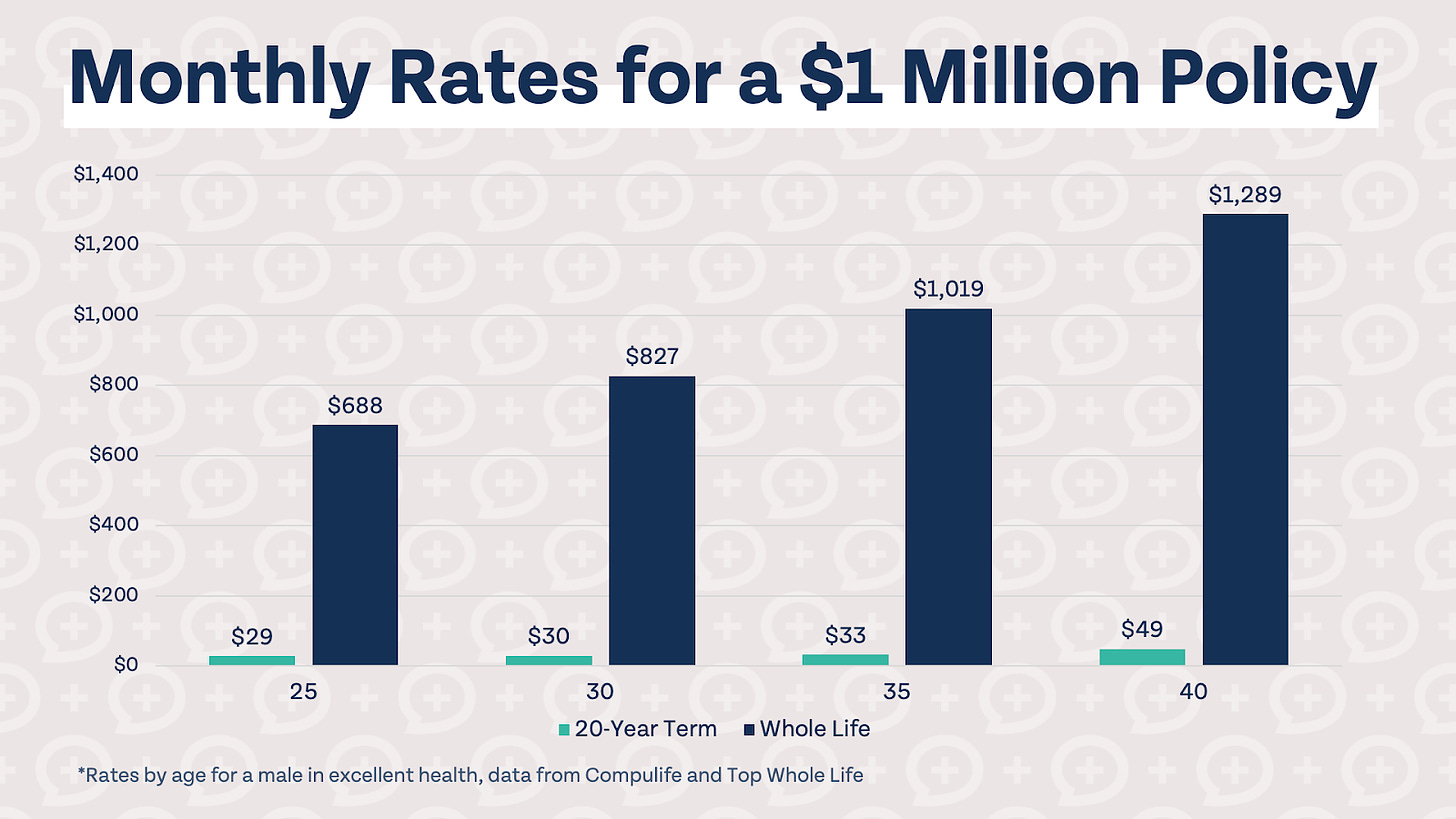

While we believe that permanent life insurance doesn’t make sense for everyone, and shouldn’t be viewed as a retirement investment vehicle, we are big fans of life insurance and of the protection it provides. Term life insurance policies offer protection for a period of time at an affordable cost. Check out the chart below of monthly premiums for a $1 million dollar policy, for a male in excellent health.

Share image

Term life insurance is pure insurance protection without any investment or cash value component. We believe it’s best to keep your insurance protection and investments separate. What do you think the insurance company does with the cash value portion of your permanent insurance policy? It’s invested in a mix of risk-on and risk-off assets. You can cut out the middleman, and sales charges, commissions, fees, and expenses, by investing directly in the market.

One of the arguments against term life insurance is that you are “throwing your money away” because the death benefit only covers a certain term. In fact, 99% of term life insurance policies never pay a death benefit to a beneficiary or beneficiaries.

This is not a downside, but a feature. Term life insurance is designed to cover a low-probability, high-impact event. Coverage is so affordable because it is unlikely you will ever receive a payout. This is a good thing! Never receiving a payout means you outlived your insurance policy.

Once your invested assets are large enough to pay off any debts and provide for your dependents, you may be able to self-insure. Term life insurance is meant to cover that period of time in your life when you have a need for life insurance (debts like a mortgage, and dependents, such as a spouse and children) and aren’t yet able to cover that need yourself.