-

▼

-

▼

What if your path to financial independence could be boiled down to just three numbers?

That’s exactly what we’re breaking down today — the three essential financial metrics you need to understand and optimize to accelerate your wealth-building journey.

✅ Why These 3 Numbers Matter

While personal finance involves many variables, these three key numbers act as your financial compass. They’ll help:

-

Guide your decisions

-

Track your progress

-

Set realistic financial goals

1. Burn Rate

Your burn rate is the total amount of money you spend each month. It includes:

-

Fixed Costs: Mortgage/rent, insurance, taxes, utilities

-

Variable Costs: Groceries, gas, entertainment, etc.

-

One-Off Costs: Occasional but necessary expenses like car maintenance or medical appointments

Why Your Burn Rate Matters:

-

It determines how much you can save each month

-

It influences how much you’ll need in retirement

-

It helps calculate your emergency fund (typically 3–6 months of expenses)

2. Your Number (Financial Independence Number)

Your financial independence number is how much you need invested to safely retire. This is calculated using the 4% Rule, which assumes you can withdraw 4% of your portfolio annually in retirement.

How to Calculate It:

Multiply your annual expenses by 25

OR

Divide your annual expenses by 0.04

Example:

-

Arvin spends $90,000/year → Needs: $2.25 million

-

Manny spends $75,000/year → Needs: $1.875 million

Note: This gives you a present-day estimate. It doesn’t factor in inflation but is useful as a general target.

3. Savings Rate

Your savings rate is the percentage of your income you save and invest each year.

Why It’s Crucial:

-

A higher savings rate shortens your time to financial independence

-

Lowering your burn rate increases your savings rate automatically

Example Comparison:

-

Arvin saves 10% of his $100k income → Takes 37 years to reach FI

-

Manny saves 25% of the same income → Reaches FI in just 22 years

Same income, different spending habits = drastically different outcomes.

Two Levers to Improve These Numbers

-

Spend Less:

-

Cut unnecessary expenses

-

Eliminate debt

-

Downsize housing or lifestyle if possible

-

-

Earn More:

-

Side hustles

-

Freelance work

-

Upskilling to earn promotions or higher-paying roles

-

Putting It All Together

Here’s your roadmap:

-

Track your burn rate – Know where your money goes each month

-

Calculate your FI number – Multiply annual expenses by 25

-

Boost your savings rate – Cut costs and increase income

Key Takeaway:

These three numbers — burn rate, FI number, and savings rate — work together to create a powerful plan for financial freedom. Optimizing even one of them can dramatically accelerate your journey.

Start today, be intentional with your money, and align every dollar with your goals. Small changes now can lead to big freedom tomorrow.

Enjoy the Show?

Where You Can Watch and Listen:

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

- Episodes of The Money Guy Show every Friday

- Episodes of Making a Millionaire every other Monday

- Mini-shows every Wednesday

- Ask Money Guy Livestreams every Tuesday

- Tons of other fun content!

What if I told you that your path to financial independence comes down to just three numbers? Guys, I am so excited about this because today we’re going to break down these three crucial financial metrics and how to optimize them to accelerate your wealth-building journey. Make sure to stick around until the very end because we’re actually going to put everything together to show you how you can use these three numbers to build wealth.

Now, of course, financial planning and ensuring that you have a solid plan in place will take more than just knowing three numbers because everyone has a different set of variables and circumstances that surround their financial life. But we can lay the groundwork for understanding your financial future by focusing on three key metrics that serve as the building blocks of any successful financial plan. You can think of these numbers as your financial compass—they’ll help guide you toward your goals and show you exactly where you stand on your journey to financial independence.

The first crucial number you need to understand is your burn rate. Think of your burn rate as the foundation of your financial planning journey—your financial footprint. This number includes everything from your mortgage or your rent payments all the way to your daily coffee runs. Understanding your burn rate is absolutely essential because it directly influences both how much you can save and how much you will need in retirement. Your burn rate is basically the amount of money that goes out the door on a monthly basis.

You can break this down into a few categories. First, you have your fixed costs—these are predictable expenses like taxes, mortgage or rent, insurance premiums, and maybe even utility bills that remain relatively stable from month to month. Then there are your variable expenses—these are things like groceries and gas, which can fluctuate based on your lifestyle choices and your circumstances. While these costs may vary, you can typically find a reliable average by just looking at your spending over the past couple of months. And then lastly, these are your one-off expenses that crop up—things like an oil change or maybe a dentist appointment. These are relatively small expenses that aren’t necessarily emergencies but need to be accounted for in a budget.

When you add up all of these expenses—the fixed costs, the variable expenses, and the one-offs—you get your total burn rate. While it can be helpful to break these categories down to better understand and track your spending, what really matters, at least for purposes of today, is the total monthly amount that’s going out the door. This comprehensive number forms the foundation for all of our other financial calculations.

Understanding your burn rate in particular is valuable because it serves multiple purposes in your financial journey. For starters, it determines how big your emergency fund should be—a crucial first milestone on your path to financial independence. We typically recommend having around 3 to 6 months of expenses saved. But more importantly, burn rate plays a vital role in calculating your number for financial independence, since your investment portfolio will ultimately need to generate enough income to replace your monthly expenses.

And your number is actually the second number of the three important financial metrics you need to know. The concept of your number, or the amount you need for financial independence, is simple but incredibly powerful. By understanding this, you can begin charting a clear course toward your financial goals and can begin making informed decisions about both your saving and investing strategies.

All right, now let’s explore how you can calculate your number—the amount that you’ll need to achieve financial independence, at least the easy back-of-the-napkin way. This calculation is rooted in what’s known as the 4% rule, a widely accepted principle in financial planning. The 4% rule suggests that you can safely withdraw 4% of your investment portfolio each year in retirement, with a high probability that your money will last for at least 30 years. This means to generate the income you need in retirement, you’ll need a portfolio that’s roughly 25 times your annual expenses, since 4% is really just 1/25 as a fraction.

To illustrate this, let’s look at two examples. We’re going to assume we have two investors: Arvin and Manny. Both have an income of $100,000. Arvin, after taxes, fixed expenses, and everything else, spends $7,500 a month or $90,000 a year. So if we use the 4% rule, we can determine that a good estimate for his financial independence number would be $90,000 × 25 or $90,000 ÷ 0.04, which equals $2.25 million. Manny, on the other hand, has a burn rate of $75,000. That means that using that same 4% calculation, he only needs around $1.9 million.

It’s important to note that this isn’t factoring in inflation—like how much they need in today’s dollars in the future—but it does give you sort of a rough estimate of what your endpoint needs to be, or at least what it would be if you were retiring today. You can see that these small decisions—maybe living in a cheaper apartment or not driving as nice of a car—can have dramatic differences. And not only does Manny need less to be financially independent than Arvin, he actually gets there a whole lot faster.

Remember, Arvin’s burn rate is $90,000 a year, which means he’s only able to save 10% of his income of $100,000, so he’s only saving $10,000 a year. At this savings rate, assuming an 8% annual rate of return, it would take almost 37 years for Arvin to reach financial independence. Manny, on the other hand, has a burn rate of $75,000 a year, meaning with those same assumptions he can save 25% of his income. Compounded at 8% over his working career, he actually reaches his financial independence number in 22 years—that’s 15 years less than Arvin.

What makes these examples particularly powerful is that in both cases we’re looking at two individuals with the exact same income. The only difference is how they manage their money. By reducing your burn rate from 90% to 75%, you achieve a double benefit: you increase your savings rate while simultaneously decreasing your lifestyle—or how much you’ll eventually need for retirement. This combination creates a powerful accelerator that can cut years or maybe even decades off of your journey to financial independence.

This comparison reveals a powerful truth about the relationship between your burn rate and your savings rate. Realistically, they’re just two sides of the same coin. Every dollar that you don’t spend—your burn rate—becomes a dollar that you can save—your savings rate. Manipulating each of these numbers is where the real magic happens.

There are two main levers you can pull to optimize both your burn rate and your savings rate. The first is simply spending less. This could mean cutting back on unnecessary expenses, eliminating debt to reduce your burn rate, or maybe even downsizing in retirement so you only need to replace a portion of your current burn rate. The second lever you can pull is earning more, which becomes particularly important once you’ve optimized your spending. Because after all, there’s only so much we can cut out of our budgets—but in theory, your income can be scaled infinitely with side hustles, freelancing, or other income sources.

So these three metrics—your burn rate, your number, and your savings rate—work together to form a comprehensive picture of your financial health. Your burn rate determines your free cash flow and how much you’ll need in retirement. Your retirement number gives you a clear target to aim for, calculated based on your annual expenses. And your savings rate determines how quickly you can get from where you are today to that target.

To put these numbers into action, start by tracking your expenses to understand what your burn rate is. Then use that burn rate to calculate your retirement number by multiplying it by 25 or dividing it by 0.04. It won’t be a perfect calculation, but it can be a helpful approximation—at least to give you somewhat of a goal. Finally, optimize your savings rate by finding opportunities to reduce expenses and increase income.

Remember, even small improvements in these numbers can drastically accelerate your journey to financial independence. By consistently monitoring and optimizing these three numbers, you will have a clear roadmap to guide your financial decisions and track your progress toward financial independence. Start today by calculating your own numbers and identifying which areas you can make improvements in. Remember, the goal isn’t to be a miser—it’s about being intentional in spending your money and making sure every dollar aligns with your values and your long-term goals.

When you optimize these three numbers—your burn rate, your retirement number, and your savings rate—you create a financial rocket ship that can dramatically accelerate your journey to financial freedom. With that, we hope now you feel empowered to know the three numbers that you need to know for a great big beautiful tomorrow. Be sure to leave a like, subscribe if you haven’t already, and we’ll see you in the next one.

Free Resources

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

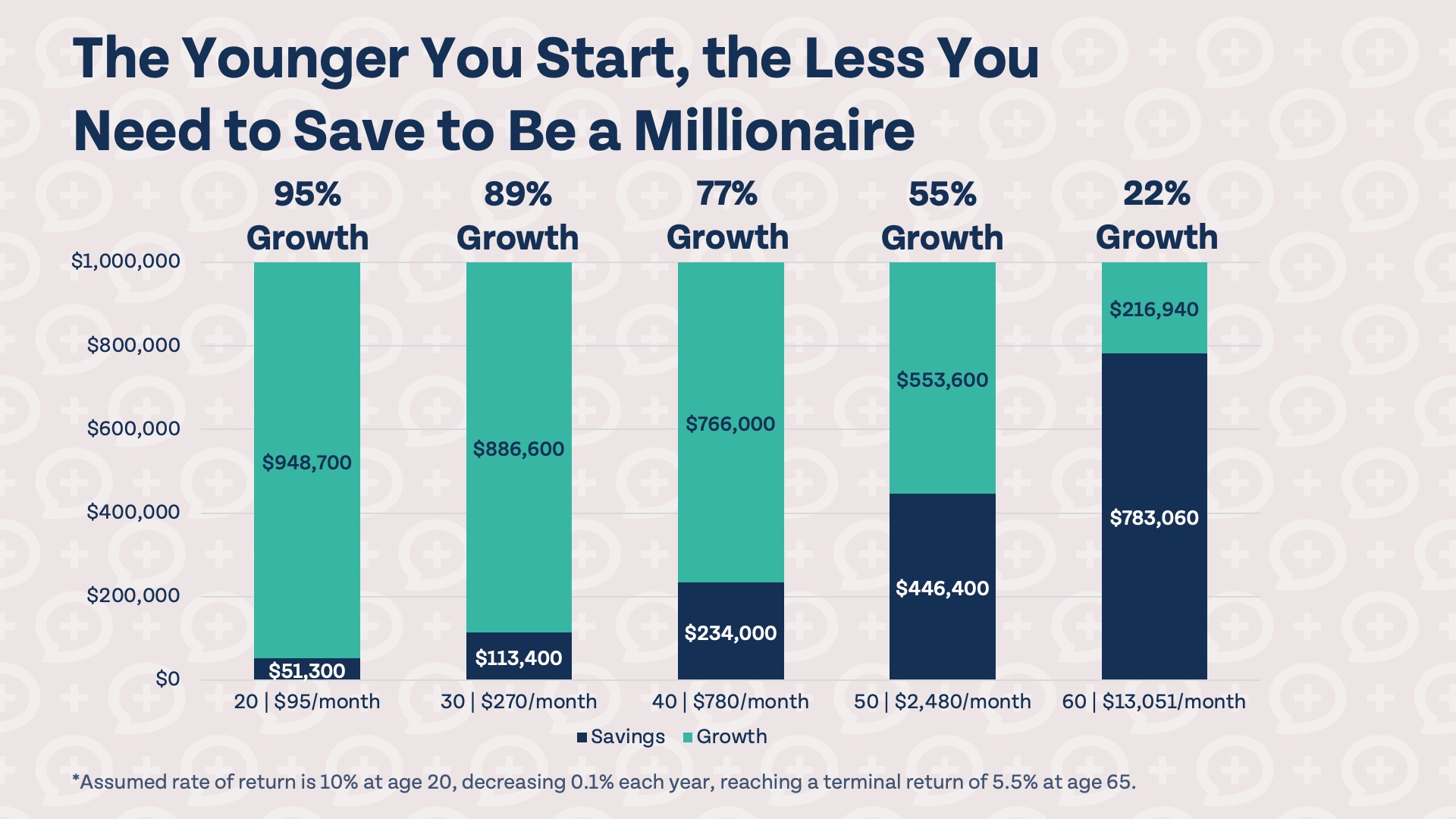

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

Articles

How Much Do You Actually Need To Retire?

Believe it or not, the concept of saving for your own retirement is a fairly recent creation. Brian, our Money Guy, predates the 401(k) plan....

Articles

What Is the Current State of Real Estate Investing? with Dave Meyer of BiggerPockets

We are so excited to welcome Dave Meyer of BiggerPockets joins us to discuss tips for investors, the housing market, and his new book. Want...

Articles

Should We Switch to S&P Before Hiring a Financial Advisor?

My wife and I are 20+ years from retirement. We are close to where we hire a financial advisor within 2 years. All $250k is...

Financial FAQs

Courses & Tools

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Recent Episodes

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

These Money Moves Feel Like Financial Cheat Codes

Want to build wealth faster without taking unnecessary risks? We break down seven financial "cheat codes" that can dramatically improve your long-term finances and help...

Episodes

Do You Really Have To Budget Forever?

Do you need to budget forever? Brian explains when to graduate to cash flow management & focus on what can help you move the needle...

Episodes

Should You Die With Zero?

Is Die With Zero actually good advice? We break down the book, the risks of under-saving, and how to enjoy money today without wrecking your...