-

▼

-

▼

I did a show back in January titled “The ABCs of Asset Allocation”, but many things have changed over the last 9-10 months. We have added quite a few listeners and many have sent me emails looking for specific discussion on asset allocation. My last show was on the basics of investing, so I think the timing is right to work on your allocation knowledge.

Terms needed to understand asset allocation:

Domestic Stocks = US Companies

Market Capitalization of US Stocks (According to MorningStar®):

Large Cap = US Companies with a Market Cap greater than $11 Billion (these are the companies that are household names like Wal-Mart, GE, Home Depot, Coca-Cola, Pfizer, and so forth)

Mid Cap = US Companies with a Market Cap between $2-$11 Billion (these are companies that you might have heard of like HR Block, but are not the size of the previous listed group.

Small Cap = US Companies with a Market Cap below $2 Billion. Probably not going to recognize the small company unless you specifically use their product or they are in your town.

International Stocks = Obviously companies that are based outside of the United States. Examples include: Nestle (Switzerland), Lafarge (France), GlaxoSmithKline (UK), Mitsubishi (Japan)

Value Stocks vs. Growth Stocks (according to about.com):

Value = Stocks that are under priced by the market for reasons that have nothing to do with their businesses. Often a stock’s only sin is not being a part of the current hot sector. Typically have a low price earnings ration (P/E), more equity than debt on their balance sheets, and current assets are twice current liabilities. (For an example of a Value stock lets look at Dodge & Cox Stock Fund’s top holding according to MorningStar®: Hewlett-Packard Company (PE = 20.46))

Growth = Stocks that have projected or historic strong growth rates, return on equity, and earnings per share (EPS). (For an example of a Growth stock lets look at Fidelity Contrafund’s top holding according to MorningStar®: Google Inc.(PE = 46.17)).

The easiest way to determine the style of a stock or mutual fund is to look it up at www.Morningstar.com

MorningStar® takes into account company valuations and other factors to determine the asset class of the holding.

Now that we know a few terms how do you make them work for you?

First where are you in the saving stage?:

If you are just starting out and have not built up a nest egg over $200,000 I think you should consider sticking to one of the good Fund of Funds investments. Both Fidelity and Vanguard now offer target retirement funds. With these funds you determine what year you think that you will retire and then purchase the fund that has the same target date. These fund’s are great in the fact that they automatically adjust the allocation based upon how close you are to retirement (obviously more risk in early years with much safer investments as you approach your retirement date). There is a downside to target funds… their diversification is limited to Stocks, Bonds, and Cash Equivalents. This is ok as you start out, but after you build a sizable asset base I think you need other allocation choices such as Real Estate, Absolute Return Strategies, and Commodities to complete your investment allocation.

For those looking for the cheapest game in town consider the following index funds from Fidelity or Vanguard. Fidelity’s Four In One Index (FFNOX) or Vanguard Total Stock Index Fund (VTSMX). These simple choices offer basic diversification with no commissions and practically free of any internal fees. However, just like the target retirement funds their diversification is limited to Stocks, Bonds, and Cash.

For those that have built up some holdings¦ The basic asset classes I use in portfolio management include: Domestic Stocks, International Stocks, Fixed Income (Bonds), Commodities (Natural Resources, Oil & Gas Holdings), Real Estate (Both Domestic and International), Absolute Return Strategies (Hedge Funds), and of course Cash Equivalents.

A hypothetical individual with a moderate tolerance for risk might have the following allocation (remember that this is an example… I do not know your personal situation or your personal risk profile including existing assets, age, and goals… in other words this is not a personal recommendation).

Cash & Equivalents = 5%

Fixed Income = 15%

Absolute Return Strategies = 20%

Domestic Stocks = 38%

International Stocks = 16%

Real Estate = 2%

Commodities = 4%

Cash = Since a good money market fund is yielding around 5% you do not have to feel as guilty about having a portion of your money in unsexy cash

Fixed Income = The Federal Reserve recently reduced interest rates by 1/2%, so the Intermediate and Long-Term Bonds benefited but the Short-Term Bonds lost value. I would consider finding a good Total Return Bond Fund that covers many types of fixed income and then I would also consider some of the Inflation Protected Bonds. It is interesting to note that when I did this show back in January we had an inverted yield.

Absolute Return Strategies = This class use to be reserved for only the wealthiest individuals, but now anyone can invest in this unique investment class through mutual funds. MorningStar® even added a new category (Long-Short) to cover this type of investment. Make sure you pay attention to the risk of the investments. I prefer the conservative funds with limited risk.

Domestic Stocks = 50%-70% of your exposure to this investment class should be in large cap holdings. I personally like ETFs and Index Funds for Large Cap Investing. Mid and Small Cap exposure is trickier because you need a good manager and the good ones close their doors quickly to new investors because of their popularity.

International Stocks = The lion share of your investment will be in large European countries, but you may also want to spice up this asset class with some exposure to Emerging Markets like Latin America and Asia. Be careful of your risk profile because International holdings especially Emerging Markets can be very volatile.

Real Estate = This asset class is currently getting hammered, and I am not so sure that the bottom has been found. Back in January I warned, “I have been calling for a pull back in REITs and RE mutual funds for the last 2.5 years, but they keep appreciating. Be careful here because you do not want to top the market.” It is nice when your past thoughts turn out to be accurate, but let’s face it you did not have to be a genius to see that the Real Estate was overheated. International Real Estate opportunities have increased in the last two years and have performed well, and may be a good diversifier since Domestic Real Estate is still trying to find firm ground.

Commodities = Man what a run that oil/gas and natural resources have had so far in 2007. I have dialed this allocation holding back just a bit in light of the $80/barrel price that oil has reached recently. I am hoping that if we have a mild winter and the world does not have any global disruptions we can find another buying opportunity between now and Feb of 2008. To see what a big difference 9-10 months makes review what I said back in January, “This may not be a bad time to add a limited exposure to this asset class. We all know that last year oil prices ran up to $78/barrel and I not so sure I feel that the world is stable enough to sustain low $50s for a barrel of oil.” Natural Resource funds that not only invest in Oil/Gas, but also other natural resources can help spread your exposure in this asset class.

I did a show back in January titled “The ABCs of Asset Allocation”, but many things have changed over the last 9-10 months. We have added quite a few listeners and many have sent me emails looking for specific discussion on asset allocation. My last show was on the basics of investing, so I think the timing is right to work on your allocation knowledge.

Terms needed to understand asset allocation:

Domestic Stocks = US Companies

Market Capitalization of US Stocks (According to MorningStar®):

Large Cap = US Companies with a Market Cap greater than $11 Billion (these are the companies that are household names like Wal-Mart, GE, Home Depot, Coca-Cola, Pfizer, and so forth)

Mid Cap = US Companies with a Market Cap between $2-$11 Billion (these are companies that you might have heard of like HR Block, but are not the size of the previous listed group.

Small Cap = US Companies with a Market Cap below $2 Billion. Probably not going to recognize the small company unless you specifically use their product or they are in your town.

International Stocks = Obviously companies that are based outside of the United States. Examples include: Nestle (Switzerland), Lafarge (France), GlaxoSmithKline (UK), Mitsubishi (Japan)

Value Stocks vs. Growth Stocks (according to about.com):

Value = Stocks that are under priced by the market for reasons that have nothing to do with their businesses. Often a stock’s only sin is not being a part of the current hot sector. Typically have a low price earnings ration (P/E), more equity than debt on their balance sheets, and current assets are twice current liabilities. (For an example of a Value stock lets look at Dodge & Cox Stock Fund’s top holding according to MorningStar®: Hewlett-Packard Company (PE = 20.46))

Growth = Stocks that have projected or historic strong growth rates, return on equity, and earnings per share (EPS). (For an example of a Growth stock lets look at Fidelity Contrafund’s top holding according to MorningStar®: Google Inc.(PE = 46.17)).

The easiest way to determine the style of a stock or mutual fund is to look it up at www.Morningstar.com

z

MorningStar® takes into account company valuations and other factors to determine the asset class of the holding.

Now that we know a few terms how do you make them work for you?

First where are you in the saving stage?:

If you are just starting out and have not built up a nest egg over $200,000 I think you should consider sticking to one of the good Fund of Funds investments. Both Fidelity and Vanguard now offer target retirement funds. With these funds you determine what year you think that you will retire and then purchase the fund that has the same target date. These fund’s are great in the fact that they automatically adjust the allocation based upon how close you are to retirement (obviously more risk in early years with much safer investments as you approach your retirement date). There is a downside to target funds… their diversification is limited to Stocks, Bonds, and Cash Equivalents. This is ok as you start out, but after you build a sizable asset base I think you need other allocation choices such as Real Estate, Absolute Return Strategies, and Commodities to complete your investment allocation.

For those looking for the cheapest game in town consider the following index funds from Fidelity or Vanguard. Fidelity’s Four In One Index (FFNOX) or Vanguard Total Stock Index Fund (VTSMX). These simple choices offer basic diversification with no commissions and practically free of any internal fees. However, just like the target retirement funds their diversification is limited to Stocks, Bonds, and Cash.

For those that have built up some holdings¦ The basic asset classes I use in portfolio management include: Domestic Stocks, International Stocks, Fixed Income (Bonds), Commodities (Natural Resources, Oil & Gas Holdings), Real Estate (Both Domestic and International), Absolute Return Strategies (Hedge Funds), and of course Cash Equivalents.

A hypothetical individual with a moderate tolerance for risk might have the following allocation (remember that this is an example… I do not know your personal situation or your personal risk profile including existing assets, age, and goals… in other words this is not a personal recommendation).

Cash & Equivalents = 5%

Fixed Income = 15%

Absolute Return Strategies = 20%

Domestic Stocks = 38%

International Stocks = 16%

Real Estate = 2%

Commodities = 4%

Cash = Since a good money market fund is yielding around 5% you do not have to feel as guilty about having a portion of your money in unsexy cash

Fixed Income = The Federal Reserve recently reduced interest rates by 1/2%, so the Intermediate and Long-Term Bonds benefited but the Short-Term Bonds lost value. I would consider finding a good Total Return Bond Fund that covers many types of fixed income and then I would also consider some of the Inflation Protected Bonds. It is interesting to note that when I did this show back in January we had an inverted yield.

Absolute Return Strategies = This class use to be reserved for only the wealthiest individuals, but now anyone can invest in this unique investment class through mutual funds. MorningStar® even added a new category (Long-Short) to cover this type of investment. Make sure you pay attention to the risk of the investments. I prefer the conservative funds with limited risk.

Domestic Stocks = 50%-70% of your exposure to this investment class should be in large cap holdings. I personally like ETFs and Index Funds for Large Cap Investing. Mid and Small Cap exposure is trickier because you need a good manager and the good ones close their doors quickly to new investors because of their popularity.

International Stocks = The lion share of your investment will be in large European countries, but you may also want to spice up this asset class with some exposure to Emerging Markets like Latin America and Asia. Be careful of your risk profile because International holdings especially Emerging Markets can be very volatile.

Real Estate = This asset class is currently getting hammered, and I am not so sure that the bottom has been found. Back in January I warned, “I have been calling for a pull back in REITs and RE mutual funds for the last 2.5 years, but they keep appreciating. Be careful here because you do not want to top the market.” It is nice when your past thoughts turn out to be accurate, but let’s face it you did not have to be a genius to see that the Real Estate was overheated. International Real Estate opportunities have increased in the last two years and have performed well, and may be a good diversifier since Domestic Real Estate is still trying to find firm ground.

Commodities = Man what a run that oil/gas and natural resources have had so far in 2007. I have dialed this allocation holding back just a bit in light of the $80/barrel price that oil has reached recently. I am hoping that if we have a mild winter and the world does not have any global disruptions we can find another buying opportunity between now and Feb of 2008. To see what a big difference 9-10 months makes review what I said back in January, “This may not be a bad time to add a limited exposure to this asset class. We all know that last year oil prices ran up to $78/barrel and I not so sure I feel that the world is stable enough to sustain low $50s for a barrel of oil.” Natural Resource funds that not only invest in Oil/Gas, but also other natural resources can help spread your exposure in this asset class.

Enjoy the Show?

Where You Can Watch and Listen:

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

- Episodes of The Money Guy Show every Friday

- Episodes of Making a Millionaire every other Monday

- Mini-shows every Wednesday

- Ask Money Guy Livestreams every Tuesday

- Tons of other fun content!

Free Resources

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

Articles

Are Index Funds Still Better Than Active Funds in 2025?

Over longer periods of time, index funds tend to outperform actively managed funds in most categories. Recently, total assets in index funds have surpassed the...

Articles

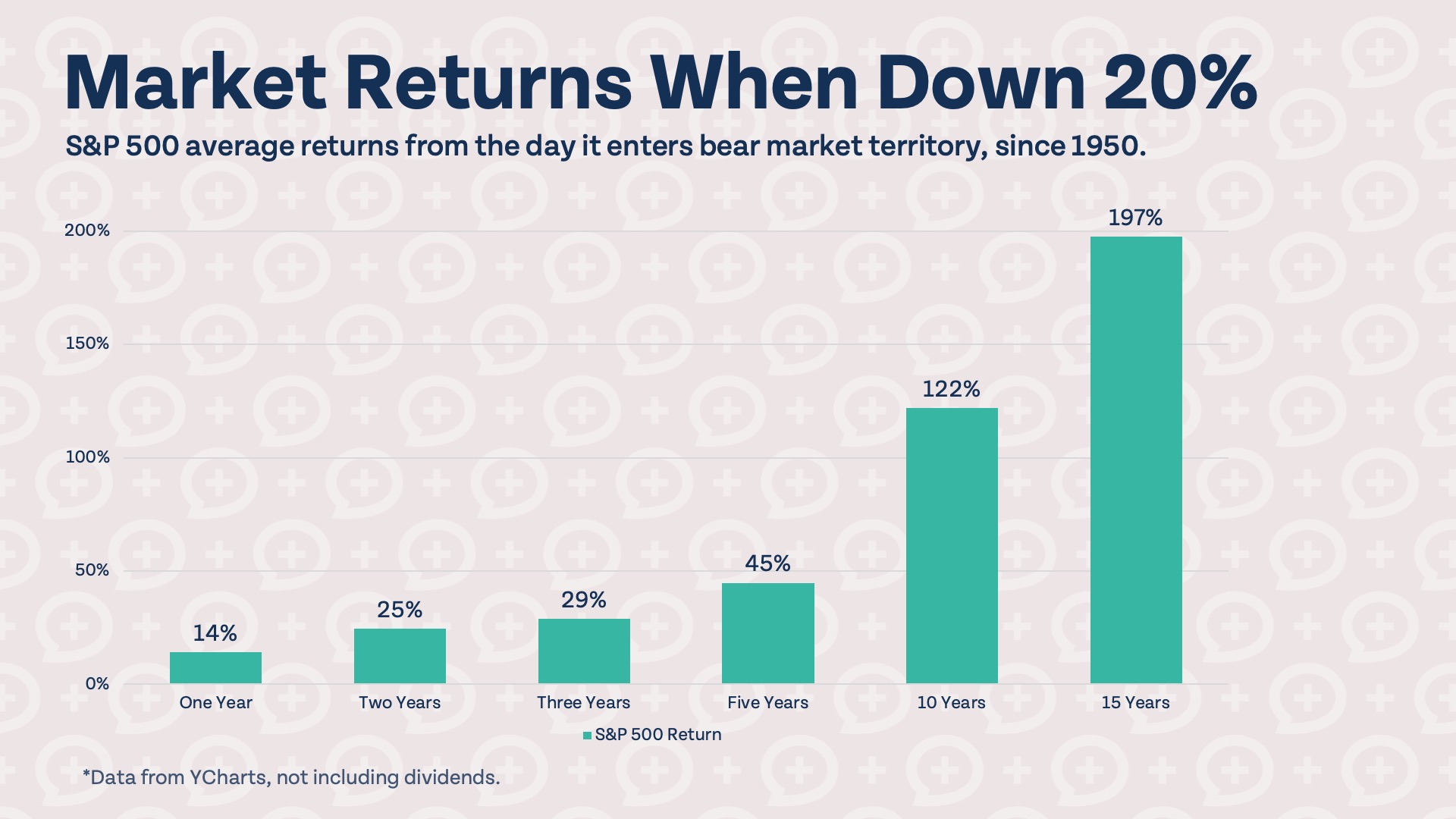

What To Do When the Stock Market Is Down

The S&P 500 is down nearly 15% from its highs earlier this year, inching closer to bear market territory. While it may not be wise...

Articles

How To Prepare for a Bear Market in 2025

The Nasdaq stock market index is in correction territory, down over 10% from recent highs. The other major US indexes, the S&P 500 and Dow,...

Financial FAQs

Courses & Tools

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Recent Episodes

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

Financial Advisors Correct the Internet (Part 2)

Is viral financial advice doing more harm than good? In this react episode, we correct the internet once again and separate the news from the...

Episodes

These Money Moves Feel Like Financial Cheat Codes

Want to build wealth faster without taking unnecessary risks? We break down seven financial "cheat codes" that can dramatically improve your long-term finances and help...

Episodes

Do You Really Have To Budget Forever?

Do you need to budget forever? Brian explains when to graduate to cash flow management & focus on what can help you move the needle...