-

▼

-

▼

Death and taxes, everybody’s favorite subjects, right? There’s plenty of tax advice online. Some is brilliant, some is dangerous, and some is just hilarious. We react to the internet’s best and worst tax advice, from W-4 withholding formulas to Monopoly kids crying about taxes and more.

Discover which strategies actually work, which are too good to be true, and which could land you in serious trouble with the IRS. Remember the critical difference between tax avoidance (Okay!) and tax evasion (NO way!) when planning your financial roadmap.

Plus, check out our 2026 Tax Guide and our Ultimate Guide for Tax Planning Strategies to learn our favorite tax planning strategies that apply to just about anybody looking to reduce taxable income and save money every year.

Enjoy the Show?

Where You Can Watch and Listen:

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

- Episodes of The Money Guy Show every Friday

- Episodes of Making a Millionaire every other Monday

- Mini-shows every Wednesday

- Ask Money Guy Livestreams every Tuesday

- Tons of other fun content!

Introduction – Internet Tax Advice (0:00)

Brian: Death and taxes. Everybody’s favorite subject. So, why not make it as fun as possible?

Bo: Brian, I am so excited about this. Is death really people’s favorite? Okay, whatever. I’m so excited about this because right now the internet is going to tell us what we need to know about our tax system. Let’s dive right in.

W-4 Withholding Strategy (0:19)

Video Clip: Is there a magic formula or some way to figure out how many you can claim on your W-4 so you get the smallest tax return back? There’s a formula, but it’s not based on the number of dependents because the IRS tables are wrong, of course. Okay. So, um, thus you, you know, you can claim like for instance, my daughter when she first got out of college claimed six dependents. She didn’t even have one and it still got her a refund. Okay? So, she still didn’t have enough coming out. So, that’s how bad the tables. They’re not minorly off. They suck. The way you would do it is one of two ways. The most accurate way is to actually do a fake tax return for the year. Actually prepare your tax return and let it tell you exactly what you would owe in taxes, your total tax bill, and then divide that by the number of months and that’s what needs to come out of your check per month. And so if your actual tax bill is $4,800, then $400 a month needs to come out, right?

Bo: Dave said that when his daughter graduated, she had like six dependents and it still got her a refund. Well, yeah, the more dependents you claim, the less taxes they withhold. She should have claimed zero dependents and she didn’t want to get a refund. So, it makes sense that she still got a refund because I think she likely did it wrong. Now, I know W-4 forms, they’ll kind of walk you through. Okay, answer this question. Answer this question. Answer this question. And I do think that Dave is right. You can do a tax projection. You can arrive at what you think your tax bill is going to be and you can reverse engineer your withholding, but a lot of people don’t know how to do that. So, what I would say is this year when you do your taxes, pay close attention. Do I owe a big amount? If that’s the case, I probably need to increase my withholding or if I get a big refund, maybe I need to decrease my withholding. And I would do it that way rather than trying to go out and figure out, okay, well, how do I do a tax projection? How do I do that if that’s not something that’s sort of in your wheelhouse?

Brian: The hassle factor is high for the way Dave laid this out. I think it’s the right way, but I wouldn’t do it this way. Here’s what I would do. First year you get a job, actually fill out the form the way it is. If you’re married, put married. And you can still check a box that says, “Hey, but I want to be treated as single because I want to have the maximum amount withheld.” If you think you’re going to get a refund, you don’t have to check that box and it’ll claim both. And then when you do your taxes in that first year, pay attention. If there’s a huge refund, you immediately know you need to go do a new W-4, change the numbers, and then grip and rip and let it go until the next tax season.

Monopoly Kid Crying About Taxes (2:46)

Video Clip: Where’s all your money gone, daddy? Taxes. Uh-oh. He’s crying. Let me fix my houses. Bug. It’s okay. It’s part of the game. Monopoly. It’s not fun to what? It’s the worst part of the game. Oh, it’s what? Taxes.

Bo: Amen, brother. You got it. How many times, Brian, have you sat down with a small business owner, they launch their first business, they start their first side gig, and maybe they’re not laying in front of the couch crying at the same realization. Holy cow, why on earth do I owe so much taxes? I finally just made my business profitable. It is something that if you do not plan for it and don’t know that it’s coming, you may also find yourself in tears.

Brian: Probably a proud parent moment, though. Like, okay, he’s going to be a hard worker and not want to pay taxes. He’s an American.

Never Pay Tax Again Strategy (3:39)

Video Clip: Here’s how to never pay tax again. So, this is what I would do if I was solely basing my decisions off of tax and nothing else. First, I would become a real estate professional under IRS definitions because they receive by far the best tax advantage. Second is I would purchase real estate. And third is whenever I sell the real estate, I would only do 1031 exchanges so that the capital gains is deferred. And finally, what I would do is you could borrow against that property to use that cash to live off of. And then I would only transfer the real estate by leaving it in my will or in my estate, not by gifting it while I’m alive, so that the people that receive it get a step up in basis. And as long as you’re under that estate tax threshold of 11 million per person, that’s your tax-free formula.

Bo: Look, it’s true. What she laid out is accurate. Now, one of the things if you’re going to perpetrate the strategy, you have to be comfortable always being in debt. Because you heard where her cash flow comes from is borrowing the equity out of the properties that she has and then she does a 1031 and she exchanges, she borrows the equity out and borrows the equity out. So you’re never actually going to have like a really impressive looking net worth statement because your liability column is always going to be substantial. But she is correct that is a way to not pay tax.

Brian: Here’s the thing. She did say something that’s very true and I’ve often thought this is like the lobbying arm of the real estate professionals is pretty spectacular because a few years ago when they came out with the small business exclusion, the QBI business exclusion where essentially 20% of small business income doesn’t get taxed, they excluded most professionals. Like if you go out there and look at your CPAs, your attorneys, your financial advisors, your doctors, they don’t get the small business exclusion on their stuff because they’re considered professionals. But guess which professionals somehow got carved out of it? It was real estate professionals. It was architects. It’s amazing. It’s almost like they helped write the legislation.

Cost Segregation Paper Loss Strategy (5:44)

Video Clip: Here’s how you can avoid 100% of your income taxes every single year. We call this strategy the paper loss strategy. In order to use it every single year, you have to understand the rules. The very first thing that I’m going to need you to understand is you’re going to need to buy an investment property. When you buy a rental property, it could be an Airbnb or it can be a long-term rental. But as soon as you purchase the property, I want you to write off everything that’s on the inside of the property. This could be appliances, bathrooms, tubs, cabinets. And when you write off everything that’s inside of the property, it creates a big expense. We call this the cost segregation study. Once you do the cost segregation study, it creates a big enough loss to offset your W-2, your 1099, your stock, and your crypto income, making you tax-free.

Brian: You don’t see a lot of people doing cost segregation on residential, but on commercial property for sure. We’ve even done cost segregation on real estate that we’ve bought. But the thing is you have to be a real estate professional to be able to take it against W-2 and ordinary income. It’s not the easiest test to pass. You can’t just on your tax return say hey I’m a real estate professional, give me all these benefits. I think a lot of people are going to be like uh-oh because the IRS is going to call you on that.

Bo: Yeah. I think Carlton what happens for most folks is they buy the property, they do cost seg study, get all those expenses front loaded. And what you have is you have losses against the passive income on that property for a few years, which is great, but it likely is not going to offset the other income sources if you do have W-2 income or investment income. It’s only going to serve to offset the income applicable to that type of property, that type of investment.

Brian: Yeah. I mean, most people it’s just going to be a big carry forward. That’s what especially, you know, a lot of people get into residential rental thinking they’re going to be able to write off everything. And then you find out, wait a minute, I make more than like was it $150,000. You’re like, “Oh, I’m going to have to carry this loss forward until I actually sell the property.” Like, “What the heck did we even do this for?”

Tax Refunds Aren’t Free Money (7:43)

Video Clip: Hello. Hey, I can’t come in to work today. Is everything okay? I can’t see. You can’t see something wrong with your vision? No, I can’t see myself working today. Bye.

Bo: Huh? So, I think it’s great. A lot of people, they get a big tax return, they get a big tax refund, and they’re like, “Boom, I’m rich. Look at all of this free money the government just gave me. I’m loaded now.” And I think what they don’t recognize is the government didn’t give you money. They didn’t say, “Hey, you know what? Congratulations on filing your taxes.” All they did was give you back money that was already supposed to be yours. So, if you’re someone who’s getting a big refund and that money comes back to you, I would not treat it as found money. I would treat it as money that you loaned the government interest free for the last year.

Brian: All that video did was make me feel old.

Bo: Elaborate.

Brian: I was trying to pay attention thinking I was actually going to hear something there and I was like, “Oh, is this like a video meme?” You know, because it had tax return, big refund, and then okay, enjoy it. Then you put the voice over. There was just a lot going on that I just didn’t completely get. I guess it’s like a joke and I just, it wasn’t funny to me. I’m sorry. I can tell it was funny to you though. So that’s all right. It’s a generational video meme. Maybe we should just…

Business Owner vs. W-2 Employee (9:00)

Video Clip: Here’s the problem with earning six figures as an employee. At 100K, you’re in the top 3%. And after taxes, that hard earned salary can leave you with just 65K. Instead, imagine earning six figures as a business owner. You can write off expenses like the latest gadgets and business trips abroad, allowing you to keep more of what you earn. That’s why owning a business beats earning six figures any day.

Brian: Well, okay. Look, I feel like I’ve got it on both sides in that we have lots of employees, but I’ve also been an employee and then I’ve been a business owner. It is true. There’s a few more things that are more deductible, but there’s also a lot more things that cost.

Bo: That’s right. Entrepreneurship is wonderful and it’s a great thing if that’s something that makes sense for you, but it’s not for everyone. And I would argue that there are a lot of people out there, if you compared someone who makes $100,000 of a W-2 salary versus a business owner that has $100,000 in revenue, depending on the business, that W-2 salary might actually have more money than that business owner. So just because you’re a W-2, just because you collect a paycheck, doesn’t mean that that’s necessarily a bad thing. You should try to figure out how to go out on your own.

Brian: I think entrepreneurship is somewhat of a calling. If you’re doing it because of tax savings, you’re probably not starting a business for the right reason. Believe me, it takes more than just tax savings. You need passion. You need cash reserves. You need to have talent that actually is so marketable that you get rewarded for bringing this out to the public.

Sheltering 66% of Income (10:26)

Video Clip: Here’s a quick way to shelter 66% of your income legally. I’m Tyler. I’m a former financial advisor and portfolio manager. Now, I make financial content for free so that you don’t have to pay for it. Let’s say I make $75,000 a year pre-tax. Number two, I would start by putting $4,150 bucks in a health savings account, above the line deduction. Number three, next I’d put $7,000 into a traditional IRA, above the line deduction, and we’re rolling. Number four, next I’d put $23,000 into my traditional 401(k) pre-tax contribution. Number five, then I’d cap it off by taking the single filer deduction of $14,600 bucks. Number six, and I’d turn around and tell the government that I officially made $26,250 bucks of taxable income. Went from the 22% to the 12% tax bracket at this rate and projected to be a millionaire in just under 14 years.

Bo: And there’s one thing I would change, and I have to think through this. I’d want to look at the taxes, but I’d rather do a Roth IRA. I love maxing out the 401(k), but imagine if he did Roth IRA contribution, and imagine if he did a Roth 401(k). Imagine those dollars growing tax free. I’d want to know more about what his income trajectory over the long term looks like.

Brian: If you were just doing this as a thought exercise on how you minimize income as much as possible for taxes, then boom. Yeah, it’s kind of cool that you made 66% of the money disappear from a taxability. What I like is because it just right here on the screen is that you’d be a millionaire in under 14 years. Imagine if you’re a tax-free millionaire. And the other thing is because you funded it with after tax money, you’re actually getting more of the money into that account that’s growing and compounding that won’t have the headwind of taxes in the future.

Bo: One of the beautiful things about financial planning is a lot of people focus on how can I save the most amount of taxes today. But if you have a really good financial plan, you’re not thinking about how can I save the most amount of taxes today. You’re thinking about how can I save the most amount of taxes over my entire lifetime. And that’s why at these lower income thresholds in the 12% bracket or even 22% bracket, we love building Roth assets.

Not Filing Taxes for 8 Years (12:21)

Video Clip: Now, we’re going to take a call from a client who hasn’t filed tax returns for many years. Most people once they don’t file for a lot of years, usually they’re too scared to file. Also, they get in the process of if I didn’t file for that many years, why should I file now and I have to pay somebody to do it? So, let’s talk to him and see if he’s different than everybody else. Here’s your advice. One thing led to another. So, I have not filed taxes in the last 8 years, which is not good. Why haven’t you filed? I couldn’t afford to file. When you don’t file, the IRS can charge you criminally, but if you don’t pay, then there’s so much they can do, but it’s usually worse if you don’t file than if you file and not pay. And how old are you? 52. Okay. Married? Yes. And children? Who files with the children? My wife. File separately. I think it was a good idea for your wife to file separately. This way, she’s not responsible for your tax debt. Do you own any real estate? I have a mortgage on my main residence. The mortgage is for 150 right now. How much would you say the house is worth? 230,000. It’s easier to deal with it now because the more equity you have, the more the IRS will expect you to pay. I’ll send you some documents. You will contact the IRS and see what we need to file. And we’ll just file the bare minimum. Sometimes they only require us to file a few years, usually the last six years. And if we owe money, then we’ll figure out how we’re going to pay for it. We set up a payment plan to see if you qualify for any of the tax relief programs.

Brian: There are programs where the government will let you get on an installment plan with them. Now, I will tell you that that kind of puts you on the naughty list with the IRS. So, you kind of really need to be careful before you go that route. It’s better to do it now than to let this just continue to build up in the background and create a huge tax bomb for the future.

Bo: Yeah. I always wonder where the mindset is. Someone, you know, I don’t file this year and like, okay, well, I didn’t file last year and I kind of got away with it. So then I don’t file the next year and the next year and the next year. If you are someone with income and assets and you have things that the government could come take away like your assets, like your income, I don’t think operating under the assumption, oh well, they’re just not going to catch this, I’ll just fly under the radar. I don’t think that that’s what likely happens. And when you do get that letter, whether it be a year, 3 years, 5 years, 8 years from now, they literally have the authority to come take your stuff, to come garnish your wages, to come repossess your assets. You do not want to be on that side of the federal government.

Brian: Pay your taxes. If you get nothing else out of this video, pay your taxes. We’ve covered it earlier in the show that tax evasion is illegal. And that’s when you don’t file your taxes, when you purposely exclude stuff, that’s tax evasion. That’s going to get you put in the clink. But if you are smart and you actually keep up with what’s going on with the financial world, the tax policies, you can actually use tax avoidance, completely legal, and maximizing your wealth journey. And that’s why we love covering this type of content. Who would have thought coming in here talking about death and taxes could have been this much fun? I’m your host Brian joined by Mr. Bo. Money Guy Team, out.

Free Resources

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

Articles

The Best Tools for Filing Your Taxes in 2026

Have you filed your taxes yet? You still have ample time left until the April 15th deadline, but it’s probably best not to procrastinate too...

Articles

6 Financial Changes To Make in 2026

There is no need to wait until an arbitrary date on a calendar to make positive changes in your financial life, but if you are...

Articles

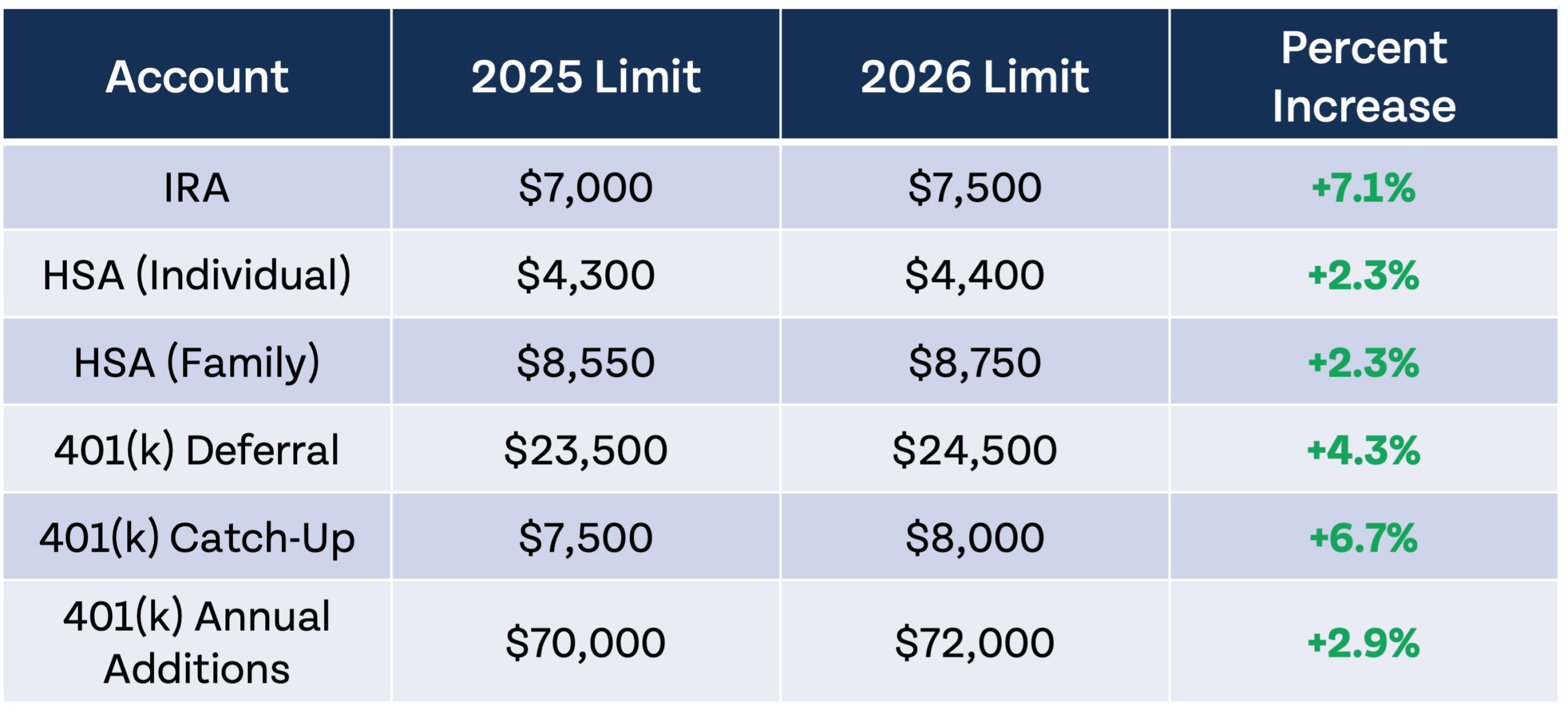

The IRS Just Announced 2026 Tax Changes!

Each year, the IRS adjusts retirement account contribution limits, standard deductions, marginal tax rate brackets, and more for inflation. I’m happy to announce that it...

Financial FAQs

Courses & Tools

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Recent Episodes

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

Financial Advisors Correct the Internet (Part 2)

Is viral financial advice doing more harm than good? In this react episode, we correct the internet once again and separate the news from the...

Episodes

These Money Moves Feel Like Financial Cheat Codes

Want to build wealth faster without taking unnecessary risks? We break down seven financial "cheat codes" that can dramatically improve your long-term finances and help...

Episodes

Do You Really Have To Budget Forever?

Do you need to budget forever? Brian explains when to graduate to cash flow management & focus on what can help you move the needle...