-

▼

-

▼

Markets crashing isn’t new, but how you react is everything. We break down the five biggest market crashes in U.S. history, from the 1929 Wall Street collapse to the COVID crash of 2020. Discover the common mistakes that devastated investors, the key takeaways to protect your portfolio, and why a well-built financial plan stands strong through any market storm. Learn how to control what you can, avoid hype-driven investing, and build long-term wealth no matter what headlines say.

Enjoy the Show?

Where You Can Watch and Listen:

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

- Episodes of The Money Guy Show every Friday

- Episodes of Making a Millionaire every other Monday

- Mini-shows every Wednesday

- Ask Money Guy Livestreams every Tuesday

- Tons of other fun content!

Introduction: Markets Crash, But What You Do Next Matters (0:00)

Brian: Markets crash. That’s not new. What you do next, that’s everything.

Bo: And Brian, I am so excited about this because there’s a song and dance that the media does time and time again when the markets crash, telling you that the market will never recover and that you should sell everything. And we want to cut through that noise today because we believe there’s a better way to do money.

Brian: Today, we’re going to look at the five worst market crashes in US history: the cause, the effect, and what you can learn from each so that your financial plan succeeds before, during, and even after volatility. Let’s jump right in.

Crash #1: The Great Wall Street Crash of 1929 (0:40)

Bo: All right, Brian, let’s talk about the very first one. Now, this is the one that I think everyone has heard about. This is the Great Wall Street crash of 1929.

Brian: This is the one that actually led to the Great Depression. I think even if you’re not as familiar with the Wall Street crash, you’re very familiar with the Great Depression, all the bread lines and everything else. So, Bo, let’s give them the timeline and even kind of set the context of what was going on back then.

Bo: Yeah. So, this actual crash took place from 1929 to 1932. And as you can imagine, the headlines were pretty aggressive. Wall Street in panic as stocks crash. I mean, this was a terrifying time in our country, something that we had not seen up until this point.

Brian: Well, this is also what broke the banking system. You think about all the runs on the banks. If you watch It’s a Wonderful Life, you see what was kind of a flash of what was going on. And there’s a few key factors that we can kind of focus on and I think as since we’re doing five of these, I want everybody to have the context of think about greed and then think about the exasperation that comes from then the fear that this creates. The human dynamic is amazing and you’re going to see a trend through all these. And here’s the key factor on this one: excessive speculation. There’s some of that greed showing up and margin trading. Did you even know that they had margin trading back then?

Bo: People did not even know that that was a thing in the ’20s. What happened is people saw run-ups and they started pouring money into the stock market. They started selling their bonds, their fixed income, their conservative assets, and then they even started mortgaging their houses to get more money in. So, this is literally just like you said, Brian, this is like greed at an epitome. People wanting more, more, more, more, more and then I mean I couldn’t believe when I read the stat that 1929 there were 300 million shares of stock that were on margins.

Brian: Unbelievable. This is the wild part. And then the lack of regulation and market exuberance that obviously led to a disconnect from what the companies were worth that were on these exchanges to what the value that they were trading at. It just got disconnected completely. And then the federal government tried to curtail this. They tried to raise interest rates, but this was on top of a mild recession that had happened earlier that summer. So, it was this perfect mix of events. And so, when we think about this, when we think about this as an investor, what did the actual numbers look like? What was the gravity of this?

Bo: If you think back to this time period, it was actually an 89% drop in the Dow Jones Industrial Average. I mean, that is devastating. That makes my stomach hurt just looking at it. And then if you think about this, this is why this sparked the Great Depression. This is what I mean when you just see the stats of the GDP fell 30%. Unemployment peaked at 25%. This is if you’re getting I mean think about that from a standpoint of your social group, your friends, your family, you know, people that have been devastated by the impact of this speculation and then the aftermath of all these people losing their jobs is really kind of a scary thing. And then that led to little to no liquidity available in the markets. You hear about the bank runs that caused over 9,000 banks to fail. And this was such a severe downturn. This was so gravitous that the market actually didn’t get back to its pre-crash levels until 1954. That’s how severe and how big and how bad and how aggressive this downturn was.

Key Takeaway: Trees Don’t Grow to Heaven (4:25)

Brian: And so the question may be, okay, well, what do we take away from this? What do we learn? How can we think about that market crash and apply it to present day? And I think the takeaway is something that we can all constantly be reminded of. Trees don’t grow to heaven. Now, people are say, “What? What do you mean by that?” I just want you to know I am old enough that I’ve lived through so many crazes that people just lose their mind about. Historically, you hear people talk about tulips. I’ll talk about Beanie Babies. You can think about anything where people are chasing the latest greatest trends to their detriment. I mean, this is the human component. Back to the greed is that there’s just never enough that people just to satiate the appetite that they want more, more and they take all these crazy risks and then when the human element, the herd element where everybody panics and gets into fear together, you see this is why Bo, don’t go chasing the hot dot. Make sure you’re not sticking all of your financial success to one key thing being successful and you’ll be in a much better place.

Bo: Yeah. In 1929 people were margining up to 90%. It’s like nine times your invested amount. That is so aggressive and so far out on the risk spectrum that if there were a 10% correction in the market, it would absolutely devastate you. It would completely wipe out your portfolio. Now, this is what we’re not saying. We’re not saying that the markets are scary and you need to avoid them and stay away from them altogether because market crashes are normal and they’re a part of being an investor. But while they are normal and healthy, what causes them to be devastating is when your behavior becomes abnormal and unhealthy. So you should be making the same decisions during a market crash as you do during the bull market. And in 1929, that was not what people were doing.

Brian: Yeah. It’s the common sense of the things we share on the show all the time. Don’t go out there and leverage up to go invest and do all kind of other crazy speculative risky things. Know your why with your money and what you expect out of it. And you can actually use it as a really powerful engine to create the wealth and the life that you’re dreaming for.

Crash #2: Black Monday – October 1987 (6:35)

Bo: All right, Brian. So, we’re talking about the five most significant downturns in stock market history. The second one actually occurred in October of 1987, and this is known as Black Monday. Oh, wow. And this is one I mean, when you see the headline, look at this headline here is that stocks plunge 508 points, a drop of 22.6%, 604 million volume, nearly doubles the record.

Brian: And here’s the thing that shocked me Bo when I first read this I was like it talked about systems broke and we live in a world now where algorithms and other things but the systems that you think about you can put in limit orders you can think about all the option systems. This really was one of those key factors where the programmatic trading and the portfolio insurance which caused all kind of other strange ripple effects caused this huge drop.

Bo: Yeah. So it’s fairly complicated what actually happened, but basically there were complicated financial products that were involved and these programmatic trading triggered it to where it just became this pylon effect that bad went from worse and worse went from worse to even worse and it fell precipitously so much that was the most significant single day drop in US history. And this was amongst the fact that valuations were super high and there were some global geopolitical things going on that had the public naturally a little bit more anxious and uncertain. So when the fear crept in, everyone ran for the exits rapidly.

Brian: So let’s look at what this looks like visually. And here’s the crazy thing. Now we see the drop of 26%. But I just saw in that headline close between 22 and 23% of this came in one day. Single day. And what’s crazy is when I look at the graph when we were doing the show meeting and I was like, “Wait a minute, that doesn’t look as steep as I would think.” And it was brought… This is a Monday. That’s right. So when you look at this chart, realize you had a close on Friday and because we use Y Charts, it basically tried to level out between what happened Saturday, Sunday, but this is actually a one day drop. So it is so much steeper than even what the visual shows. That is a gut check if I’ve ever seen it. Can you imagine? You have a million dollar portfolio and you come out the other side and within a weekend you’ve lost $280,000, you’re devastated.

Bo: And so the aftermath of this was pretty significant. Also, markets returned to their pre-crash levels by May of 1989. But it’s interesting, even though this was such a significant bad day and this actual downturn right here around Black Monday was so severe, a recession actually did not follow this. Everybody thinks, oh, these giant bear markets, these giant crashes, it moves the economy into depression. That was actually not what took place in 1987. There was no recession there.

Key Takeaway: One Bad Day Won’t Derail You (9:29)

Bo: So, what’s the takeaway? What’s the thing that you ought to know or the thing you ought to recognize? One singular bad day or one singular bad event won’t necessarily derail your wealth building journey even though it does feel painful in the market.

Brian: Yeah. I mean even on that previous graph it showed and we’re going to talk a little bit more about this V-shaped recoveries is a common thread you’ll hear but it is important for anybody who starts investing. There’s a reason we tell you this is long-term money. Money that you can let sit out there for 5 to 7 years is because even in normal markets, these are we’re doing the five biggest drops. But you think about the intra-year changes that we see and I don’t know if anybody’s ever shared this with you but if you look at it we have a graph up on the screen and for my podcast listeners it is very common that every year including the good years you’re going to see intra-year changes or drops of around 14%. People don’t know that. They just assume that when we talk about an annual rate of return of 8%, 9% it’s going to come in those nice little pre-fabricated cubes. No, there’s going to be a lot of gut-wrenching emotions that you better be prepared. It’s just a feature of this wealth building process, but don’t get caught up in the emotional side of this.

Bo: I think people don’t recognize that when you hear years like 2003 where the market made almost 30%, they don’t recognize that inside of that year the market was down 14% or in 2009 and the market makes almost 25%. Inside of that year, the market was down 28%. Volatility and downturns and the market moving up and down is normal. That’s why you want to make sure that you don’t make rapid decisions when things get uncomfortable because the worst thing that you can do is try to get out at the bottom when it’s going to turn very quickly.

Crash #3: The Dot-Com Bubble Burst (2000-2002) (11:23)

Bo: And I think these next couple recessions, these next couple severe bear markets show us that because this is one, Brian, you remember all too well: the 2000 to 2002 dot-com bubble burst.

Brian: This is what’s amazing to me is that these last three that we go I actually was managing money through all three of these and the dot-com bubble just to kind of set the stage for everybody and once again everybody’s chasing the hot trend. If you look at what the headline was on this, the year dot-com turned into dot-bomb, and I did live through this, and this is where it didn’t matter if you were doing pet food, if you’re doing grocery stores, if you just put .com at the end, money was just being thrown out there after people because once again, the human factor is that we pile into things thinking that we’re going to get into the latest greatest trend. And it was devastating financially to a lot of folks.

Bo: And so what ended up causing this was exactly that, this massive speculation on unprofitable companies. So the opportunity looked so exciting, so amazing, so incredible that the fundamental numbers did not actually justify the valuations these companies were seeing. And what that ultimately led to was overvaluation, companies being listed for way more than they were worth, and herd behavior. You would go to the office Christmas party or to the family reunion and all of a sudden you hear somebody telling you about oh this latest greatest amazing high-flying stock they made all this money on and so naturally you decide okay I got to pile in, pile in, pile in, pile in, pile in. This FOMO driven investing, this idea that if I’m not in that I’m going to miss out led to the market being unbelievably frothy and even irrationally exuberant.

Brian: Well, I think it’s something and we’ll get to it but the key takeaway is, but this is something just for you to internalize and think about is that a lot of people when we have disruptive new technology, you have to realize that this disruptive technology is going to take a lot and turn it into a few key players. So to have those few key players that end up coming out top of the heap at the end, you’re going to see lots of destruction in the wake of that. So let’s actually look at the actual numbers. Yeah. From this drop from the dot-com bubble bursting. If you look at the S&P 500, it actually dropped 49%. It cut in half over this time period. Yeah. I mean, and this is widespread wealth destruction. We had you think about this, the recession of 2001 kicked in. You also this is the start of the last decade. Now, here’s I want to give you guys the context of somebody who was actually managing money through this is that I actually we did if you were a professionally managed portfolio with diversification that was goals-based and your risk profile, you actually did really good. This was a great time to be a financial adviser because I remember how in this period, diversification actually got a lot of people through this and actually come out even better.

Bo: Yeah. If you are someone and you’re going through this downturn and you’re going through this type of scary market, the things that have always been sound continue to be sound and actually continue to be even more sound. Things like diversifying your portfolio, not having everything in one basket. Things like dollar cost averaging. Yes, the market from the peak to the trough dropped 49%. But if you were buying every month or every quarter or putting your money to work every year, you are actually capitalizing on that decline. And if you have a long-term horizon, if you can zoom out and say, “Okay, yes, the market is down right now. My portfolio is down. I have some losses on paper, but my timeline is 10, 15, 20, 25, 30 years out into the future.” If you can have that perspective, those tools, those keys can allow you to be a successful investor even when these market environments present themselves.

Key Takeaway: Hype Is Not a Business Model (15:15)

Brian: So, what’s the big takeaway we have from the dot-com bubble bursting? Hype is not a business model. That’s exactly right. That’s like I said, a lot of destruction is going to be created and I think a lot of people feel like they have to go scramble in and try to pick the next big winners. But it is worth remembering that 90% of fund managers who are doing this getting paid professionally to go pick the next latest and greatest thing underperform just the index. And that’s over a 15-year time frame. So guys, I’m telling you, innovation is going to create lots of opportunities for you to make money off of, but there’s also going to be lots of destruction in its wake. So quit trying to pick the winners yourself and just buy the market itself. And I think you’ll be rewarded in the long term in a much better way.

Bo: Oftentimes it’s a more prudent investing strategy to just be the market than to try to beat the market. And the dot-com bubble sort of underlined that to be true.

Crash #4: The Great Recession (2007-2009) (16:12)

Bo: All right, Brian, let’s talk about the next great market crash that we’re seeing. This is the fourth one on our list. And this one is another one that you and I remember all too well. This is actually the Great Recession from 2007 to 2009.

Brian: Yeah, this one I always like because and I love the icon we used here because we have a house instead of an arrow going up and down. If you’re noticing this is how much intent and purpose we put in this stuff. And it’s because we did have a complete collapse. And you guys, you now have the context. You know the after effect. But for everybody who didn’t know, back then everybody’s saying God’s not creating more land. That’s right. So houses can’t go down in value. Man oh man, did we show that that is not the case. Once again trees don’t grow to heaven is that look at what happened back in 2008.

Bo: Yeah. We actually saw a number of key factors leading to this great recession. One of them subprime mortgages. Banks were lending money to people that did not need to be borrowing money and they were borrowing it in droves. We saw excessive leverage. Folks that didn’t need to be borrowing money anyways were borrowing more and more and more. And then financial institutions are recognizing, hey, we can package up all this borrowing, all this leverage, all these bad deals. And if we package enough of them together, we can sell them as something that they are not. And this beautiful storm of horrible decision-making conglomerated together to create the largest downturn, the most significant drop that we’ve seen in the financial markets and the economy since the Great Depression.

Brian: Well, I mean there’s so much once again the hubris of the human condition is that we have this overconfidence. We take something that’s good and then we just the greed of the situation is I mean I lived through this and I remember I even used one of these loans a stated income loan. Can you imagine if your underwriting process where housing is such a hard thing just asking somebody hey on your word what do you think you have coming? Stated income, not going out there and looking at pay stubs or anything else. This thing that shows just the amount of speculation and greed that went into this. And once again, valuations got disconnected from where the value of actual assets were. And if you want to see what the drop is, look at this. We lost 49% over this two-year period. And what this doesn’t show, I mean the graph shows it, but you can see a lot of this came in that fourth quarter of 2008 where the poop really hit the fan where we realize this is where you saw Bear Stearns, Lehman Brothers, and all this other stuff where you realize all these people who were just heavy into these mortgage products got crushed.

Bo: Yeah. From October 1st of 2008 to November 21st, that 49% loss that we saw of the Great Recession, 36% of that happened in that small time frame. That’s how severe that fourth quarter was. And so the aftermath was pretty severe as well. Not only did we see a severe global recession, not just here in the United States, but we saw it across the entire globe. We saw bank failures, we saw government bailouts. It was unprecedented times. Again, the most severe economic downturn that we’ve seen since the Great Depression and again fueled by greed and bad financial decision-making.

Brian: Well, I mean, and we all remember the loss of jobs. Housing was just, you know, you saw neighborhoods that just had essentially PVC pipes on the land for a decade because this devastated. I even have seen people talk about the aftermath of this is the loss of trade because we just quit building homes and that’s why now we have inventory issues where there’s just I think this has contributed to the situation we’re in now where housing is hard is because it had such a financial impact that just the supply just got disrupted and we’re still paying the price for some of these decisions.

Key Takeaway: Don’t Stretch Yourself Too Thin (20:07)

Bo: And so, what’s the key takeaway? What things should you take away from this? Don’t ever stretch yourself too thin or don’t get too lean on cash. Don’t buy into the hype. Oh, well, they’re not making more land. You can’t lose money on real estate, so you need to buy as much as you can. You need to lever up as much as you can. You need to put as little down and borrow as much as possible. If you find yourself in a situation where people are trying to convince you to make financial decisions that don’t even pass the common sense test, your spidey sense should start going off that maybe this is not what I need to start doing.

Brian: Well, I mean also I think think about the Financial Order of Operations. There’s a reason cash has two steps is because we all take it for granted until we go underwater and get in an emergency situation like, “Oh my gosh, cash is so much more valuable because home equity lines, all these other things that are tied to housing, it might be a little bit more quicksand than it actually is stable or bedrock that we were presented.” And that’s why we’ve tried to help you. We not only have we given you the blow-by-blow of how not to fall into access to cash traps, but we have home buying calculators. We have a home buying checklist. Go to moneyguy.com/resources. Take advantage of these things because we’re trying to educate you so you don’t make those mistakes that history has already shown us the way for.

Bo: Yeah. I think if we don’t learn about our history, we are doomed to repeat it. It’s why we come up with the things that we do and the resources that we have and the tools that we make available to you. These are all things that we have pulled out of these downturns, these recessions, these negative market events so that you will not fall prey to them so you can keep yourself protected. But inevitably, even if you’re making all the right decisions and you’re doing all the things that you’re supposed to be doing, there’s a good chance that unknown unknowns are going to come your way. Things that you could not have imagined, you could not have planned for may come into your purview. And that’s exactly what happened with the fifth most significant downturn we’ve seen in the stock market history.

Crash #5: The COVID Crash (March 2020) (22:04)

Brian: This one actually took place in March of 2020. This was the COVID crash. Yeah. Now, look, I’m split in two different ways. I can’t believe this many years has passed since COVID, but I’m also, you know, we are now far enough from it that we can take some lessons and learn from what was going on. Like if you look at the headlines talking about nobody had this on their bingo card for the year is because it is the unknown. I mean nobody when a pandemic and then also the reaction because once again we’re herd creatures. So you can see we had the worst route. The headline on this was the worst rout for Wall Street since 1987 which we already know how crazy that is. So here’s Bo over what are the key factors that actually led to this.

Bo: Well, obviously the first thing is there was a global pandemic at play. There was an unknown where everyone was scared about health risks that were very real concerns across the global public. And because of that, we saw economic shutdown. A lot of industries, people weren’t allowed to leave their house. Industry was not allowed to operate. And we saw supply chain disruptions. We just took for granted the fact that, hey, the thing that I need to be here tomorrow is going to show up tomorrow. Well, if the entire supply chain shuts down, there are massive global economic impacts of that. And that’s exactly what we saw during the COVID crash. And what the numbers actually would suggest is that in just over one month, we saw a 34% decline in the market. This was the fastest bear market we have ever encountered in the US stock market.

Brian: Yeah. I mean, I think if you were reactionary, you probably got yourself in a heck of a situation because it was one of those things where there was a lot of the aftermath was massive stimulus. You know, I think about how we were paying people to basically be home. We were paying businesses so they could do payroll. We now it got us through it, but we’re still we don’t even know how we’re truly going to pay the price on this for all the debt and other things we’ve taken on, but it definitely created a lot of stimulus and that but it is because all this money was thrown at it. It was the shortest recovery in US history. And that’s why that V-shaped recovery is a legitimate thing. And that’s why sometimes the best thing you can do even in bad situations is do absolutely nothing because reacting is not the course of action. And that’s what key takeaways and this is what Bo we’re going to talk about what you can do before so that it’s good during before and even after the key takeaway is control the controllables.

Key Takeaway: Control the Controllables (24:46)

Bo: Yeah, there were certainly things in COVID that we did not have any control over. There was so many unknown unknowns, but there are things that we did know. And one of those things is, hey, I had a financial plan going into this pandemic. And if it’s a sound, well-thought-out financial plan, it should be good before craziness happens. It should be good while craziness is going on. And it should even be good after the craziness passes. It’s why we want to have things like emergency reserves of three to six months of living expenses. If I’m a retiree or someone living off of my portfolio, if I had 12, 18, 24 months of liquid living expenses readily available, I did not have to make any decisions in the midst in the middle of COVID that had long economic impacts for me. It’s why a sound plan is a sound plan because it prepares for those things. So control the things that you can control. And the better you do that, the more prepared you’ll be for the things that you cannot control.

Brian: I know we’re getting new people every month and a lot of you are like, “Okay, it sounds good, but what’s this actual plan that you guys paint by numbers?” I mean, we really literally have written the book so you don’t have to go reinvent the wheel. This is the instruction manual. Go take advantage of it. It’s completely free. Go to moneyguy.com/resources. This is going to protect you because you’re not going to run into how often in here Bo did we hear people running into they ran up too much debt or people just were so excited about how good their housing was done that they bought bigger houses and they cut it so close they didn’t have emergency reserves and you even built a system that’s going to maximize the tax benefits but then even get to the why so you live your great big beautiful tomorrow. We’ve written the instruction manual for you guys. You just have to kind of do it and don’t just take our word because we also want to show you because there’s been a common theme is I think anybody who’s lived through these and I couldn’t believe that I’ve actually lived through four of these five things and I’ve managed money through three of these five things and there’s a consistency that literally consistent behavior and not losing your mind and letting the emotions overcome this. And that’s why we have a great kind of close out to this.

When in Doubt, Zoom Out (27:04)

Brian: When in doubt, zoom out. And Bo, kind of you can look at this. I mean, this graph is telling a huge story here.

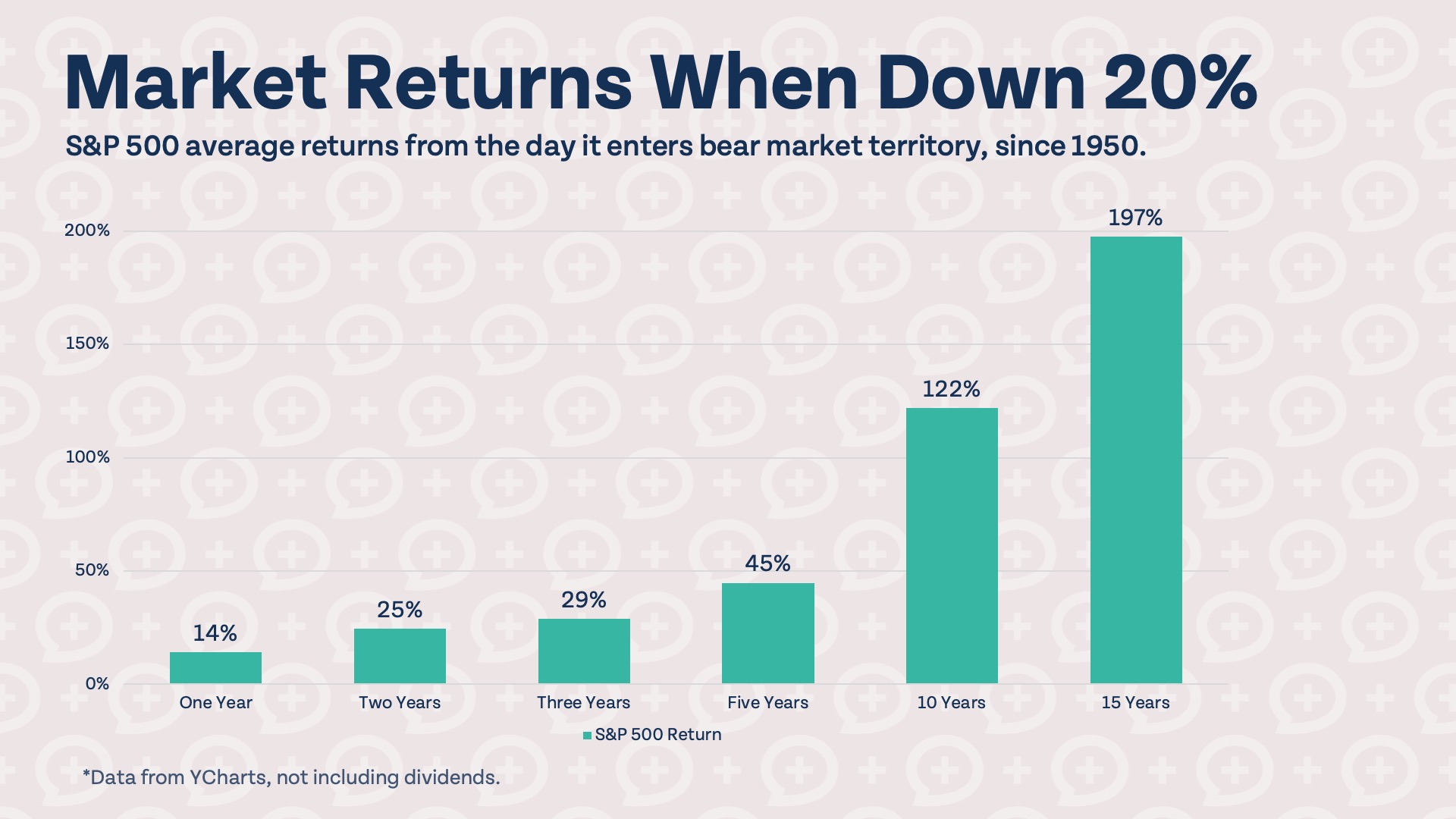

Bo: Yeah. Even though we just went through the five most significant downturns in stock market history, you may be thinking, guys, well, the stock market, it sounds scary and uncertain and volatile and uncomfortable and maybe I should have just avoided altogether. Well, even with those downturns, even with those significant events that have taken place in our US economic environment, if you were to zoom out and just look at what the stock market has returned from 1930 all the way until present day, it’s like 17,000%. So, at any point in time, if you were an investor, if you were well diversified during the last decade, you were still an investor that made money. If you were someone who was investing in the ’70s, ’80s, and ’90s, you were someone who was making money in the 2000s and 2010s, you were someone who was making money. If you can zoom out and have a long-term perspective, it’s not a matter of if a downturn is going to happen or if we’re going to have a bear market. It’s just a matter of when it happens and are you going to be prepared and recognize that this too shall pass. The market is up far more often than it is down. And the ups are far greater than the downturns if you have a long-term perspective.

Brian: Also, I think if you look at this graph and we think about like the Great Recession or the Wall Street crash, that was an 80 plus percent drop and I can’t even you can’t even see that. So, because in perspective of history, it’s so small. Even fast forward to the Black Monday, barely see it on this graph. Even 2000, the dot-com and the 2008 Great Recession, it looks so small. So, a lot of you might be looking at this going, “Guys, does that mean the greatest days are behind us because this thing has had a huge run-up?” I talk about this all the time, the law of accelerating returns and the fact of innovation of the ’80s with the personal computer and then what happened in the ’90s and early 2000s with even the internet and the proliferation and now we’re in this new AI phase. When you hear me talk about the law of accelerating returns, guys, this stuff is speeding up. So, that’s why you still have the opportunity. The big thing is just control your behavior. Control the controllables as we just talked about.

Navigating Complexity: When to Get Help (29:20)

Brian: And a lot of you are like, okay, beyond the Financial Order of Operations, what does this mean for me? Because I have been doing this. I’ve lived through a lot of this. But guys, I don’t know. I’ve now created something because I’ve lived through this. I have seven figures of success and now my simple life has become so much more complicated. How do I navigate this? This is your first time. And I get nervous for people when especially you’re the CEO of a multiple seven-figure enterprise. How do you navigate the complexity that comes just from this wild world we’re in? Once again, the abundance cycle comes in because we will leave the porch light on for you. I want you to come absorb as much of the free stuff we give you, but when your life gets complicated and you worry about, hey, this is so big now. I don’t want to make a mistake. Give us a chance. Go out there to moneyguy.com/become-a-client and check out our introduction message. Just so you can see what we look like when we put coats on, too. And, you know, and I think you’ll see that there is something to this abundant cycle that we’ve created since 2006.

Conclusion: Be Greedy When Others Are Fearful (30:25)

Bo: Investing does not have to be scary. Money is nothing more than a tool that allows us to achieve the goals that we have. And putting our dollars to work for us is the method that we use to achieve those goals. And the more educated and more well-prepared you can be for the unknown unknowns, the more likely you are to have a consistent plan that you stick to over the long term. And if you can do that, you really can have a great big beautiful tomorrow.

Brian: And we just talked about crashes. And you can’t help but think about crashes and use Uncle Warren: be fearful when others are greedy and greedy when others are fearful. That’s so much easier for me to read out to you than to actually live. And that’s what we’re going to help you become that financial mutant so you actually get excited when everybody else is freaking out and we’re going to continue to create this type of content. I’m your host Brian Preston, Mr. Bo Hansen, Money Guy team out.

Free Resources

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

Articles

Are Index Funds Still Better Than Active Funds in 2025?

Over longer periods of time, index funds tend to outperform actively managed funds in most categories. Recently, total assets in index funds have surpassed the...

Articles

What To Do When the Stock Market Is Down

The S&P 500 is down nearly 15% from its highs earlier this year, inching closer to bear market territory. While it may not be wise...

Articles

How To Prepare for a Bear Market in 2025

The Nasdaq stock market index is in correction territory, down over 10% from recent highs. The other major US indexes, the S&P 500 and Dow,...

Financial FAQs

Courses & Tools

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Recent Episodes

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

We Changed The 4% Rule!?

Retirement planning isn't as simple as following the classic 4% rule anymore. In this Live Q&A, we explain why the traditional retirement withdrawal strategy deserves...

Episodes

Is Aggressive Saving Derailing Their Short Term Goals?

High earners in their mid-twenties, cash poor, and a wedding 12 months away. In this episode of Making a Millionaire, we show Joey and Leah...

Episodes

Why This Money Advice Has EXPIRED

Traditional financial advice isn't always wrong, but some money rules simply haven't kept up with today's economy. In this episode, we reveal which classic money...