Change your life by

managing your money better.

Subscribe to our free weekly newsletter by entering your email address below.

Subscribe to our free weekly newsletter by entering your email address below.

Index funds are one of the best wealth-building tools available to everyday investors, but most personal finance content only tells half the story. Bo reveals four uncomfortable truths that people often leave out and the importance of discipline to stay the course.

You’ll learn why you may be less diversified than you think, why set-it-and-forget-it can quietly erode your after-tax returns through poor asset location, and why the index fund label alone doesn’t guarantee quality or low cost. This episode won’t change the fundamental case for index funds, but it will give you the tools so you can invest with confidence.

For more guidance on building a smarter investment strategy, explore the Ultimate Guide to Investing and free tools at moneyguy.com/resources.

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

Bo: People love index funds. It’s pretty common to see personal finance junkies online telling people to just buy index funds and hold them forever. And it’s no wonder they’re so popular. They’ve got low fees, built-in diversification, and they outperform most professional fund managers over time. But there are some details about index funds that people often leave out and some misconceptions that can cost you. Guys, I am so excited because today we’re going to reveal four uncomfortable truths about index funds that most people skip over so you can have the complete picture before you invest.

Bo: Before we get into the uncomfortable truths, let me be clear about why this buy-and-hold index funds advice became so popular in the first place. It’s because index funds really are one of the best tools available to everyday investors. The S&P 500, which is the index tracking the 500 largest publicly traded US companies, has had an average annual return of roughly 10% since it launched in 1957. That doesn’t factor in inflation, but it’s still an impressive track record. The US stock market has been one of the greatest wealth creation engines in human history, and index funds are a simple way to take advantage of it. Over the last 15 years, 90% of active managers of US large cap funds have underperformed the S&P 500. In other words, the majority of professional fund managers, people who do this full-time with research teams and proprietary data and decades of experience, still can’t consistently beat a simple index fund over the long term. When you layer in the higher fees those actively managed funds charge, the gap gets even wider. So clearly index funds are pretty great and we’re not here to dispute that. But when it comes to investing, it’s important to understand what you actually own because if you don’t, it could lead to mistakes.

Bo: So here’s the first thing most people get wrong about index funds. They assume that owning an S&P 500 index fund means they’re broadly diversified across 500 different companies. And technically, yes, you do own a slice of all 500. But the S&P 500 is what’s known as market cap weighted, which means the largest companies get the largest slice of every dollar you invest. The top 10 companies in the S&P 500, names like Apple, Microsoft, Nvidia, Amazon, and Alphabet, make up roughly 40% of the entire index. So, a good chunk of your money in an S&P 500 fund is actually concentrated in just 10 companies. And the bottom 250 companies in that index represent a small fraction of your total exposure.

Bo: And that’s the first uncomfortable truth about index funds. You might be less diversified than you think. And that’s not necessarily bad. Those top companies are large, well-established, highly profitable businesses, but it does mean that if the mega cap sector has a few rough years, your diversified index fund is going to feel it pretty hard. On top of that, the S&P 500 is entirely US-based. So if you’re holding a domestic large cap index fund, you have zero exposure to international markets, small cap companies, emerging markets, or other asset classes like bonds or real estate. So the takeaway here is to know what you actually own. An S&P 500 index fund is fine, but adding exposure to international funds, small cap funds, or a total market fund can give you more diversification.

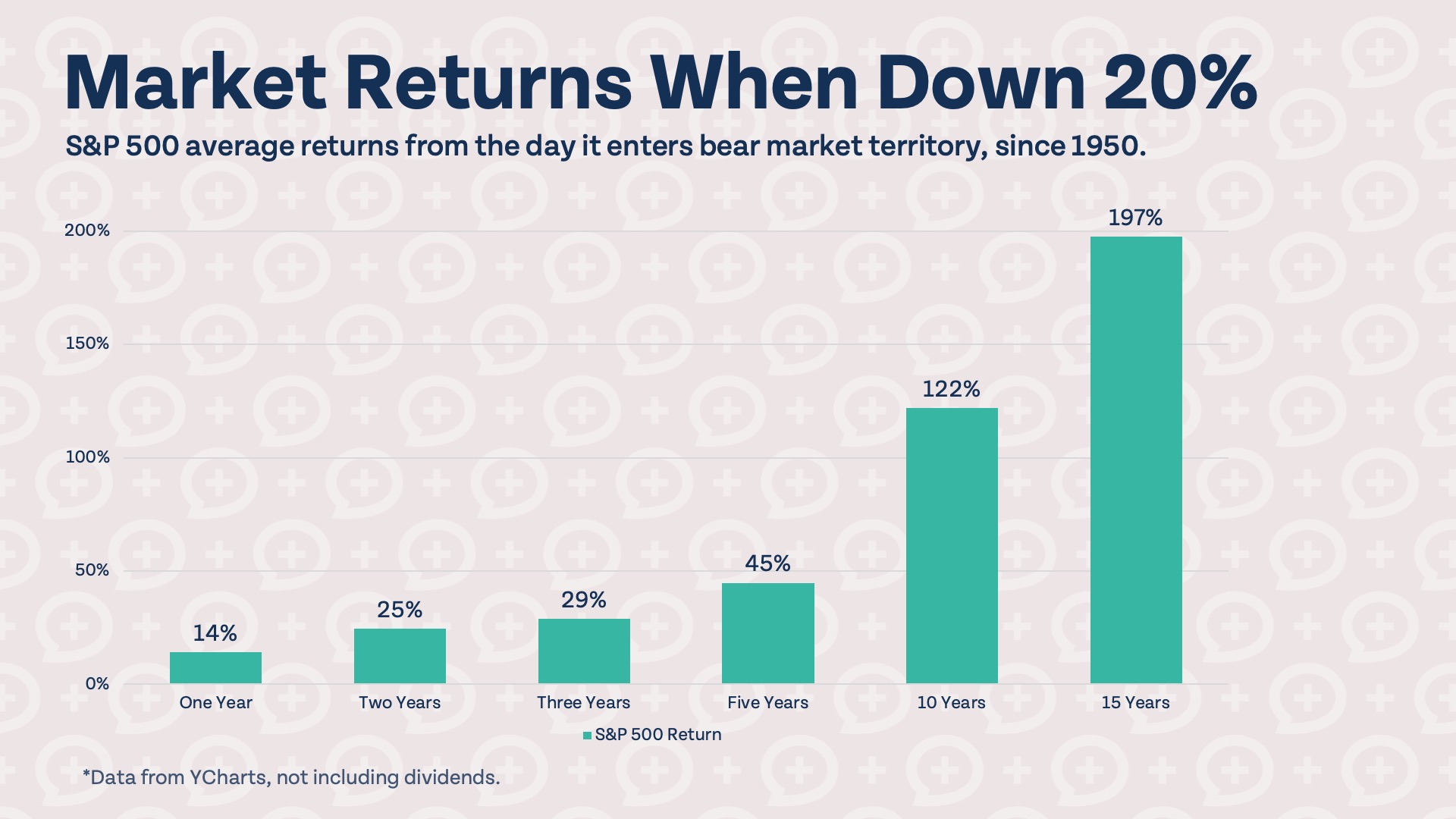

Bo: The next uncomfortable truth is the most important one of the list, and it’s one that can cost investors the most money. You see, index funds technically have excellent long-term returns, but here’s the thing. Those returns only apply to investors that actually stay invested. The S&P 500 has experienced multiple downturns of 30%, 40%, even 50% or more during major market crashes like the Great Recession of 2008, the dot-com bubble bursting, or even the pandemic downturn of March of 2020. In every single one of these periods, there were some investors who looked at their account balance, panicked, and sold, which means they locked in their losses and likely missed a significant portion of the recovery. And that’s the second uncomfortable truth about index funds. They don’t protect you from yourself.

Bo: In 2024, Morningstar published a report stating that over the previous 10 years, the average fund investor earned 1.1 percentage points less per year than the funds they invested in. And that means investors missed out on about 15% of the fund’s total returns, largely because of those poorly timed purchases and sales. Your investment strategy is only as good as your ability to stick to it when things get scary. This is one of the reasons many people choose to work with a fiduciary financial adviser like the ones we have here at Abound Wealth. Not just for the planning, but also for the coaching. There’s tremendous value in having someone in your corner who can steer you away from making emotionally driven decisions at the worst possible moment.

Bo: The next uncomfortable truth about index funds: they’re not entirely set it and forget it. One of the great selling points of index funds is that they are simple. You put your money in, you don’t touch it, you just let it grow. And that’s not a bad approach. Generally speaking, the less you tinker, the better. But if you set it and you truly forget about it, you could miss out on some gains. For example, an index fund in a taxable brokerage account has different tax implications than the same fund inside of a Roth IRA or a traditional 401(k). And you want to pay attention to that. Holding the wrong assets in the wrong accounts is what we call poor asset location. And it can reduce your after-tax returns over time, even without you realizing it.

Bo: Plus, index funds have no awareness of your estate plan, your insurance coverage, your debt, or your specific life goals. And yet, a lot of people mentally check the box on their finances once they have an index fund set up, and they stop paying attention to the bigger financial picture around it. The takeaway for this one: index funds simplify investing, but investing is just one piece of your financial life. You need to think about which accounts you’re holding them in, how they interact with your tax situation, and how they fit into your overall financial plan.

Bo: The next uncomfortable truth: not all index funds are created equal. When people hear index fund, they often assume they’re all basically the same thing, but they’re not. Index funds vary in three very important ways: what index they track, how well they track it, and most importantly, what they charge you to do so. The expense ratio is the annual fee a fund charges expressed as a percentage of your assets. It gets deducted from your returns automatically without you ever writing a check, which makes it easy to ignore. But over decades, the difference between a 0.015% expense ratio and a 1% expense ratio is enormous.

Bo: There are also index funds that track narrow or exotic slices of the market, a single sector, a specific country, or a leveraged version of some index. Those can carry higher costs and higher risks while still marketing themselves as index funds. The label alone doesn’t guarantee quality or low cost. The takeaway here: stick to broad market, low-cost index funds from reputable, established providers like Vanguard, Fidelity, or Charles Schwab. Look for expense ratios under 0.1% for broad market funds and read what the fund actually tracks before you buy it.

Bo: None of these uncomfortable truths we just walked through change the fundamental case for index funds. For most people, low-cost broad market funds remain one of the best and most accessible ways to build long-term wealth. And if you’re looking for a great starting point, we actually love target date retirement index funds because they handle the rebalancing for you. You just pick the fund closest to your expected retirement year and it automatically adjusts the asset allocation over time, gradually becoming more and more conservative as you get closer to that date. So you always have a blend of stocks and bonds appropriate to your timeline.

Bo: But here’s the deal. None of this really matters that much if your savings rate is too low. Your savings rate is much more important than your rate of return, especially in the early stages of wealth building. So, the question is, are you saving and investing enough? If you want to know if you’re on track, check out this video right here to see exactly how much you should save based on your age and your target retirement date. And as always, keep building towards your great big beautiful tomorrow.

Free Resources

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

Over longer periods of time, index funds tend to outperform actively managed funds in most categories. Recently, total assets in index funds have surpassed the...

Articles

The S&P 500 is down nearly 15% from its highs earlier this year, inching closer to bear market territory. While it may not be wise...

Articles

The Nasdaq stock market index is in correction territory, down over 10% from recent highs. The other major US indexes, the S&P 500 and Dow,...

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

Making late mortgage payments or raiding your 401(k)? Without a consistent plan, these behaviors can slowly snowball into financial disasters. Brian reveals 4 financial warning...

Episodes

We know Friday is coming up - but is the SpaceX IPO actually worth your money? We break down the risks, the frothy valuation, and...

Episodes

Twins on the way, a surprise 72-month car loan, and a short emergency fund - another story from the messy middle! See how we help...

Subscribe to our free weekly newsletter by entering your email address below.