Change your life by

managing your money better.

Subscribe to our free weekly newsletter by entering your email address below.

Subscribe to our free weekly newsletter by entering your email address below.

Brian and Bo reveal 10 surprising money stats for 2025 that every financial mutant needs to know. Learn why most Americans still can’t cover a $1,000 emergency, how Buy Now, Pay Later has quietly become a $4,000 debt trap, why first-time homebuyers are older than ever, and the magic behind $250K being “halfway” to $1M. Along the way, you’ll get practical takeaways (from car-buying rules to investment strategies) to help you make smarter money moves today and build your great big beautiful tomorrow.

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

Bo: We’ve got some brand new money stats for 2025 that we think will absolutely shock you. And Brian, I am so excited about this because the world of personal finance isn’t always super juicy, but sometimes we hear a stat that absolutely blows our minds. And those stats are what we’re going to share with you guys today. So, love them, hate them, these 10 stats will absolutely shock you. And some towards the end are downright mind-blowing.

Bo: So, Brian, this first stat is an oldie but a baddie. It’s one that just drives us nuts. We know that right now, according to Bank Rate, 59% of Americans could not come up with $1,000 for emergency.

Brian: Yeah. I think it’s important for all of our financial mutants to know, and remember, this is why we bring it up every year. Your emergency reserves is your protection or your barrier from what life throws at you so you don’t have to make desperate decisions. So make sure you plan accordingly.

Bo: So how do I do this? What do I do? I have to figure out how to make temporary sacrifices. How can I live on just a little bit less than I make today so that I can have a cushion in place so that my financial life does not get derailed? Because far too often we see people that live way too lean and then one of those unknown unknowns happens and they just start swiping. They just start racking up the credit card debt.

Brian: And then also don’t sleep on the fact that your financial order of operations is great in making sure you know exactly how much to have to start that emergency funds with step one highest deductible covered. So if you want to have a free copy of your own financial order of operations, go to moneyguy.com/resources.

Bo: All right, mindblowing stat number nine. And this one is not an oldie, but this is a frustrating one because it has come on the scene rapidly. The average user of buy now pay later has borrowed almost $4,000. And here’s a Captain Obvious statement. Majority of these people, nearly half of them have reported at least one financial problem. There is 24% said, “Hey, because we use this buy now pay later, we have regrets about overspending.” How about the 16% that missed the payment or how about the 15% once again being pushed by consumption in our society regretted the entire purchase.

Bo: And what is buy now pay later? It’s this idea of okay, I don’t need to actually spend money on this thing today. I can just make four easy payments of $19.99 or five easy payments of… And what’s absolutely wild is that 49% of consumers, one out of two people in America will use buy now pay later in 2025. And 20% said that they’re doing this every single month.

Brian: So, I think let’s talk about some key takeaways. Convenient debt, because that’s what this is. This is purchases of convenience, and they’re making it that much easier. Convenient debt is still bad debt. And people say, “Oh, Brian, there’s no interest rate.” If you’re someone who’s doing buy now, pay later so that you can pay a small amount now and not have to pay a full amount, there’s a good chance that you can’t afford that thing you’re buying. And frankly, if you can’t afford it, don’t buy it.

Bo: All right, speaking of bad habits, let’s talk about number eight. 27% of trade-ins for new cars have negative equity. That means that when I go to trade in my car, I actually owe more on the car than it is worth, and I am rolling that into my next purchase.

Brian: Well, I mean, look at this. Close to 8% of people owed more than $15,000. If we tried to figure out what the actual average was of negative equity in the second quarter of 2025, according to Edmunds, it was right under $7,000. That means that when you go to purchase a new car, you are paying because of negative equity, you’re taking out a loan that is $7,000 higher than the cost of the automobile.

Bo: So, what’s causing this? Why is this happening? Well, one, and we see this all the time, it’s low down payments. We know that cars are depreciable assets. As soon as you drive them off the lot, they go down in value. How about the fact that longer loan terms? If you think about the fact that the typical loan is now 68 months, that is almost double what we talk about when we say 20/3/8. And then what about high interest rates? We know that right now for a used car, the average interest rate is 11.9% almost 12%. Even for new cars, which are highly subsidized, the interest rate is a little over 6.5%.

Bo: And a way that you can make sure that the car falls into the reliable realm is if you can follow 20/3/8 with your purchase. You’re going to decrease the likelihood of being underwater. And if you’ve never heard of this before, 20/3/8 is simply a rule that says when you go buy a car, whether it’s new or used, we want you to put 20% down. We don’t want you to finance it for any more than 3 years or 36 months. And that car payment cannot exceed all of your car payments cannot exceed 8% of your monthly gross income.

Brian: And this is one of those things, guys, it is so much better to actually be rich than to look rich. So, don’t drive around in your wealth because all these decisions where people are financing and driving cars well beyond what their paycheck would recommend or suggest for them are failing to miss out on their Roth IRAs, all the things that their future self will regret because they were trying to fake it until they made it.

Bo: All right, we talked about cars, which is a huge purchase. Let’s talk about the next biggest purchase that most people will make in their lifetime. And this one really was a mind-blowing stat. Would you believe that right now the median first-time home buyer is 38 years old, almost 40 years old before they’re buying their first home?

Brian: Well, let’s actually pull up the stats on this, it’s even scarier than this. As you can see, if we’ve just gone back a decade previous, that stat was 31. But that’s not even the full picture because look at repeat buyers, that number has gone from 53 to 61 just since 2015. But here’s the thing that kind of blew my mind is if you look at all buyers when they group them all together, we went from 44 all the way to 56.

Bo: And so one of the questions, okay, why is this happening? It’s because home affordability is at an all-time low. We know that if you look just a few years ago in March of 2019, if you had a household income of $75,000, roughly half of the housing marketplace was affordable to you. You fast forward to now, March of 2025, only 20% of available houses are affordable.

Bo: So if you are in the market to buy a home and you do want to do it the right way, we want you to follow our 25/3/25 rule. And what that suggests is that when it comes to your down payment, you don’t have to put down 20%, you can put down a down payment as low as 3%. We don’t require 20% for first-time home purchasers. We also want to make sure that you plan on being in that home for at least 5 years. And we want you to make sure that the total cost of your housing is less than 25% of your gross income.

Bo: This leads to number six. Income only explains 30% of net worth. No, no, Brian, that’s got to be wrong.

Brian: I think there’s a lot of people, look, without a doubt, making a bigger income can turn into a better opportunity for building. But unfortunately, because of I don’t know if it’s lifestyle creep or it’s just lack of discipline. There’s a lot of people out there that are spending every dollar that comes into their household. So that’s why you cannot directly say income is resulting in higher net worth for the majority of people.

Bo: We always say all the time in the show, it doesn’t matter how much you make, it matters how much you keep. Just because you have a high income, just because you have an ability to spend a lot of money does not mean that you’re going to have the discipline necessary to be able to use that money to create margin to ultimately create wealth.

Brian: So, let’s give us the takeaways, guys. I want to make sure that anyone can build wealth. It’s really leaning into that first ingredient on the three ingredients of wealth building discipline. Can you live on less than you make and actually put that money to work?

Bo: And that leads to our number five mind-blowing stat. 61% of 401k plans now have automatic enrollment where if you don’t want to participate, if you don’t want to be part, you actually have to opt out as opposed to opt in. And the results of this small little change have been mind-blowing.

Brian: Yeah, this one warms my heart a little bit. Automatic for the people. Look at what has happened since 2006. Automatic for the people has caused people now we got 61% auto-enrollment. More people are going into retirement plans and their future selves will thank them for it.

Bo: Think about this. Plans that had automatic enrollment had a 94% participation rate compared to 64% without that. That means that because of this automatic enrollment, people are participating. And of those, 69% of folks who do automatic enrollment have it built in where every year it gets 1% better.

Bo: So make sure you invest that money because the next stat that’s going to break your heart is when you find out 28% of IRA rollovers remaining cash after seven years.

Bo: So Andy Reid, he’s the head of investor research behavior at Vanguard. He literally called this, he said, “IRA cash, cash sitting in IRA is a billion dollar blind spot. Folks putting their money into IRAs via rollovers or contributions and not doing anything with it.” And so you may be asking the question, okay, how’s this happen? 68% of folks said they didn’t realize it was in cash. 48% said, “Hey, I thought as soon as I rolled it over, Vanguard was just going to take care of it.” And then 15% of folks said, “You know what? I knew I was supposed to do it. I just never got around to it.”

Bo: So, let’s fix this today. If you go look at the key takeaways from this is know what your dollars are invested or first listen to the show, hit pause right now and then go pull up your accounts and say, “Oh, okay. Good. I’m invested.” Make sure this money is truly invested so you’re not part of this horrible statistic.

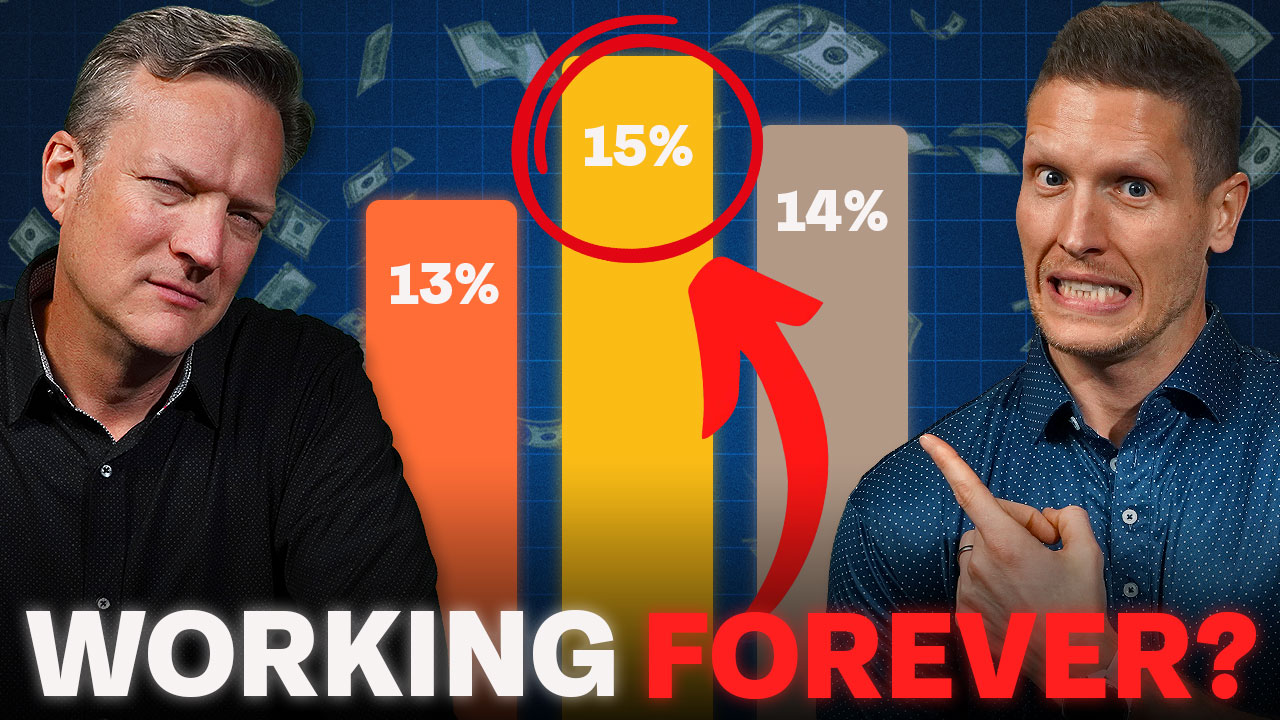

Brian: And the solace that you can have is if you put your money to work, if you actually begin participating in the equity markets, do you realize markets are up eight out of 10 years? People think that the stock market, oh, it’s like gambling. It’s red or black. It’s win or loss. That’s not true. If you look at any given decade over a 10-year period, the markets are usually up for eight of those years and down or have a bear market in two of those years.

Brian: Well, I think a lot of people because the nightly news covers all the ups and downs throughout the year. There’s a lot of intra-year declines. Meaning that even in really good years, the market might be down as much as 49%. We’ve seen that in certain years, but if you just average it out, there’s likely a 14% intra-year decline that even good years have. It’s just you need to zone out of that noise and just know markets make money eight out of 10 years.

Bo: And that leads to mind-blowing stat number two. Would you believe it if we told you that $250,000 is halfway to 1 million?

Brian: Now, wait a minute, Bo. Something doesn’t compute here. The math ain’t mathing. It’s because 250 out of a million is 25% and you’re saying that’s half. Half is 50%. How can 25% be 50%?

Bo: So, let’s show you this. Let’s assume that you’re going to save $833 a month. You’re going to save $10,000 every single year. And let’s assume that you can make 8% rate of return on those dollars. Well, after I have been investing for 13.8 years, I will have gone from zero dollars to $250,000. It took me 13.8 years to get there. But do you recognize that if I just keep up the exact same behavior, exact same savings, exact same rate of return, over the next 13.8 years, I go from 250,000 to 1 million. 250,000 may not be halfway in dollar terms, but it is halfway in time terms to a million.

Brian: Man, this is why compounding interest is magical is because you’re halfway there. So, yes, it’s only a quarter of the money. It’s 250,000 out of the million dollars, but from a time standpoint, you’re already halfway there because that money is going to start growing upon itself.

Bo: And do you recognize that when you hit the two comma club, once you get into seven figure status, having a net worth of $1 million literally puts you in the top 10% of Americans getting to that milestone. So yeah, maybe a million isn’t enough for you. Maybe your number is 1.6 million or your number is 2.2 million or your number is 4.3 million. If you want to know what your number is, you can go to learn.moneyguy.com and check out our know your number course.

Brian: Bo, I’ve got a great way if you really want to feel special and celebrate your accomplishments financially, especially if you’ve crossed into seven figure status. We’ve set up a website for you. If you just go to moneyguy.com, you can look at become a client because we love celebrating our financial mutants. We call this the abundance cycle where yes, you come here, we give you tons of free stuff. Just go to moneyguy.com/resources. We’ll load you up with all the free stuff, but there will come a day where you realize, man, this simplistic thing that I started has gotten really complicated.

Brian: I’m your host Brian Preston. Mr. Bo Hansen for the rest of the Money Guy team. Money Guy out.

Free Resources

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

There is no need to wait until an arbitrary date on a calendar to make positive changes in your financial life, but if you are...

Articles

Americans aren’t feeling good about their finances. Last year, 16% of Americans said they believed their financial situation would be worse in a year. Now,...

Articles

In 2018 the Supreme Court struck down a law that prohibited most states from allowing sports betting. Gambling on sports is now legal in most...

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

Is passive income really passive? We explain 3 common passive income myths and share our preferred strategy that helps you measure twice and cut once.

Episodes

Are you a Gen Z or Millennial discouraged about retirement? Discover how the vast majority of millionaires got there as regular savers, plus our new...

Episodes

Think your rental barely breaks even? We reveal the shocking math when this couple asks if they should sell their duplex to reclaim their time...

Subscribe to our free weekly newsletter by entering your email address below.