Change your life by

managing your money better.

Subscribe to our free weekly newsletter by entering your email address below.

Subscribe to our free weekly newsletter by entering your email address below.

The dream of owning a home might feel closer than it has in years. We dig into why inventories are climbing, prices are dropping in many markets, and what it means that the average first-time homebuyer is now 38 – the highest on record. We also explore why your housing costs shouldn’t exceed 25% of your gross income, how to use our calculators to see what you can afford, and why buying a home should be a strategic (not emotional) decision. Plus, we share tools and checklists to help you make the smartest move for your future.

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

Brian: Home prices in certain markets are being slashed. What do you need to know?

Bo: Brian, I am so excited about this because finally, it sounds like maybe, just maybe, there’s a glimmer of hope. There’s some light at the end of this housing tunnel because we’re seeing something right now that we have not seen for a while. And I think it’s going to be exciting to a lot of folks out there.

Brian: Well, it’s a long time coming because a lot of the issues with what has driven prices up post pandemic is inventory. I mean, you think about it, we shut down all the supply chains. We lost a lot of people that were in the home building process and you saw inventory kind of taking a toll and you know what happens when you limit the supply of houses available? Prices go up a lot. So, this is a very positive thing to actually see some positive changes in inventory.

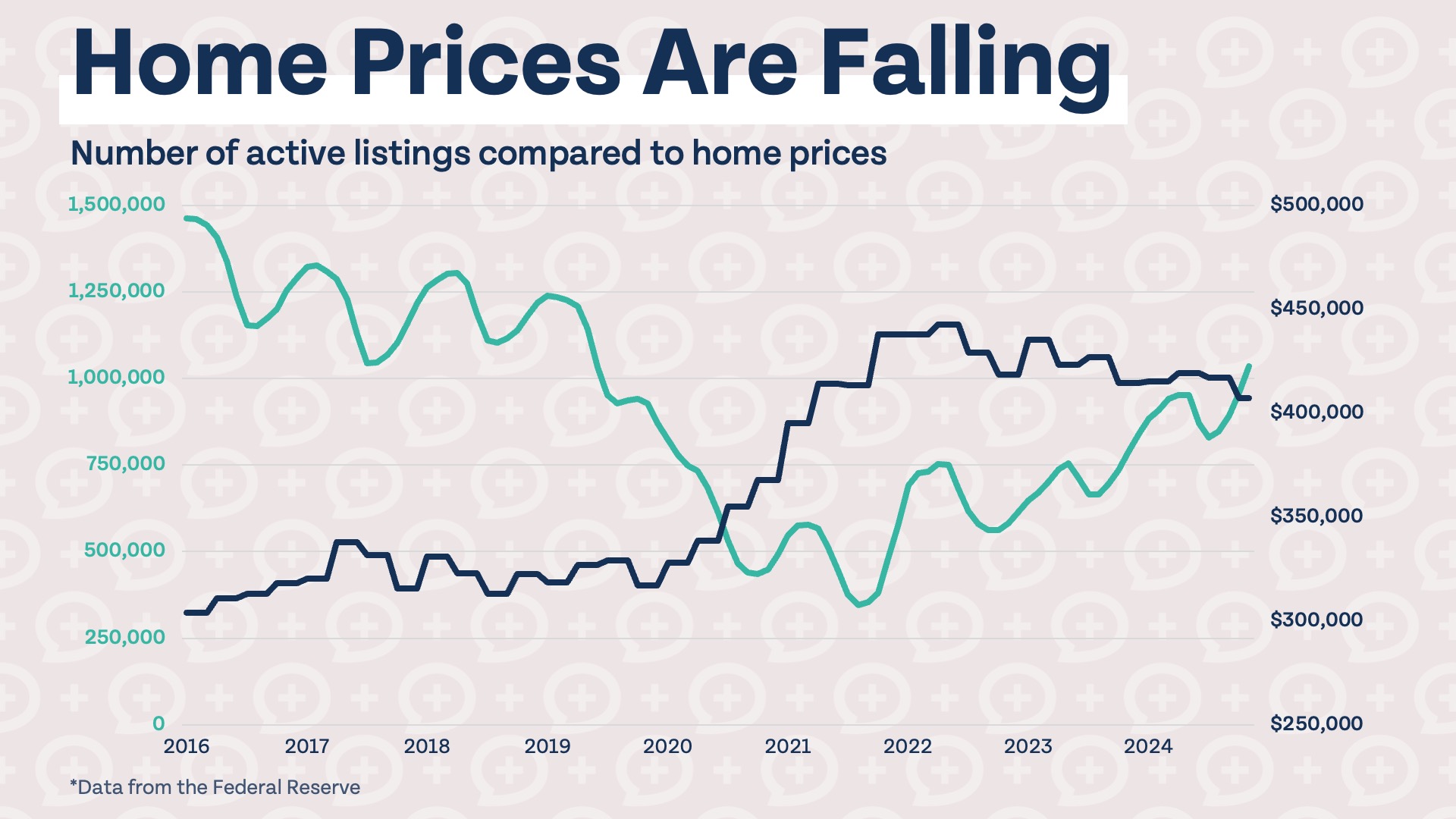

Bo: Yeah. When you actually look at the data itself, and this is data from the Federal Reserve, you can see exactly what happened with the number of active listings from July of 2016 all the way till May of now. It kind of bottomed out right there post pandemic around 2021, 2022, but now active listings have steadily been increasing. We have more inventory. That’s one thing that’s potentially affecting home price. And the other thing is that first-time home buyers right now, this is a thing to know, a thing to be aware of. First-time home buyers are now reaching an age of 38. That’s an all-time high.

Brian: I don’t like that all-time high. That’s why I like any positive information that actually shows that home ownership and pricing is getting better is because I don’t like seeing the stat that instead of it being, because it seems like it was just a blink of an eye ago, it was 33. Now we’re at 38. I don’t want to see us cross into 40 for something that I think is a lot of people’s dream of owning a house, setting roots. It seems to get harder and harder.

Bo: Well, and I think one of the reasons why that number has been pushed up is not only have home prices been increasing, but interest rates have not been super attractive. We know that right now the average mortgage rate in this country is about 6.8%. Now, that’s lower than it has been. It’s been as high as 7 and a half, 8%, but that’s still relatively high. So, it’s making it harder and harder for people to get into homes. So, even though we’re seeing glimmers of hope, it’s still not an easy market for homeowners or for individuals that are not homeowners to get into homes right now.

Brian: Well, let’s actually talk about where the rubber meets the road and the fact that now that we’ve got increasing inventories, we’ve got houses that are sitting on the market longer. It’s led to one in five homes have actually seen price reductions since April or in the month of April.

Bo: It’s been a while since we’ve seen the prices of homes come down. And we know that 32 out of 50 metro areas actually saw a month-over-month decline in the month of May. So maybe, just maybe, if you are someone who’s been trying to get into a home, thinking about buying your first home, thinking about changing homes, you’re now beginning to actually feel like, okay, maybe this thing isn’t sprinting away from me the way that it had been. Maybe now it’s getting to a more reasonable level where I can actually act and actually move on.

Brian: Realize buying a home, it’s not only a financial decision, but a lot of ways it’s an emotional decision. So, I always tell people, don’t feel like you have to get in a hurry. So, just because we’re seeing some positive trends, doesn’t mean you need to run out this weekend and go put a contract in because there’s still some analysis and homework you need to do. So, that way you can take the emotion out of the decision-making and actually see is this something you should do for your best interest.

Bo: Yeah, I think there are some questions that you can ask yourself. The first of which is, do I actually have a need for housing? I think so many of us have been taught, okay, well, graduate college and then I get a career and then I get married, then I buy a house or I start my career and I buy a house and it’s just this natural progression. That’s not necessarily the case. Just because someone else bought a home or just because that was someone else’s trajectory does not mean that that has to be your trajectory. So you want to make sure before you make this giant decision, what for most people is the largest purchase you will ever make in your life, you want to make sure that it is something that actually matches where you are in your financial life and something that you actually need. And then have that, we say this on our home buying checklist, but make sure you have a plan to live there for 5 to seven years.

Brian: It’s back to Bo’s point about achievers. Sometimes they are so excited to get to the milestone of having a house that they’ll house hack and they do other things. And I always remind them, hey, I love all those strategies. That’s a great thing to get into home ownership, but make sure that you’re actually where you’re going to set roots. If part of what is going to make you successful is landing the job in the right area with the right opportunities for going up and getting pay raises and so forth, then buying a house that locks you into that area that might not be ideal is less than the right decision. So make sure you are measuring twice on can you stay in this house 5 to seven years before you make that big decision.

Bo: And then you have to think about the other side of it. Not just the lifestyle situation but also the financial situation. Is this something that you can actually afford? Just because prices have come down does not mean that it’s automatically made housing or home ownership affordable. So there are a few rules that you ought to abide by. And the one of which that we’ve seen the most people run afoul of or ignore in this recent housing market is we want you to keep your total housing cost less than 25% of your gross income. Even with housing prices coming down, if you find yourself where housing is costing you 35%, 40%, 45% of your gross income, you are likely going to be setting yourself up in a more risky situation than you want to be in. And it’s going to prevent you from being able to build wealth the way that you want to outside of home ownership.

Brian: And look, I get it that that 25% can feel kind of constricting because, but it really the whole purpose is to make sure you don’t end up house rich, life poor because a lot of people there’s a risk that you won’t have a lot of money left over if you let all of it go towards housing. And it’s back to that point. We do give a lot of grace on your first house purchases that you only have to put down 3 to 5%. So if you run afoul of the 25%, there’s nothing that says you can’t make a larger down payment if that’s what’s necessary to keep that rule respected.

Bo: And so if you are someone who’s thinking about this and you are someone who’s entertaining the idea of buying a home, particularly your first home, we have a couple tools out at moneyguy.com/resources we want you to check out. One of them is our home buying calculator where you actually can input your variables and it will tell you how much home can you afford. And we also have home buying checklists that tell you here are the things that you want to think about before you make this huge decision. I think that home ownership is a wonderful thing and it makes a lot of sense in the financial lives of a lot of people, but it’s not a necessity. It’s not. I think that so many people operate in this world where I have to own a home, have to own a home, have to own a home, and that’s just not the case. Owning a home can be a wonderful thing for you, but it’s not a necessity to be able to build wealth or reach financial independence. So, you want to make sure if you’re going to make that decision, you make that decision at the right time for the right reasons for your unique situation.

Brian: Well, and look, I’m old man on the porch here. I actually love people owning homes, but it just has to be such a, it has to line up. You have to do the homework. Don’t let it be an emotional decision. Make sure you’re using our checklist. Use our calculators. That’s why moneyguy.com/resources is going to be your friend so you can feel like you’ve done the homework. You’ve done the due diligence you need to do to make sure this aligns with your future goals, but also gives you your best great big beautiful tomorrow in the housing market decisions.

Bo: I love that we get to share this. I love that we get to stay abreast of the things going on out there in the financial world. And I love that we get to answer your questions. We get to weigh into the things that you care about. So, if you have a question you’d like to get our take on, we have the team out in the wings collecting those questions. Make sure you get them in the chat because we do believe there is a better way to do money and we want to load you up with that. So, with that, creative director Rebie, I’m going to throw it over to you.

Rebie: Yeah, thanks. You know, I think it’s interesting. We’ve got a lot of financial mutants in our chat at all varying points of their journeys. 57% said they own a home, meaning that 42% don’t. And so I just thought it was an interesting poll to see that it’s not a sign of financial success or being a financial mutant. So I thought that that was interesting to share. That was straight from our live stream.

Bo: I love that, man. I love when we do things where we get to ask our audience, our financial mutants, information and they share information with us and then we get to synthesize that and share it with the world. Isn’t that a fun thing we get to do?

Rebie: Absolutely.

Rebie: T-Bone says, “Question. My company’s 401(k) match is 50 cents on the dollar with no limit. Wow. Leaving me in golden handcuffs. If I’d like to buy a home in the next two years, what goal should I now have for my 401(k)? I’m 25 years old, married with one kid on the way, a $110k household salary in the DC metro area.” What do you think, man?

Bo: Okay. So, we have gotten variations of this question so many times over the years. You have this thing going on, but man, I want to do this thing or I have this opportunity, but man, I want to do this thing. And I think that the best way to sort of level set on how to approach thinking through this is to remind ourselves that money is nothing more than a tool that allows us to achieve the goals that we have. And one of the things that we have to do as people who are the main characters in this life that we’re living is determine, okay, what are our most important goals? What are the things that we want to move towards the most? And for a lot of people, it might be financial independence. And for some people, it might be, hey, you know what? I do want to achieve financial independence, but before I do that, I’d like to own a home and I want to be able to set roots and I want to be able to grow my family and I want to be able to whatever that thing is for you. And so, it’s okay if sometimes along your financial path, you have to prioritize some goals over the other. So, you might say, “Hey, I really need to save up for a down payment.” And as amazing as being able to build my portfolio and continue to grow and take advantage of this financial independence or maximizing the employer match money to the extent that I can’t walk away from it. And that would be a hard one because that’s free money is you have to ask yourself how important are these two goals and how am I willing to prioritize? You’re about to say something because I can tell you didn’t like that.

Brian: No, it’s just that I think it is a great problem to have but you have to, this is like all big decisions financially have incremental decisions you have to make and opportunity cost. So the first thing let me give you the homework I would go read your plan document so you understand vesting schedules and know how much of this money is truly yours and how fast. So that’s the first thing to know how excited to get. But it is incredibly generous if your employer is truly offering a 50 cents on the dollar all the way up to the maximum you can contribute which is $23,500. So if you think in those terms that’s a guaranteed 50% rate of return. So that’s super powerful. But I also understand so that means if you were prioritizing this in a financial order of operations you’re like holy cow do I never get out of step two unless I’m putting $23,500 into my 401(k). In theory, that’s the way you should think that’s a great maximization opportunity. But understand life happens and we always, there’s two illustrations I want the content team to pull up. I want if y’all could pull up what FOO, what people think FOO looks like versus what it actually is. And as you can see this visual is a lot of people think it’s just an incremental you’re going to go through each step of the nine steps you know in their time and place and you’ll work through it quickly. That’s not the way life happens. Life will happen is that you have steps forward and then you have steps back and it actually will be a walk up the mountain, but you’re going to have some valleys built into there as well. So, buying a house could be one of those things that takes you a step back if you determine that this is so important to you. But here’s the second illustration I need the content team to pull up. I always call it what 25% can do for you, but it’s actually called how much should you save. I would look at where your age is, where you are in life, and see what percentage of your income you should be taking saving to so you don’t fall behind. And that way you can compare and contrast where you are on the intersection point of saving for the future, but then knowing because you can quickly realize, especially if you make under $200,000 of income, that employer contribution is going to be a big thing on that percentage. It’ll let you say, well, hey, if I’m in my 20s and maybe I only have to save, you know, 15 to 17%, I don’t have to do 25% already. It gives me some margin, not feel like you’re sacrificing your future self. But I do want you to feel the pressure that, holy cow, my employer is so generous that as soon as I get this goal funded to get this house, let me get back on this to maximize that 50% because that is going to be your quickest account to reach seven figure status with having an employer that’s that generous with it.

Bo: I love it. Agreed. That’s great. T-Bone, thank you for the question.

Rebie: TheSecondRush has a question for you. How do you stay focused once you’re solidly making wealth? I moved from 10% to a 25% savings rate in three years. Congratulations. But now feel like there’s no clear milestone to aim for. Do I just check back in every 3 years now? 30 years old, married, own a home, 25 years left on the mortgage, and we have no plan for kids. So, what does he do now? I feel like that’s his question.

Brian: Oh, man. I feel like this question is a tee up for some content that we not only had come out last year, but have coming out in the next few months. I’m just going to screw up the title. So, I’ll just leave it for you.

Bo: Yeah. So, here’s the thing I would tell you to do. First thing I would tell you to do, Second Rush, is I want you to subscribe right now to the channel because we do have a show coming out that’s going to walk you through milestones that you ought to be looking for and thinking about as you move through your portfolio. There’s some really exciting milestones that we hit on our journey to financial independence. So you said the question you asked is okay, well, how do I stay motivated? Because one thing is just understanding what milestones are. One of my favorite things in the world to do and I know it’s Brian’s too is every single year we do an annual net worth statement. We do ours at the end of the year 12/31 where basically we list out all the things that we own and then we list out all the things that we owe and we calculate the difference and we track where we are. Well, one of the things that makes us stay motivated is even if your savings rate is in a good place and you were saving 10%, now you’re saving 25%. As you begin to see that snowball roll down the mountain and get bigger and bigger and bigger and bigger, you’re going to start seeing some really fun stuff starting to happen on your net worth statement. And that the result, the product of that is that motivation that gets you to next year. Like, okay, oh, I saved 25% next year, but man, if I can do that again this year, my portfolio made this last year, I can. Man, if you are actually tracking it and keeping an eye on it, rather than just checking in every three years and saying, “Okay, well, I guess I’m doing okay,” find a way to do an annual net worth statement. By the way, if you need a tool, you can go to learn.moneyguy.com and check out our tool. And it even puts on there some really fun stuff in addition to just tracking your net worth. It’ll show you like, okay, here’s what my liquid assets are doing through time. Here’s what my money guy accumulator score is. Here’s what my journey to abundance looks like. All those are exciting little metrics that will allow you to stay motivated and recognize the areas in your life that you can still get excited about even when things seem to be on autopilot.

Brian: And that’s the only thing I was going to add is that I love the dashboard view that the net worth tool does because it really does take the net worth statement to another level because not only, plus you get to see the three buckets. You get to see how much your money is in tax deferred, how much is in tax-free like Roth assets, how much is in after tax. I mean, those are the type of things that I’m always trying to look at. I love the pay down debt schedule, you know, because I love kind of seeing where debt is going on my net worth every year in comparison to the liquid net worth, and then even putting your total net worth, which includes all the stuff that you can’t necessarily eat like your house and your cars. But it’s definitely a valuable resource to keep you motivated. And then that’s why I do like those milestone shows is because you know part of what we try to give you here is the why component as well is that what is your money supposed to do since it’s only a tool. Well part of the 25% is to free you to get outside of the analytics of this and live your best life. So I would go through some of the soft exercises of what is this? What why am I saving? What am I saving for? This is all part of step seven of the financial order of operations. If you haven’t gone and checked out Millionaire Mission, I really, like I said, that chapter is the chapter that really sets up, thank you, Bo, for the prop. Chapter seven, you know, when we talk about step seven, hyper-accumulation, it really does give you the why exercises so you can stay motivated, but then you get to from there, you get to do what you want, when you want, how you want. You know, if you want a nicer vacation, you want to drive a nicer car, you want to get into residential real estate or commercial real estate, this is going to set you up to kind of do those type of things, but it’s not supposed to feel constricting. It’s supposed to feel freeing that now you get to go live your best life. I feel like so many things out there in the financial world, people get caught up in, you know, I have to be so rigid and to do this is going to say no and take away. I want you to have that abundance mindset where we’re going to do this. So now we get to do more and you get to live your best life both in this decade plus the decade as you save for your 50s and 60s. You’re not going to have regrets.

Rebie: Love that. Excellent. Well, TheSecondRush, thank you for your question. I hope that helps you think through what to do next.

Rebie: Millennium Interests has a question. What’s your take on the current projections from Vanguard showing a 0 to 3% real returns for the US stocks over the next decade? I know the mantra is to always be buying, but does this impact strategy?

Brian: Can we put, I need to get on the calendar the date that Vanguard puts this out because I feel like every year I get to answer this.

Bo: Oh, yeah.

Brian: This is what and I think it’s brilliant on Vanguard’s part in the fact that they post this, they get all kind of press on it. I mean, so it gets a lot of attention, probably a lot of eyeballs, a lot of clicks go to Vanguard’s website. But the thing is is that I just shared with you guys and you know, if this turns into a highlight, that part won’t show up. So I’ll reiterate it one more time is we just came through a 20% recovery in the last quarter. I mean, do you think about that? And here we are sitting at the point we’re recording this where we’re, I mean most the indexes like the S&P 500 are up right around 5%, 6% I think year to date after having an 11% second quarter. So to hear 3%, I’ve been hearing 3% by the way last year I heard 3%, the previous year Vanguard you can almost set your clock to the low expectation setup that Vanguard does and the truth is they don’t know. If you’ve ever seen the analysts that predict interest rates, the analysts that predict where the equity market’s going. I would much more look at what is the historic normal return that you see out of these index funds. And then think about the law of accelerating returns is that as innovation and technology and economies continue to expand, how are you going to be able to capture that? Don’t try to beat it, but can you just be part of that growth? That’s what I’d be focusing on. So yes, once again concludes always be buying. Making it automatic for the people is definitely one of those things you ought to be empowering and taking charge of.

Bo: I just get so frustrated because I feel like this happens over and over and over and over again. Well, I was rapidly doing some research over here because what I remember is it was like circa 2010 maybe something like that when I remember the Vanguard article coming out. You never can find the old history of it. I couldn’t. Were you able to find it? Just found it, bro. You ready for this? Good for you. So, because well, I was thinking about I was trying to remember what year it was. And if you remember, you know, 2009 was a recovery year coming out of the Great Recession and the market went even though it was down really bad at the beginning, it went gangbusters. And in 2010, Vanguard came out like, hey, we’re going to expect lower, you know, lower returns moving forward. And it gave a number of different reasons why that was the case. So, I just went and asked, hey, what was Vanguard’s investment outlook in 2010 moving forward? And it said, in 2010, following the 2008 crisis, Vanguard published research suggesting that the annualized real returns over the next decade would most likely be like 6% for stocks and 0 to 2% for bonds. So, you think about if you had like a diversified portfolio there, you’re earning less than 6% moving forward. I just very quickly said, hey, what was the annualized rate of return since 2010 for the S&P 500? And in reality, it has been like 12 and a half to 13 and a half percent annualized. Double what Vanguard said. And so I think what ends up happening is my guess, and I don’t think you said this, but my guess is they operate under the assumption, hey, we’re going to overpromise and we’re going to underpromise and overdeliver. No one’s going to be mad if we tell you the outlook for the stock market’s going to be 4 to 5% and then the outlook actually turns out to be 9 to 10. But if we say it’s going to be 9 to 10 and it turns out to be 5 to 6, well then everyone’s going to be up in arms. So they’re setting themselves up not to let anyone down. When in reality, law of large numbers would suggest if you look at the way the market has performed for the last 40, 50, 60, 70 years, it tends to be pretty consistent. There are ebbs, there are flows, there are ups, there are downs. We have a great illustration. And this is not one we have in the coffers, but shows like if you just look at market performance on a year-by-year basis, it’s absolutely chaotic. There is no rhyme or reason to how it works. But if you then look at three-year rolling periods and then five-year rolling periods, and then you look at 10 and 20 year rolling periods, it becomes very, very, very, very consistent through time. You just have to give it time to do that. So, I’d be careful letting someone else tell you they know what the future’s going to hold because I don’t think that that’s the case. What feels risky in the short term historically in the long term can be much safer because it protects you from inflation and other things. And then what feels safe in the short term can actually be very risky in the long term because of those exact same factors.

Rebie: Yep. It’s not about what you feel when it comes to the stock market. That’s what I heard.

Rebie: Donovan H says, “Have you heard of the extra mortgage payment a year to help lessen the principle of the loan to lower paid interest? Would you recommend this strategy for a household currently in step six of the FOO?”

Brian: This is a common trend. And look with interest rates being where they are on houses, you know, if you’re paying the 6.8% right now, obviously this is a good strategy as long and I love that you shared that you’re in step six. I’m not a minimum payment type of person myself. So I’ve been rounding up my payments for years. The difference is and this is where Bo’s going to jump in. That’s why he wanted me to go first is so I could fall into the trap and then he could snare me and make fun of me. I mean I have a 2 and a half% mortgage by the way and the mortgage is, I just pulled it up because I had an insurance claim and we had to do this stuff and I had to get the insurance, the goofball mortgage company involved even though I owe $50,000 on my house. But I even told the insurance adjuster I was like I want to just write a check to pay this thing off. But I was like it’s just so hard when I owe 2 and a half% interest.

Bo: Yeah. I’ll tell you the way that I did it. I love I love that answer because there’s a mathematical approach to this, right? Mathematically, okay? Yes. Can I pay an extra mortgage payment and pay down my mortgage faster? Yes, that is true. And that is a strategy. Is that optimal? Well, it depends on what your dollars could earn outside of the interest rate you’re paying on your mortgage. So, there’s an arbitrage situation. If you’re someone in your 20s, there’s a good chance that you could put your money to work and it could have a higher rate of return than what you’re paying on your mortgage. So, there’s a positive arbitrage situation there. Having said that, I think a lot of people play like little mortgage games and I’m not going to fight you on this. And so maybe your mortgage game is I make one extra payment or maybe your thing is I pay every two weeks. I’ll tell you mine and I’m not even a mortgage prepay kind of guy. I round up. So every year, you know, property taxes and insurance or whatever. If my mortgage payment comes out and say that it’s like, you know, my mortgage was $1,900, I round it up to $2,000, right?

Brian: He won’t give us his real mortgage payment. I love it. He got himself in a pickle there. He’s like, “Do I tell him my real mortgage payment?” You know, our smart audience is going to back into how much mortgage. You see how clear that?

Bo: So, yeah. So, I round up again. It’s not a strategy to prepay and I do it just so I can in my mind mentally account for what my mortgage is. But if those sort of things allow you to stick to your plan and make you feel good about the decisions you’re making, I’m not going to fight you on that. But if you’re doing that, if you’re doing that extra mortgage payment instead of your Roth IRA or that extra mortgage payment instead of your HSA, then I start to have a little bit of pause and think that maybe you’re operating suboptimally.

Brian: Do you think I’m at the point I should just pay off the mortgage since it’s down to $50,000?

Bo: Yeah. I mean, I honestly think so. I mean, just because like, you know, we’re at the point I hear so much about it, right? You know what I mean? It’s a meme at this point. You’ve been like, I think I might pay it off.

Brian: What’s funny is Megan’s sitting over there and I remember when we were starting the book tour, you know, which was June of over a year ago, basically a year ago, I was like, my goal is I’m going to have the mortgage paid off so that I don’t, so I can tell everybody on the tour that I paid off the mortgage, but for some reason, I just didn’t do it because that 2.5% just really I mean, I would have thought interest rates would have been down further now on cash. So, it was going to be a much easier decision. But yeah, you can still make if you know where to put the money, you can still make over 4% on your cash. It seems crazy. I kind of, there are a lot of financial things though where I kind of subscribe to the Forrest Gump methodology of hey, it’s one less thing. So even though like at where your mortgage amount is right now, you know, just pay it off and hey, it’s just one less thing. You know what I mean?

Rebie: I agree with that where you are, just pay it off. One less thing. Let us know if you decide to actually do it. Keep us posted. We’re going to live through this first live stream you paying it off clicking the button.

Rebie: It’s from Carrie. She’s 45 years old with a 2-year-old and a four-year-old kid. I will be 59 plus when they need funds for college, etc. Is saving extra money for this in my Roth 401(k) and Roth IRA okay? It seems more flexible and lower cost than a 529. Thanks.

Bo: So here my question would be what caused you to draw the conclusion that it’s more flexible and lower cost than 529s? Because 529s have changed a bunch over the years and now 529s I think they’re offered by all 50 states, right? You can actually do one in all 50 states depending on the state in which you live. Because by the way we love Roth IRAs and we love Roth 401(k)s. We love the fact that you put the money in and it can grow tax deferred and if you draw it after 59 and a half you can actually pull the money out completely tax-free. But for a lot of people, if you live in a specific state that has state income tax, there’s a chance that not only can you get that same Roth type benefit for 529 tax-free growth, you can also get a deduction on the front end if your state has an incentive for doing that. So Carrie, not knowing what state you’re in, that would be one of the considerations I would make is, okay, should saving to a 529 be part of my strategy? Because there’s an extra little tax benefit there that I want to do. Now, here’s what I want to make sure you’re doing. Saving for that college education needs to come above and beyond what you were already saving for your future financial independence. Meaning, this is like after you’re at your 25%, do I want to save even more to my Roth 401(k) or even more to my Roth IRA? And I bet if you think through it that way, by the time you get through your Roth IRA, you’ve already saved $7,000. Well, you can’t really use that because that’s going to be like financial independence money. And so maybe depending on your income inside your Roth 401(k), yeah, maybe you could plus that up some if you have room. But there’s a good chance if you’re saving 25% doing the thing that you’re supposed to be doing, you’re going to need the 529 capacity anyways to make sure you’re not actually cannibalizing your future retirement assets to pay for college.

Brian: That’s why I think you have to keep them separated. I mean, that’s why I love the because they have different goals. I mean, 529s and college savings is a step eight. You know, these abundance goals, prepaid future expenses, whereas your Roth IRA, your Roth 401(k), those are steps five and six of the financial order of operations. And what I worry about is if you are just throwing them all into the Roth assets and you think you’re going to create some weird dynamics for yourself in the future is because first of all already every person I know who has Roth accounts, it’s like you’re precious. You don’t like to pull money out of those. You’re hoping you die with those and then your beneficiaries get to, you know, let them grow for 10 years before they pull out of them. So Roth assets become very valuable and you just don’t want to walk away from them. I mean, I just worry you get a false sense of security because your accounts are going to look so good, but then you start pulling this money out for college and all of a sudden you gutted, you know, one of your biggest retirement assets. That’s why if you keep them separated and they have a goal and a purpose, you won’t do that mental accounting where you have a false sense of security. Because maybe sometimes to save more for college beyond what you have to do for yourself in retirement is kind of a selfless act. It’s going to require discipline and require some sacrifice. I don’t want you just feeling like hey I’m loading up my Roth. I’m loading up my 401(k). This will also cover college and then like I said you got it and whereas maybe if you’d have started a little earlier and felt the pressure of keeping them separated and knowing man in addition to my retirement I got to save for the kids college you might have made some different decisions on your consumption on your lifestyle. So I like keeping those things separated so those goals can live each their best life but be accounted for appropriately so you don’t get this convoluted jumbled up all for one goal out of my Roth account.

Rebie: Tyler H says, “I was saving for a large expense that I ended up not having to pay. I saved around $20k and I have also right around $20k of high interest at 8.6%. Should I just use the full amount to pay off the debt?”

Brian: This is the easiest one. Yes. Yes. Well, I mean, wait a minute. First, obviously go through the financial order of operations. What do you have in steps one and four? But without a doubt. I mean, if I had 8.6% and this was money above and beyond emergency reserves, extinguish it. You know what?

Bo: Yes, agreed 100%. Just behaviorally, one of the things I’d like to think about, Tyler, is this large expense that you were saving up for. I don’t know what the expense is. Behaviorally, though, I would ask myself, man, if it was saving up, oh, I’m going to buy a new car or I’m going to pay for a trip. I’m going to do whatever. Was saving up for that appropriate given the fact that you have $20,000 of high interest debt at 8.6%? I just want you to think through because there’s a good chance that if it were a large discretionary expense, it was a want, not a need. You probably should have knocked out that debt before saving for that because what I don’t want to see happen again is you’re going to do this. You’re going to pay it off. I don’t want to be in a live stream three years from now and all of a sudden Tyler H asked a question like, “Hey, I got this high interest debt again.” Like, I want you to break that cycle. I don’t know where it came from or what happened. But the fact that you were saving up for another expense while you had that debt, I just, and look, it may all be completely on the up and up, but it’s certainly worth taking a moment, having an assessment, and saying, man, okay, am I doing, am I thinking about my money the right way? And you may very well be, but it never hurts to just kind of work through that exercise to make sure that you are.

Rebie: All right. Good stuff. Tyler H, thanks for being here. Thanks for asking the question.

Rebie: KYPA has a question. It says, “Can you break 20/3/8 if you’re not paying rent? I’m a college student who’s working part-time and I bought a used car. Is it okay to break the rules in this case?”

Bo: Well, you’re not going to get arrested, right? I mean like everyone asks hey guys can I do this? Sure it’s your life you can if you want to. You can do 17/19, right? But here’s what you should do is it what you should do? Can you go if you’re living at home with your parents can you go buy that convertible Mercedes that you’ve always wanted that will make you look really cool to your friends? I mean you can, you physically can. The question is it’s a should question. It’s a should question. Is it okay?

Brian: I just don’t think I mean because I think that it’s a life lesson is if you’re going out there and using this opportunity, it is an opportunity if you’re living at home and don’t have to pay rent that do you realize how you could just be spending money stacking in the background and running through the financial order of operations very quickly. But it just seems like a wasted opportunity if you go buy a nicer car. Just so in this moment in time, you can say you’re a car person, but man, I just know as a person who’s now in my 50s, consumption decisions like cars and those type of things just seem so just empty compared to having money in the bank so that I can live the most flexible and own my time and do what I want, choose to be what I’m involved with. That’s going to pay so much more life dividends than just the feel-good moment of in your 20s or even younger. I don’t know how old this individual is since they’re living at home, but of driving a fancy car.

Bo: Yeah. I just, I don’t know the 20/3/8. It’s there because it’s a helpful metric to help us, but some of it’s also to protect us from ourselves. If you find yourself in the situation like, man, I can’t save up 20% for this car. Maybe you can’t afford that car, man. I can’t get the payments inside of three years. It’s just too expensive. Maybe you can’t afford that car. Man, if I do this 8%, that’s going to be too high. Okay, maybe you can’t afford that. Some of it is to protect us from ourselves, to make sure that we don’t prematurely make financial decisions that we are not ready to make. Because I don’t know your situation, your circumstance, but there’s a really good chance if we were to fast forward 20 years in the future, I just don’t think you’re going to look back and say, “Man, I’m so glad I bought that more expensive car that had that higher payment with a higher interest rate.” I think you’re probably going to say, “Man, I’m glad I made those wise, prudent decisions so that now at this stage of life, 20 years in the future, I can go buy that nicer car because I get to pay it off all in one year, same as cash, and I’m not actually faking it. I’m actually in the financial situation where I can do those.”

Brian: Well, I think it’s important. It’s a mindset issue is that you quickly realize when you’re young that the system is not going to protect you. It’s actually designed to help you consume more of you. If you think about what’s going on with car loans, where the average car loan is beyond $700 a month, the term of car loans has gotten where it’s what was it, six years, close to six years now. You quickly realize the guard rails are not there. So, it’s on you to develop the behaviors and the systems to set yourself up for the future because nobody’s coming to rescue you. Nobody’s coming to save you. So don’t, that’s why it just troubles me when you’re in this moment of opportunity especially when time you’re a billionaire of time depending upon how young you are where you can totally own the system that much sooner and if you fall into that consumption trap and you know and let the system with the siren song of you’ll look so cool, your friends will love you more. Whatever the thing is that’s enticing you to live this fake life. Remember it’s better to be rich than to look rich. And I’m just telling you, don’t fall into those consumption traps.

Rebie: That’s great. Good stuff. And as usual, KYPA, we appreciate you being here and asking your questions so that we can chat about it on the show.

Rebie: Let’s do another question from Codiferus. It says, “Can you explain if a solo 401(k) is better than a SEP IRA for a 1099 employee?”

Bo: Yes. Okay. I can’t explain it. Okay. Yes, I can explain it. I thought he was saying yes, it’s better, but yeah, can you explain? Yes, he can explain it. You’re the CPA, man. Walk us through this.

Brian: Well, I mean look they there used to be some subtle differences that made SEP IRAs better than solo 401(k)s for certain people is like if you’re a procrastinator and you made a little extra money, you get to go do your taxes and the accountant or tax preparer is like, man, we got to find some way to lower your tax bill. You could whip out your handy-dandy SEP IRA and it was like a time machine. You go back in time, let you set it up as long all the way if you extended the return all the way up until April, I mean October 15th. Well, now they’ve updated because the solo 401(k)s in the past had to be set up by year end. Now they’ve changed that. You can actually go back in time. I don’t think you can go back in time on your salary deferrals. Is that because that’s the W-2 decision if you’re a W-2 employee? It depends on if you’re W-2 employee, depends on how your compensation is structured. But and realize the contribution from a SEP and a solo on the profit sharing side are pretty much the same thing because it’s a version of your net profit after you take into account self-employment taxes or payroll taxes. So that’s why it’s so funny I’m old enough that I’ve seen so much of the system progress is because when I was younger this sounds so ridiculous but SEP IRAs were the go-to for everybody. And then you know, you saw people then transition to solo 401(k)s. Now it’s gotten to where I think solos just dominate this process. Now, the only thing remember with solo is there’s some caveats we got to talk about. It’s only the only employees for the company can be you and your spouse. If you have even if you got like your kids working for your company, that kind of blows this all up. You got to go traditional more of a you have to have a plan document and all the other things that go with a 401(k). SEP IRA you still if you have employees can still use it but you realize whatever you do for yourself as a percentage you have to do for your employees at that same because it’s an employer-only contribution. Your employees are not making any contribution when you do a SEP. It’s all employer only funded. Solos are a mix because it’s not only the employer portion which is the profit sharing but it’s also your salary deferral which is at $23,500. If you’re 50 and over or you’re turning 50 this year, you get that catch-up of $7,500. Did I get all those numbers right? Look at me.

Bo: Only thing I’ll add to that is are solos better than SEPs? In our experience, solos allow you to save more money at lower incomes than SEPs. So, if you have a $30,000 income or $30,000 net profit coming through with a SEP IRA, you’re only going to be able to save about 20% of that as an employer contribution. Again, it depends on how you’re compensated. With a solo 401(k), you can do a salary deferral all the way up to $23,500 of that $30,000 plus you can do a profit sharing contribution based on the net operating profit. So, at high incomes, you can save the same in both. You’re going to run into the section 415 limits. But at lower incomes, solos allow you to save more. So that’s why they often have more advantage. Another big advantage to solos, if you have a solo 401(k) and you’re funding that, you will not run afoul of backdoor Roth pro-rata rules. If you have a SEP IRA and you’re trying to do backdoor Roth, you’re going to kind of run into some pro-rata rules you have to think through. So it provides a planning opportunity there. And now some custodians actually offer Roth solo 401(k). So, not only can you do salary deferrals in there, you can do Roth salary deferrals into your solo 401(k), which is kind of an interesting thing. Now, here’s the one caveat you need to be aware of. Brian, you started to mention this, but I don’t think you mentioned this exact one. Once your solo 401(k) gets over $250,000 of combined assets, and that’s you and your spouse, then you have to annually file form 5500 before July 31st every single year. Now, there are no taxes due. There’s not like a cost to doing this, but there are penalties if you fail to do it. So, you have to make sure that if you are over $250,000 of total assets, you are filing a form 5500 every single year, either having your accountant do it or you doing it directly. So long as you make sure you’ve checked those boxes, they are a fantastic and wonderful savings opportunity for you.

Brian: Well done. I mean, I was sitting there going, man, every one of I was like, I don’t think I left much meat on the bone for Bo and then you came back and on top of it. That’s what dynamic duo, love to see it.

Rebie: That’s why, you know, that’s why we’re here every Tuesday 10:00 a.m. Central. So, be sure you subscribe not only to know when we release personal finance videos, but also to know when Brian pays off his mortgage if he ever does.

Brian: I am. Keep you posted. We’ll come back. The suntan version of myself is going to pay off the mortgage.

Brian: Guys, remember a lot of the why, money is only a tool. We want it to so you can live life on your terms. Do what you want, when you want, how you want, and really kind of know what you value and how to own your time that much sooner. That’s what we’re creating here. So, go to moneyguy.com/resources. And then if you have, because realize we give you so much free advice that a lot of you like, what’s the catch here? Here’s the catch. It’s called the abundance cycle. We recognize we can give you all this simple advice that is going to create true abundance for you, but just natural success is going to create complications. And when that happens, we’re going to leave the porch light on for you. And we hope that you will fulfill the abundance cycle and consider giving us a shot to be your fee only fiduciary financial advisors. I’m your host, Brian Preston, Mr. Bo Hanson, Rebie, and the rest of the content team. Money Guy out.

Free Resources

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

Homeownership has long been associated with the American Dream. 64% of Americans say owning a home is one of their life goals, and 50% say...

Articles

The Trump administration recently proposed offering homebuyers the option to choose a 50-year term for their mortgage, which they said would be a “complete game...

Articles

As mortgage rates have held relatively steady over the past few years, with average fixed 30-year rates between 6% and 8% since September of 2022,...

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

We react to viral finance chaos: saving young is dumb, Roth IRA scams & sports betting schemes.

Episodes

Can saving too much money actually hurt you? Discover five situations where good savers make costly mistakes, from cash sitting idle for years to relationship...

Episodes

Real estate isn't as passive or profitable as TikTok claims. Brian reveals 5 uncomfortable truths about real estate investing & the most dangerous trap investors...

Subscribe to our free weekly newsletter by entering your email address below.