-

▼

-

▼

Tax evasion? No way! Legal tax avoidance? It isn’t just legal, it’s encouraged by our tax code. However, the playbook changes dramatically with each decade of life. In this episode, we break down the age-specific tactics to legally minimize your tax bill, revealing the advantages of Roth accounts for 25-year-olds, how proper tax bucket structuring in your 30s can mean the difference between paying $25,000 or just $4,000 in taxes on the same $200,000 retirement income (that’s $20,000 more to spend every year!), and why strategic Roth conversions during your 40s can save between $600,000 to $1.3 million in lifetime taxes.

But here’s the plot twist: what works at 30 could sabotage you at 50. From the often-overlooked $2,500 student loan interest deduction in your 20s to the magical 0% capital gains rate when income dips below $97,000 in your 40s, to the complex choreography of RMDs, QCDs, IRMAA, and Social Security taxability in your 50s and beyond, each decade demands different strategies. Watch the full episode to discover which tactics apply to your age right now and learn why timing these moves correctly could be worth more than your actual investment returns. For more tax planning resources and strategies, check out our Ultimate Tax Guide, as well as more free resources at moneyguy.com/resources.

Enjoy the Show?

Where You Can Watch and Listen:

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

- Episodes of The Money Guy Show every Friday

- Episodes of Making a Millionaire every other Monday

- Mini-shows every Wednesday

- Ask Money Guy Livestreams every Tuesday

- Tons of other fun content!

Introduction – Tax Avoidance vs. Tax Evasion (0:00)

Brian: Here’s the thing. Tax evasion completely illegal. However, tax avoidance, legal tax avoidance is very smart and it’s actually encouraged by our current tax code.

Bo: Brian, I am so excited because today we’re talking about strategies to help you pay less in taxes. And this looks different depending on your stage of life. So, in true Money Guy fashion, we are going to break it down by age.

Brian: With that, let’s dive right in.

Your 20s – Don’t Overcomplicate It (0:34)

Bo: All right, Brian. So, let’s talk about how to beat the IRS specifically at the beginning of your financial journey in your 20s. And I think the first one, I think this is counterintuitive to a lot of folks at this stage. Don’t over complicate it.

Brian: Well, yeah. Look, I mean, a lot of things have changed just in my time that I’ve been dealing with taxes is that now the majority of us are just going to take the standard deduction. Matter of fact, 91% of taxpayers choose to take the standard deduction in 2022 is the most recent data that we have from the Tax Policy Center. And that makes sense because the standard deduction after recent legislation a few years back has actually made it where the numbers are high enough that it captures most people.

Bo: Yeah. While you could go out and itemize and you could go try to find those deductions for most young people, it’s going to be really hard to get over the standard thresholds. If you’re just looking at 2026 numbers, the standard deduction for a single filer $16,100, for a married filing jointly filer over $32,000. So rather than trying to spin your wheels and track all these expenses and figure out what you’re going to do from a deduction standpoint for a lot of folks, keep it simple. Just take the standard deduction. You’re likely going to be exactly where you need to be.

Brian: This next tip, get your employer match. Look, this is step two of the financial order of operations. It’s a two-fer because we absolutely love the free money that your employer’s loading you up with. But here’s the thing. A lot of times these employers are going to require you to do they’re going to do a 50 cents on the dollar or a dollar-for-dollar match. When you put that money into the system, there’s some tax benefits that actually come from those contributions as well.

Bo: Yeah. So, not only is it free money, there are tax advantages as well. And then once you’ve gotten that free employer match, we want you to prioritize your tax-free accounts. So, these are things like your Roth IRA, your Roth 401k, your health savings account. These are wonderful mechanisms because even though you don’t get a tax deduction today, unless you’re doing the HSA, those dollars grow tax deferred, and then assuming you make qualified withdrawals, you can actually take that money out completely tax-free. It is literally a way to legally hide money from the government forever. So, if you’re not prioritizing the tax-free accounts, there’s a good chance that you’re missing out on a bunch of huge tax savings opportunity.

Brian: Look, there’s going to be people that say, “Yeah, but you’re paying the taxes now versus…” That’s a feature. That’s not actually a thing that’s working against you. Because for a lot of you, you have literally decades of growth. We want to lean towards compounding growth and seeing all that compounding growth tax-free. Super exciting and super powerful for you.

Bo: And then another reality when it comes to taxes for a lot of folks in their 20s is that we know a lot of 20-somethings have student loans that they’re currently working on knocking out. Well, don’t forget for certain taxpayers, you can actually deduct your student loan interest. You can deduct up to $2,500 of interest paid on qualified loans during the year or whatever you paid in those loans, whichever is lower, assuming you meet certain income thresholds. There are incomes that once you cross over those, you cannot deduct. So, if you’re someone paying student loans and your income qualifies, make sure that finds its way onto your tax return.

Brian: And this doesn’t require you to itemize. This is something that you get to do whether you’re itemized or whether you take the standard deduction. This is outside of that. So, make sure you take advantage of the opportunity.

Your 30s – Being Intentional with Three Tax Buckets (4:09)

Bo: So, the theme in your 20s is don’t over complicate it. But now, as we move into our 30s, things do get a little more I don’t want to say complicated, but they do get a little bit more nuanced. So, how do you think about in your 30s lowering your tax bill and beating the IRS? So, I think the first thing is you have to be intentional. And specifically, we want you to be intentional with your three tax buckets.

Brian: Yeah. If you’re not familiar, and by the way, we build a lot of this into the financial order of operations. The three tax buckets are your three different tax accounts. You have tax-free, which are your Roth accounts. You think about your Roth 401k, your Roth IRAs, and we even put the health savings account in this because you have to have access to a high-deductible health insurance plan. That’s its own choice. But still tax-free growth is an opportunity. And then we have our tax deferred. This is typically where your employer contributions and other things as well as your traditional IRA that you’re making pre-tax, they go in tax deferred. And then that third bucket is after tax and that’s going to be your taxable brokerage accounts, those bridge accounts that hopefully after you build up all the tax-free, the tax deferred, you’re probably going to start dumping money into those after tax because that’s going to be the easy access accounts if you are part of that retire early community.

Bo: Now, a lot of people say, “Guys, does this really matter?” I mean, I hear you talk about the three buckets, but in practical terms, is this even a significant thing to think about? We want to show you that when you’re in your 30s, we want you to begin with the end in mind. We want you to think about the future. And that’s why the three tax buckets matter. So, let’s think about two taxpayers. Let’s say that we have Inefficient Ivan and Manny the Mutant that have both made it to financial independence. And in their financial independence, they’re going to live off of $200,000 of retirement income. Now, Inefficient Ivan, he just spent his entire career maxing out the 401k, which is great. He just put money in his 401k and saved on a pre-tax basis, but never really worried about the three tax buckets. Manny, on the other hand, followed the financial order of operations. And so he had his pre-tax bucket and his tax deferred or his pre-tax, his after tax and his tax-free bucket. So when they get to retirement and when they go to begin living off of their assets, Inefficient Ivan, even when he starts collecting social security, is going to pay ordinary income on all of his income. Every dollar he pulls out of that pre-tax account is going to be taxed as ordinary income. Manny the Mutant is different. He pays ordinary income on his pre-tax withdrawals. He pays ordinary income on his social security, but the after tax account, the bridge account, the brokerage account has favorable tax rates and obviously the Roth and HSA are going to be completely tax-free. So if we think about what their actual tax returns would look like, Ivan is going to be in the 22% marginal bracket and because we work in a progressive tax system, his effective rate is going to be just under 13%. That means that on his $200,000 of retirement income, he’s paying a touch over $25,000 in taxes, which means he has about $174,000 to spend. Compare that to Manny, who is literally living off of the exact same income. He’s only in the 12% marginal tax bracket. Again, we’re going to work through a progressive tax system. His effective tax rate is only 2%. Which means because he focused on the three buckets, he only pays $4,000 in taxes, which means he has $196,000 to spend in retirement. Almost $20,000 more than Ivan simply because he built his accounts and his account structure super efficiently.

Brian: This is why it’s so important. We always say, look, we can give you tons of free advice because you can have the desire to keep your financial life super simple in the beginning, but tax policy, tax and tax planning is definitely going to complicate your life. And we always talk about this is a choose your own adventure. If you do this right, if you maximize the financial order of operations, if you’re paying attention to where the intersection is on what the marginal tax rates you’re paying, what the savings opportunities are, if you structure it right, you can actually legally manipulate the tax code at the end of your retirement because you get to choose which accounts am I pulling from, how am I pulling from, because by the way, we didn’t even mention on here, a lot of our clients will also have health savings accounts with a lot of reimbursements that they’ve never taken. So if they need to keep tax rates low so they can get zero capital gains on those after-tax accounts, guess what? They have a pot to go pull that money out of to help fund that retirement. The maximize all the planning because when you’re in the workforce, you just don’t have that much ability. Your earned income is high enough that it’s driving you up into those high tax brackets. But when you retire, you get a lot more flexibility and you get to choose how you want to do your taxes and still stay on the right side of the law.

Your 30s – Child-Related Tax Breaks (9:08)

Bo: Another thing that happens for a lot of folks in their 30s is this is where we begin to grow families and start to have children. And so one of the things when it comes to tax policy we want to make sure that you’re not forgetting is that there are certain child-related tax breaks that you ought to be aware of and that you should be taking advantage of and a lot of them have changed a touch over the past couple years.

Brian: Well I mean let’s talk about the big one child tax credit guys and by the way you heard me say credit. I didn’t say deduction I said credit. What I love about credits is they are a dollar-for-dollar reduction in the taxes you owe. So for instance, under the new one big beautiful bill that came out last year, it updated the child tax credit to where now it’s $2,200 per qualifying child beginning in 2025. So take for example, somebody who pays $8,000 in taxes or is supposed to pay $8,000 in taxes before the qualifying credits. They have two qualifying children. And right away, their tax bill has dropped by $4,400. Do you see how powerful it is? So, make sure you understand what you qualify for by just having children. And that’s just the tip of the iceberg on this thing because that’s your child tax credit. Bo, there’s also the dependent care flexible spending account.

Bo: Yeah. This is basically a pre-tax account that you can use to go pay for child care while you work, up to $5,000 per household. You can elect at the beginning of the year. I want to fund this account. $5,000 pre-tax and I’m going to use that to go provide care for my child. And it can be used for things like daycare, preschool, before or after school care, or even sometimes like summer day camps if you need someone to have child care while you’re out working. But it’s usually a use it or lose it. Meaning, you don’t want to put more into the account than you think you will use by the end of the year. But it is one of those unique FSAs that even if you’re taking advantage of this, you can still be someone that takes advantage of an HSA, a health savings account. Because oftentimes when you participate in a flexible spending account, you can’t do an HSA. Dependent care FSAs don’t work that way. So, if you’re someone who has to pay for child care and your employer offers this benefit, it’s a great way to save on taxes for an expense you’re going to incur anyways.

Brian: You know, I’ve already earlier gone through the child tax credit. I’m going to give you another credit and this is one back when I was in the 16 years that I was actually personally preparing taxes for clients. This one was a sleeper because if I knew somebody was working or I knew they were a full-time student and I knew they had children, the first question I’d ask them because they always overlooked this. I was like, “What were your dependent care expenses?” Because if you can tell me what your expenses are, very likely you’re going to qualify for this child and dependent care credit where we can get 50% credits up to $3,000 for one qualifying child, $6,000 for two or more. This is a powerful credit that if you’re paying for all these child care expenses so you can go work, so you can go back to school, make sure you’re taking advantage of the tax credits that are available to help you offset that.

Bo: But even if you’re not a dual income, dual working household, perhaps you have a spouse that stays at home and does not work outside the home. Another thing that you ought to be thinking about in your 30s that a lot of people don’t recognize is you can actually fund a spousal IRA. Just because your spouse doesn’t work and does not have any earned income on their own does not mean that they can’t fund an IRA. So, we have a lot of clients that even if the spouse stays home, we still want to max out Roth IRAs or we still want to fund the non-deductible traditional, do back doors. Don’t forget that non-working spouses can still have assets accumulate in their name. And at least in my experience, it’s a wonderful thing for them to get to see on the net worth statement every year to see that we’re actually putting money in accounts in their name even though they’re not working outside the house.

Brian: Another one that’s really powerful, if you have a high deductible health insurance plan, you ought to really consider the health savings account. And why we love these is because look, they get all the benefits of tax-free growth just like your Roth accounts, but they’re actually even better. They can be triple tax advantage because and what I when I say triple tax advantage, what I mean is you get a deduction on your contribution. They also grow completely tax deferred and if you use it for qualified medical expenses you get to pull the money out completely tax-free. That is unheard of that you get the deduction on the front end and you get to pull it out on the back end completely tax-free. Now I like to think for people in your 30s because remember this is by age. How do you maximize this? In your 20s you’re probably using this as a clearing account. You put the money in, you take the tax deduction, you pull it right back out to reimburse yourself. By the time you get in your 30s, you might be in the financial situation now where you can start making the contributions, taking the deduction, but then paying for the health care expenses out of pocket. And you say, well, why would you do that? Why wouldn’t I just use this as a reimbursement or clearing account? Is because we are sharing with you is that if you actually load up these health savings accounts, you can go invest those dollars, let them grow over time, and then at any point in the future, you can pay yourself back for those expenses. So these things are very powerful on maximizing what compounding growth can do for you. Still taking reimbursement years in the future as long as you’re keeping the good records. And this is something that I think I always tell people it’s a sleeper on if you’re trying to build up you know that in retirement health care expenses are going to be super expensive. It’s going to be close to multiple six figures at this point. This is a great resource that’s going to be there for you.

Bo: Now, we’ve thrown a ton of credits and deductions and accounts. If you want to know more, if you want to do a deep dive, we actually have a tax guide that we update every single year. If you go to moneyguy.com/resources, you can check out the 2026 tax guide walking through all the recent legislation changes. And it’s a quick one-stop reference. If you have a tax question, you want to know where a limit is, you want to know where credits apply, it is available for free for you out there at moneyguy.com/resources.

Your 40s – Max Out Tax-Advantaged Accounts (15:29)

Bo: All right, Brian, we’re going by age talking about how do we decrease our tax bill and beat the IRS. So, now let’s move to the 40s. This is kind of that next stage. This is sort of that fork in the road. You know, 20s was all about simplicity. 30s was about maybe being a little more intentional. Now 40s is about really doing the hard work.

Brian: If we’re just giving a short tagline, max out. I mean, that really is what you ought to be. You hopefully you’re at the point because we all know peak earning years are in those 40s and even early 50s, but it’s really in the 40s are loaded up that these are some peak earning years. You ought to be trying to really catch up and max out those tax advantage accounts.

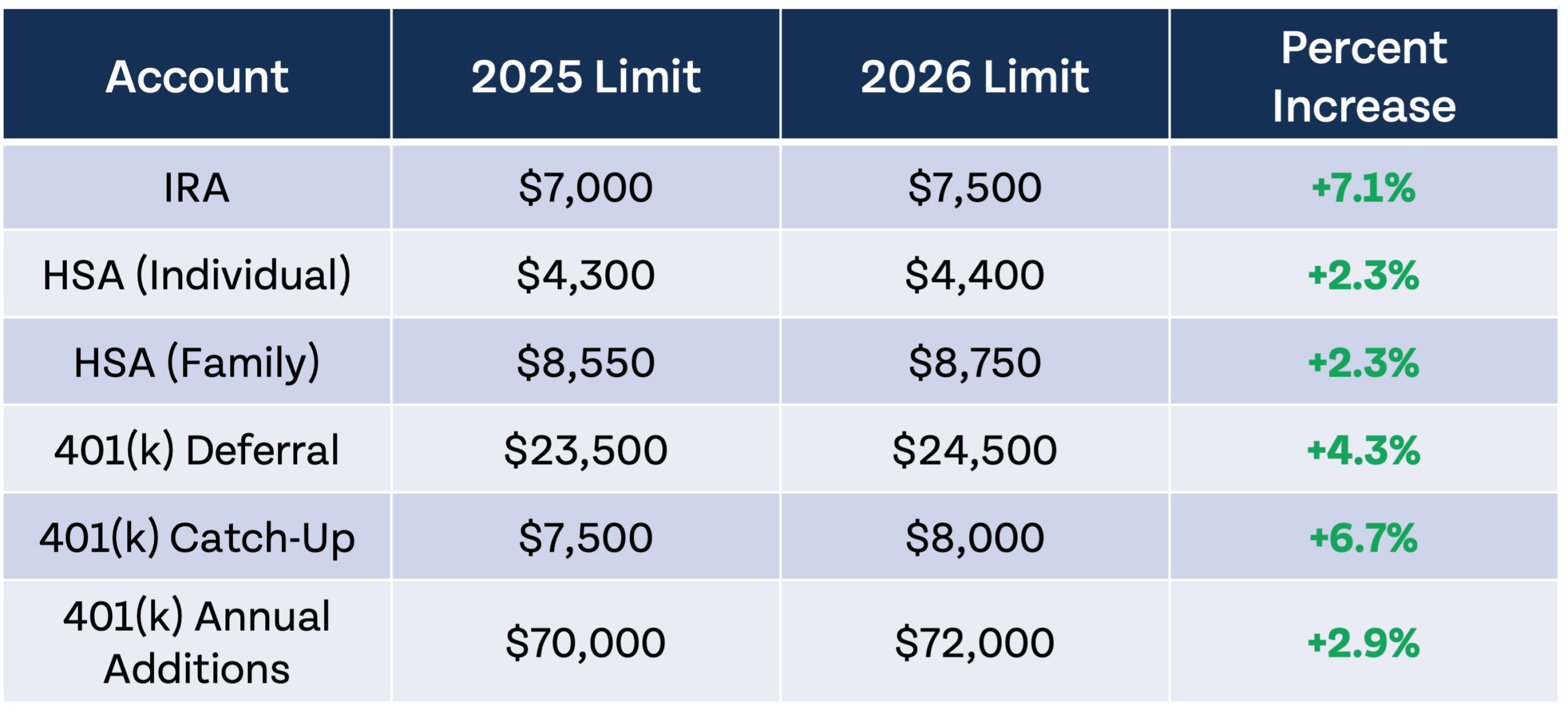

Bo: But now it can be difficult to do because when you think about the limits across all of the accounts that we have to fund at our disposal, the numbers get kind of big. Again, if we’re just thinking about 2026 numbers, if you’re participating in an employer sponsored retirement plan, like a 401k, 403b, 457, or maybe you’re a federal employee that participates in the Thrift Savings Plan, you can defer up to $24,500 of your salary. If you’re saving in an IRA, you can do $7,500. If you’re self-employed and you want to fund a SEP IRA, you can do $72,000, assuming you have income to justify that. If you participate in a simple, you can save $17,000 in 2026. Or if you’re someone who’s funding a health savings account, on the individual level, the limit is $4,400, but on the family level, it’s $8,750. You can see very quickly that some of these numbers are pretty high. And if you begin stacking some of these, in order to be able to max all these out, it does require a pretty significant income.

Brian: Yeah, this is one of those things where we want you because it’s not going to be an either or. A lot of times it can be an and because you can fund your employer plan, but you can and also fund your Roth IRA. So we like it when people stack things, but we felt like we need a case study or at least an example to show what does it look like when Manny the mutant does max out.

Bo: Yeah. So if Manny was going to max out his 401k at $24,500 and he was going to max out his Roth IRA either directly or via the back door, that’d be another $7,500. Then if he’s taking advantage of an HSA on the individual level, that’d be $4,400. That’s a total of $36,400 of tax incentivized savings that Manny could do. Well, if we just want to think about a 25% savings rate, that means that Manny would have to be making $145,000 in order to max all these out. So, even if your income is not at that level, and even if you’re not able to max out, that’s okay. It’s why we designed Brian, hold the thing for me. Still got it. It’s why we designed the financial order of operations so that you could know exactly what you should be doing with your next dollar in the most tax efficient way.

Brian: Yeah, I want to make sure people don’t get frustrated. You can still make it to steps seven and eight even if you don’t make $145,000. You just need to pay attention to your 25%. That’s what we want you to be a 25% gross income savings rate. You’re going to get beyond maxing out once you get through doing the Roth IRA contributions and you’re adding that as a percentage to seeing what your retirement is with your employer, then yes, you can actually move on to step seven and even step eight without hitting those annual contribution limits. It’s more about are you doing the 25%. What I worry about is I don’t worry about a person making $100,000 saving 25%. They’re going to be A-OK because social security is going to cover a lot of retirement and other things. What I really worry about are you financial mutants that are getting out there and maybe your income is getting closer to $200,000 and you locked it in when you were making $100,000, $120,000. You’ve got to keep going up because the further you are from the social safety net the more retirement falls on your shoulders. So you need to take advantage of what all these tax benefits and savings opportunities are so you don’t get left behind in the future.

Your 40s – Strategic Roth Conversions (19:36)

Bo: So, a lot of what we’re talking about today is how do I save taxes today? How do I save taxes this year? But this next one is less about how much you pay in tax this year and more about how much you pay in tax over the lifetime of your financial plan. Because a lot of folks in their 40s, depending on the situation they’re in, it might make sense to strategically begin converting some of your pre-tax assets, some of the assets that you accumulated in a higher tax scenario into Roth so that you can get those dollars growing tax-free for the long term.

Brian: Yeah, I already said these because it’s funny how these decades start getting married to each other because I already said peak earning years were in your 40s or 50s. Well, I also think it’s your 40s or 50s where you have the one-off life stuff or even early retirement that allows you to do these Roth conversion strategies and that’s the exact type of thing because we’re looking to have arbitrage situations with the tax code to take advantage of unique things that we spot and we had a great example of this. We did a Making a Millionaire and Bo, walk them through how did this case study work and we saved literally millions of dollars by just structuring our taxes a certain way.

Bo: Yeah. Carrie and Robert were in this wonderful situation where they were retiring a little bit early and they wanted to think about, okay, well, how should we structure our accounts and what should we be thinking about? And so we said, “Okay, based on where you guys are, we laid out here’s what we anticipate your tax situation looking like for the rest of your life.” And if you’re out there listening to the podcast, what you can see on the screen is that every year is an individual tax year. There was one year around age 62 where there was an inherited IRA that was going to pay out, but pretty much they were in a really, really, really low tax bracket until required minimum distributions started at age 75 because a lot of their assets were in pre-tax assets. They had this quote unquote tax bomb that was going to hit them later in life. They didn’t need to pull the money out, but they were being forced to pull the money out because of the way that the tax code is written. So, we said, “All right, what if instead of waiting for that tax bomb to hit, what if we started doing some strategic Roth conversions now? And what if we just said there’s a little bit of room left in the 12% tax bracket? What if we just max out the 12% tax bracket every single year via Roth conversions until we get to RMD age?” Well, by doing that, we were able to decrease in theory the total taxes they would pay over their lifetime by about $600,000. Not only did we decrease that tax bill, but by having those dollars now grow tax-free, when we look at the terminal portfolio value that they would have ended up with, it was a million and a half dollars higher than it would have been had they not begun on this Roth conversion strategy.

Brian: So, this is one I want everybody to think about your tax situation because it’s weird from a tax plan to say, “Wait a minute, I’m going to take on more income now.” That seems why would I want to accelerate my income? Well, let us explain. Look, when you’re in these low tax brackets, 12% is pretty low. I mean, if you think about where we are as a country and all the obligations and stuff, when you’re paying 12%, that’s a pretty low tax bracket. And you might be leaving just tons of money on the table, especially if you have a seven figure retirement account. You need to kind of perk up in your chair a little bit when we say look all those dollars that are 12%, you’re not maximizing. You might be leaving something in the future behind on this. And so much so that if you think 12% is great, we’ve even had clients that we said, “Well, look, 12% is definitely historically a really good low tax rate, but because we think you have such a big tax bomb.” And definitely Carrie and Robert fell into this standpoint. We’re like, you might even want to go into the next tier and actually 22%, bring that forward so that you’re not paying 35% in the future because that’s when taxes can get really expensive and we try to get proactive. But I understand it’s a delicate balance Bo and I’ll let you go through the case study some more because nobody likes to pay taxes. But we are trying to think long term and we’re beginning with the end in mind but we’re also thinking about today and there’s a delicate balance on how much taxes do you pay now versus wait for it to grow and develop into this bomb. That’s what we do as financial planners try to help you stick the landing so you don’t have regrets later.

Bo: Yeah. With Carrie and Robert, we said, “Hey, if you guys don’t just max out the 12% bracket, but if we just max out the 22% bracket up until the time that your inherited IRA pays out, by doing that, we’re going to be able to make sure that none of your RMDs later in life fall into that 32% bracket. We’re going to be able to keep everything in the 24%.” Well, when we did that, if we consider the base case of them doing nothing, we were able to decrease their cumulative lifetime tax bill by about $1.3 million. And in saving that $1.3 million in taxes and allowing those dollars to grow tax-free, they actually ended up with almost $3.5 million more at the end of their plan. Now, in reality, this is not prescriptive. This isn’t exactly the way that financial plans lay out, but this shows if you can be strategic by thinking about shifting these dollars earlier on in your financial journey, it can have huge six and seven figure impacts later on in your financial life.

Brian: I even think it goes beyond just the taxes because the taxes are a huge part of it. Another is what’s the legacy that this gets passed on to your loved ones. Believe me, a lot of you have huge seven-figure retirement accounts. You realize somebody’s going to pay the taxes on that and it’s still a blessing when you know when inheritances come, somebody’s got to pay the taxes on that and I always think about from when I’m doing legacy planning. I love Roth accounts because you know that not only are they when they pull them out tax-free, you even have the opportunity potentially to let it continue to grow for another 10 years before you have to pull the money out. If we do the right strategic tax planning, not only are we going to minimize the long-term impact on you on those required minimum distributions, but we’re also going to allow more of your beneficiaries to inherit assets that have more Roth assets. So, it’s not more of a tax bomb for them. It’s more of these are assets they’re going to be able to use for the future and for their own legacy, too.

Your 40s – Tax Loss Harvesting and Gain Acceleration (26:18)

Bo: Another thing that’s likely happened in your 40s is your accounts have gotten larger in size. And what may have not been an opportunity available to you in your 20s and 30s might begin to look attractive in your 40s. And one of those is when we have bouts of volatility when we see the market begin to have some cracks in the wall of worry and have some downturns. You might be someone at this stage of your financial journey that can take advantage of tax loss harvesting where essentially you sell a loss position. You lock in those losses. You go redeploy those dollars into a similar but not identical type investment. You maintain the same investment posture, but now you have this huge tax benefit that you get to carry on into future years.

Brian: Yeah. This is one of those find the silver lining in a bad situation, Bo. Whenever there’s volatile periods, we’re definitely turning lemons into that lemonade. That can help you from a tax planning standpoint. And on the other side of the coin, because that was consider tax loss harvesting. Another one we like to talk about is accelerate your gains. And you’re like, wait a minute, you guys are telling me there’s actually some benefits to taking gains before I need the money. We’re saying absolutely. Our tax policy has some unique quirks in it is that y’all realize that there’s actually if your income’s below a certain threshold, there’s actually what’s called a 0% capital gains tax. That’s right. If you can go ahead and if your income is below for married couples, I believe it’s right around $97,000, you can take you don’t pay taxes on your capital gains. So, you can imagine if you’re one of these people that you leave the workforce early or you have a year that maybe you’re unemployed or your spouse has stayed home with the kids and you look at your income, you go, “Holy cow, we qualify for this 0% capital gains.” You should not sleep on that. We could reset your basis higher by going ahead and taking advantage of this quirk of the tax code.

Bo: Yeah. If we think about this in a practical case study sense again, let’s take Manny the mutant. Let’s say that Manny had a $20,000 investment that had performed really well and now it’s turned into $50,000 and Manny’s starting to figure out, okay, what’s the right time? How do I think about divesting out of this position? Well, let’s say that something happens, job change, single income household, and he is in a situation where the taxable income for his household is $65,000. He could then sell this entire position, recognize that $30,000 capital gain and it’s still going to fall inside that 0% capital gains rate. Meaning the tax due on the sale of this holding is going to be zero. But if however he were to wait and maybe he goes to a two-income household or he changes jobs or he has some other income source kick in and the taxable income now goes to $100,000 and he decides he wants to then sell this investment. Well, now all $30,000 of that long-term capital gain is subject to the 15% capital gains tax rate, where he could have sold it a year before and paid no taxes, this year he has to pay $4,500 in taxes. The timing of when you sell your investments and when you take advantage of these unique opportunities can have thousands, if not tens of thousands of dollars of savings available to you.

Brian: So you can start to see the quirks of the tax code is because this isn’t something you want to find out when you go get your taxes and go, man, I could have done more. This is why you need to be proactive. And this is the part where I always say life gets complicated as you start figuring out how do I actually get access to all this money I’ve been building up in the background. That’s where we kind of come in and help people navigate these situations. So that Bo that wraps up the 40s.

Bo: One other thing I just want to throw in this because we get this question all the time. What if I don’t want to sell the investment? What if I don’t want to get rid of it? One of the things this is why it makes sense. You hear all the time we talk about loss harvesting. There’s the idea called the wash rule. I can’t sell something at a loss and then go buy it back. That does not apply to gains. So, one of the things you can do is even if Manny were to sell this holding, he could go back today and buy the exact same holding at $50,000, resetting his cost basis for the future. So, this isn’t just something that you should consider, you should think about. If you are in a low income tax year, it makes sense to review every position in your portfolio to see if this is something you could take advantage of because there’s a really good chance that your future self will thank you for that planning opportunity.

Brian: Yeah, what a great planning opportunity that creates.

Your 50s and Beyond – Charitable Giving and Catch-Up Contributions (30:47)

Bo: All right, Brian. Now, let’s talk about the next stage. We talked about 20s, 30s, 40s. Let’s talk about the 50s and how do we go about beating the IRS in our 50s?

Brian: Well, this is one of those things where, you know, hopefully at this point you’re getting to the stage where yes, you’re going to have money for financial independence, but you’re also thinking more of legacy of what are there organizations I want to support? And the first thing we know that being charitable is definitely rewarding and we want you to be generous. So, bunching charitable contributions is the first thing you can consider. Remember how earlier I said that the majority of Americans are taking standard deductions? Well, that’s because if you add up the deductions for most people, they just don’t add up to enough to do itemized deductions. Well, if you’re charitably minded, there’s a good chance that maybe you can bunch your charitable contributions, cross into that itemized in a key year, and then spread out how you give to those charities in the future. There’s nothing wrong with you taking advantage of that.

Bo: A great tool that you can use if you’re bunching or maybe you’re not bunching, you’re just giving annually, you can think about using a donor advised fund where not only can you use it as a mechanism to bunch your contributions where okay, I’m going to put $25,000 into the charitable gift fund this year and get the deduction, but I’m going to give $5,000 to an organization each of the next five years, but I can also now gift highly appreciated securities. Maybe I have that $20,000 investment that turned into $50,000 and rather than having to sell it and recognize that capital gain, I can just donate that to my charitable giving account, get the full tax deduction on the full market value of that holding and all those capital gains disappear forever.

Brian: Earlier I was talking about always look for those silver lining moments where you turn a negative into a positive or lemons into lemonade. This next one is definitely one of those is take advantage of catch-up contributions. Look, it stinks. I’m in this. Once you get to a certain age, you’re like, man, I’m getting old. I wish the birthdays would quit coming. But when you cross into 50, you at least now the government says, hey, you’re old enough that you’re probably thinking about retirement. So, you’re thinking about it enough that you’re even having regrets that I should have saved even more in the past. The government gives you that opportunity by giving you access to additional catch-up contributions.

Bo: Yeah. And it depends on the account and even unique to this year depends on your age. If you’re in a 401k, 403b, 457, the catch-up amount for those over 50 in 2026 is $8,000. But there’s even a super catch-up for those that are aged 60 to 63, which is $11,250. For a simple 401k, the catch-up is $4,000. The super catch-up is $5,250. And then if you’re someone contributing to an IRA and you’re over 50, in addition to the normal contribution you can do, you can do a catch-up of $1,100 and if you’re participating in an HSA and you’re over the age of 55, you can do $1,000 as a catch-up contribution to a health savings account.

Your 50s and Beyond – Optimizing Retirement Withdrawals (33:49)

Brian: All right, we’re talking about 50s and beyond. This is also the culmination where people actually you’re transitioning from saver to now consumer, starting to spend down your resources. You’ve got to optimize your retirement withdrawal strategy. You know, throughout this entire show, we’ve walked through the three buckets. We’ve walked through all the different ways you need to fund your retirement. This is the moment where it really kind of this is game time. It’s probably the biggest thing is because now if you can pull in the right optimized strategy, it really is that choose your own adventure where you get to in a creative very legal way kind of work through how much in taxes you will pay and how much of a headwind it’s going to be on your retirement.

Bo: Yeah, we have the financial order of operations and it’s a great mechanism for helping you figure out how do I accumulate, how do I build, how do I save super efficiently. Well, we also get asked all the time, guys, why don’t you do a financial order of operations for withdrawal, for distribution, and that’s because it gets so nuanced and it’s so specific and it is not a one-size-fits-all. When you retire, when you get to financial independence, when you start living off of your assets, the way that you do it is going to be very unique to your situation, your risk tolerance, your time horizon, your account structure, your goals. You want to make sure that you think through it well because the decisions you make early on in retirement can have huge implications later on.

Brian: Well, let me just go ahead and throw out some terms that you start hearing a lot. Required minimum distributions if you’re charitably minded, qualified charitable distributions, QCDs. There’s also IRMAA if you’re thinking about Medicare. If you think about the taxability of your Social Security, do you see how all this stuff kind of starts coming to a head? And that’s why I always tell people, look, this is why we can love on you, give you all the free advice in the world, and even tell you, go to moneyguy.com/resources. We’re going to accelerate your path to creating success. And we really don’t ask anything of you. Matter of fact, we have some big plans that we’re even going to turn some things that are behind pay walls, turn those even into free resources for you soon. More to come on that. But a lot of this, no matter how much we love on you and give you, you’re going to see the fruit of our system is the success which leads to the complication. And as I think you could hear on doing an entire show on taxes by age, you guys represent and you resemble a lot of these things. And you’re probably saying, look, I don’t know what I don’t know. I don’t know where my blind spots are. I’ve only got one retirement. I wish I had somebody who’s done this hundreds if not thousands of times. That’s where we’ll leave the porch light on for you. We’d love for you to consider becoming a client. Let us help you live your best financial life. Exactly what Bo said. We have a financial order of operations to help you through all those things as you’re building assets. There’s not one for retirement because everybody is so personalized. We had a studio tour just come through and they were asking about a specific financial product and I was like, the reason I’ve never done content on that is because there’s just too many variables that I have to see your taxes, I have to see your age, I have to see your risk profile. I couldn’t do a good job with doing that, but I can do that for specific clients. And we will write that plan for you. We will make sure it represents and let you live your best life because money is nothing more than a tool. We just want to make sure that we maximize that very important element so you live your best life. I’m your host Brian joined by Mr. Bo. Money Guy team out.

Free Resources

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

Articles

The Best Tools for Filing Your Taxes in 2026

Have you filed your taxes yet? You still have ample time left until the April 15th deadline, but it’s probably best not to procrastinate too...

Articles

6 Financial Changes To Make in 2026

There is no need to wait until an arbitrary date on a calendar to make positive changes in your financial life, but if you are...

Articles

The IRS Just Announced 2026 Tax Changes!

Each year, the IRS adjusts retirement account contribution limits, standard deductions, marginal tax rate brackets, and more for inflation. I’m happy to announce that it...

Financial FAQs

Courses & Tools

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Recent Episodes

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

We Changed The 4% Rule!?

Retirement planning isn't as simple as following the classic 4% rule anymore. In this Live Q&A, we explain why the traditional retirement withdrawal strategy deserves...

Episodes

Is Aggressive Saving Derailing Their Short Term Goals?

High earners in their mid-twenties, cash poor, and a wedding 12 months away. In this episode of Making a Millionaire, we show Joey and Leah...

Episodes

Why This Money Advice Has EXPIRED

Traditional financial advice isn't always wrong, but some money rules simply haven't kept up with today's economy. In this episode, we reveal which classic money...