-

▼

-

▼

This one mistake is keeping you poor! Looking rich may be a trap. We break down the stats and show how making these “small” mistakes could be really hurting your retirement!

Enjoy the Show?

Where You Can Watch and Listen:

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

- Episodes of The Money Guy Show every Friday

- Episodes of Making a Millionaire every other Monday

- Mini-shows every Wednesday

- Ask Money Guy Livestreams every Tuesday

- Tons of other fun content!

While looking rich is keeping you from being wealthy, I am excited about this because I feel like this is a problem that exists and permeates through all of society right now. We care so much about the way we look and how others perceive us that it is leading us to likely make some sub-optimal financial decisions.

Yeah, I remember when at first there was “The Millionaire Next Door” and then Dr. Stanley, of course, wrote “Stop Acting Rich.” It was one of those things where you realize the actual behaviors of successful people are not what we’ve been led to believe. And that goes for consumption as well. A lot of us in this world, where we have social media and the gram, are being told the way things are, but it’s not always what it seems.

That’s right. We are sucked into this idea that we need to look a certain way, buy luxury brands, and be luxury consumers so that others can see how well we’re doing. We want to show off how successful and awesome our life is on social media. When we say luxury, we’re talking about brands like Louis Vuitton, Rolex, Dior, Chanel, Tiffany, and others that are often advertised in fancy magazines or golf magazines.

This was brought to my attention when we did a show years ago about Rolex purchasers. It’s interesting when people repost some of our content. We pulled the stats, and it still holds true. Imagine our surprise when we researched who actually wears Rolex watches. It was unbelievable. We found that 74% of Rolex owners make less than $120,000 a year. Now, don’t misunderstand; $120,000 is a significant income. But this stat says that three-quarters of the people who wear those watches actually make less than that. And these watches are pretty expensive; they’re not inexpensive. A basic Datejust is probably north of $5,000, if not even $5,000 to $7,000 with the post-COVID inflation and everything else. But the higher-end models can be tens of thousands or even thirty thousand dollars, depending on the features.

Now, let’s take into account that 27% of regular luxury consumers have a household income of less than $50,000. We’re talking about luxury goods here, not the base brands. These are people who have incomes lower than $50,000. You wouldn’t think they need to buy the generic brand; they should go and buy the luxury brand. There’s a disconnect there; something is not adding up because those should not be the people who are purchasing these brands. At least that’s probably not the best use of their dollars.

When we talk about building wealth with $50,000 or less, a lot of people argue that they can barely survive on that income. Yet somehow, over a quarter of these people still feel that they should be buying luxury goods. That is not the path to building financial independence. And this is not a trend that is getting better. When we did the research, we found out that those who earn less than $40,000 have seen a 365% increase in their spending on luxury goods since 2020. That’s worth repeating. Since COVID and the economic downturn, folks making less than $40,000 a year are increasing their consumption of luxury goods by 365%. You would have thought that during the reset and the COVID crisis, savings rates in America would have increased because people couldn’t go out and spend money. But now, as we have started spending money again, we are falling into the same traps we were falling into before. We are buying things that are perhaps more expensive than we should be buying.

The research even went a little deeper and shared that the average luxury purchase is around $520 per year. So that got us thinking. What could that $520 turn into if a consumer made that decision once every year starting at age 18? By the time they reached retirement age (65), it could grow to almost $615,000. So, by making one luxury purchase every year instead of investing those dollars, you could be walking away from over $600,000 of retirement savings. That is real money that you are sacrificing.

I have to believe that the 18-year-old who buys the $700 Givenchy fanny pack probably won’t be wearing that same fanny pack at 65. They will likely be embarrassed about it later, just like the parachute pants or Z Cavaricci pants of my generation.

The resurgence of fanny packs can be 100% attributed to trends. It is interesting that whenever you shop online, every product seems to offer a buy now, pay later option. 45% of buy now, pay later customers use it to make purchases they can’t afford. Meaning, if they had to pay in cash or all upfront, they wouldn’t buy those things. But if they can make six monthly payments of $19.99, suddenly it becomes more affordable. That is not the way you want to make financial decisions because you won’t get ahead on your financial journey if you’re just figuring out how to get by one purchase or one month at a time.

It is essential to educate yourself and understand the financial order of operations. We’re not against splurging on yourself, but there’s a proper time for it. The financial order of operations guides you through wealth-building steps like taking advantage of free money from your employer, maximizing tax-free growth opportunities, and prioritizing retirement contributions. Buying luxury goods falls more into step eight. So make sure you don’t skip the other steps on your wealth-building journey. Check out our Financial Order of Operations course to know exactly what to do with your next dollar.

Remember, being wealthy is way cooler than looking wealthy. When you can afford the things you buy without sacrificing other areas, you’ll be much happier and fulfilled. Educating yourself is one of the best things you can do to impact your financial life. That’s why you are here right now at moneyguy.com, seeking resources and knowledge. Go to moneyguy.com/resources for a deep dive into our free resources.

Free Resources

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

Articles

Are Index Funds Still Better Than Active Funds in 2025?

Over longer periods of time, index funds tend to outperform actively managed funds in most categories. Recently, total assets in index funds have surpassed the...

Articles

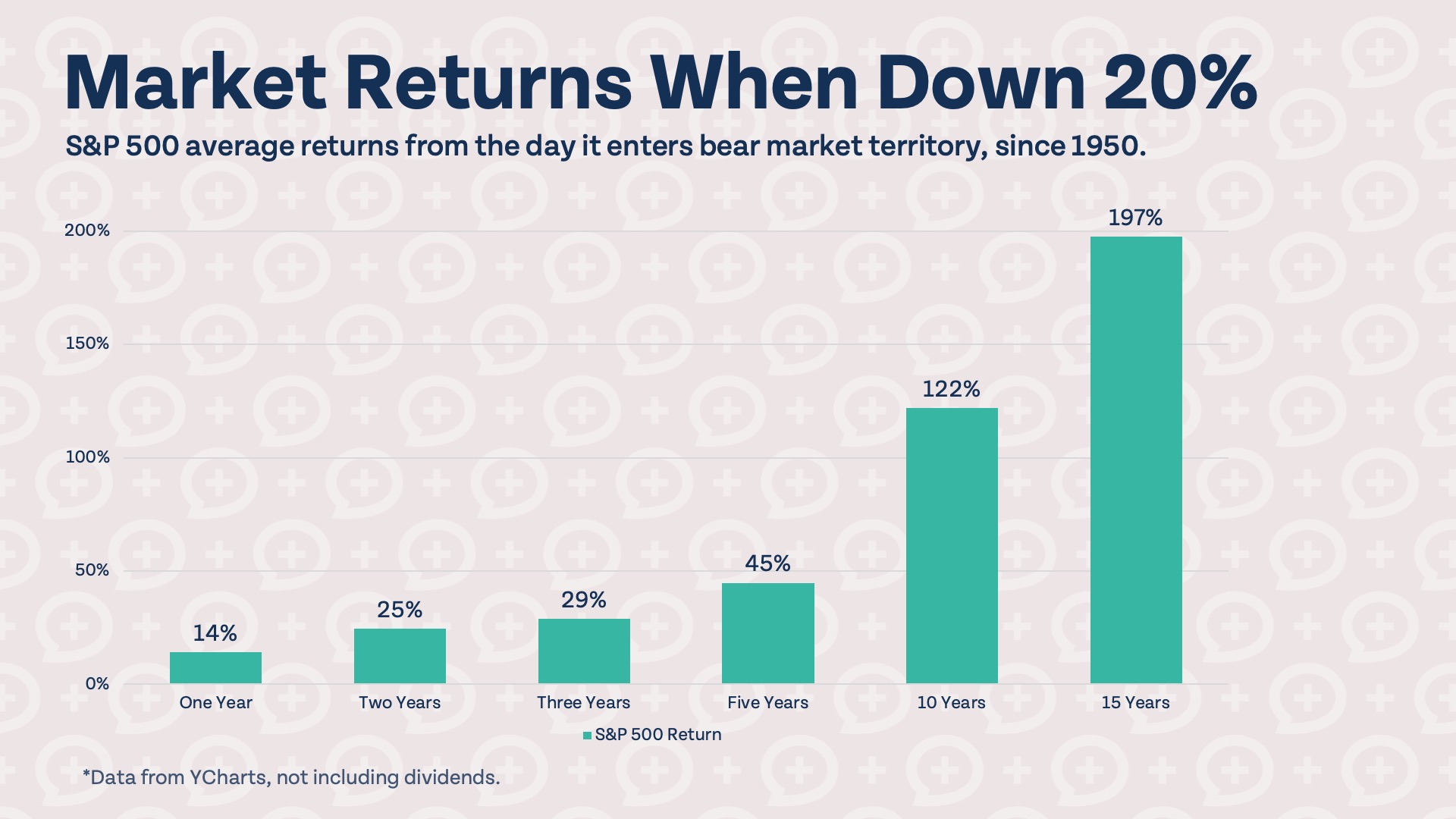

What To Do When the Stock Market Is Down

The S&P 500 is down nearly 15% from its highs earlier this year, inching closer to bear market territory. While it may not be wise...

Articles

How To Prepare for a Bear Market in 2025

The Nasdaq stock market index is in correction territory, down over 10% from recent highs. The other major US indexes, the S&P 500 and Dow,...

Financial FAQs

Courses & Tools

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Recent Episodes

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

Why This Money Advice Has EXPIRED

Traditional financial advice isn't always wrong, but some money rules simply haven't kept up with today's economy. In this episode, we reveal which classic money...

Episodes

S&P 500 vs Charizard: Which Investment Wins?

Are Pokémon cards and index funds better than the S&P 500? Brian separates the hype from reality on today's hottest collectible investments and reveals what...

Episodes

Quit Saving Money? The CoastFIRE Epidemic

CoastFIRE is exploding in popularity, but are you coasting too soon? In this Live Q&A, we break down the real numbers behind CoastFIRE, share the...