-

▼

-

▼

How do you build wealth when the average American is broke? In this episode, we do a case study comparing Average Allen (doing what typical Americans do) against Manny (following Money Guy rules) across four financial decisions to discover who builds wealth or stays broke, and the math is brutal. These aren’t unique decisions for unique people. We all face them. But if you can think differently than the average American and go against the grain, you can have a financial future that doesn’t look like the world around you.

Watch the full episode to see the complete breakdown of all four decisions, discover which mistake costs the most, and learn why time is your most valuable wealth-building asset for your financial roadmap. For more tools and resources, visit moneyguy.com/resources.

Enjoy the Show?

Where You Can Watch and Listen:

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

- Episodes of The Money Guy Show every Friday

- Episodes of Making a Millionaire every other Monday

- Mini-shows every Wednesday

- Ask Money Guy Livestreams every Tuesday

- Tons of other fun content!

Introduction – Four Decisions That Determine Wealth (0:00)

Brian: Here’s the thing. Getting rich, everyone wants it, but the gates are narrow and only a few make it. If you want to be part of the wealthy crowd, you need to hear today’s show.

Bo: Brian, I am so excited because while we know that many people don’t end up actually building significant wealth, we can actually pinpoint some of the reasons why that’s the case and hopefully after today help lead you down a very different path.

Brian: Now, you guys know we’re financial advisors here to put the math behind the mistakes. And with that, let’s jump right in.

Bo: Brian, we call our community financial mutants for a reason because they tend, at least when it comes to financial matters, they go against the grain and they live life from a financial aspect a little bit differently.

Brian: I mean, if I could just get anybody out there who’s brand new to our content to understand that small decisions can create dramatic or life-changing results. And that’s really what I hope that we can cover on today’s show is we’re going to change people’s lives with this.

Bo: And what I think is what we recognize is that these small decisions and sometimes even these large decisions, they stack up over time. And when you stack decisions both on the good side and the bad side, they can both compound. So on today’s show, we’re going to do a case study across two different types of people. We’re going to look at Average Allen, which is a representation of the way that most Americans make their financial decisions. And then we’re going to contrast that with our favorite financial mutant, Manny the Mutant. And you’re going to be amazed at how a few small decisions can have a huge impact in each of their financial lives.

Brian: Look, I’m old enough. I’m not the before picture. I’m the after. And what I think is interesting is I look back at my own life and I think about a group of my peers where we all came out of school making about the same amount of money. But I’m telling you, it is these things we’re covering today that when I look back and if you want to know where people’s book of regrets are on things that they wish that they could have over, it is going to be these four topics.

Bo: Yeah. I think when we think about common decisions that people make, these are the ones we’re going to outline today. We’re going to outline savings rate, buying a car, buying a home, and then maybe the most devastating of all that we see the most often, waiting to invest, assuming that you can always do it in the future. And I think you’re going to be amazed when we compare these two different individuals how different their lives look at the end of their financial journey.

Decision #1 – Savings Rate (2:31)

Bo: So, Brian, with that, let’s dive right into the very first one. The first decision that most people face when they begin earning some sort of money, some sort of paycheck, is okay, what am I going to do with it? How am I going to save it? And what’s my savings rate going to be?

Brian: Well, first let’s get some context. What is the typical American doing? I mean, when we pull the research from the Bureau of Economic Analysis, the average American has a savings rate around 4.6%. Kind of abysmal. Compare and contrast that to what we say financial mutants should be doing.

Bo: Yeah. We say that we want you to aspire to saving 25% of your gross income. So 4.6% is far off from 25%. A lot of people ask, okay, well guys, did you just kind of like pull that number out of thin air? How did you come up with that? No, we actually put the math behind it. And there’s a reason why we want you saving 25% of your gross.

Brian: I mean, when you look at this slide, look, if you’re blessed and you found our content and you’re in your late teens or early 20s, you can actually see a little really does go a long way. You can save as little as 10% savings rate and it’s going to create dramatic results. But unfortunately, we know from the stats, the typical American does not discover the great wonderful world of finance until their mid-30s. And that’s voila, the intersection point of where 25% comes from. But I want you to notice when you go to moneyguy.com/resources and look at this and download this for yourself, you’re going to notice none of them have 5%. So Americans are missing the mark completely even when you look at what the stats say you should be saving.

Bo: So let’s talk about okay, how significant of a deal is this? How big of an impact can this have in the lives of real people? So let’s look at our two individuals today. Let’s look at Average Allen and Manny the Mutant. Let’s go ahead and assume that they both make the exact same income. We’re looking at the median household income right now in this country of $83,730. And what we’re going to assume is that Allen is going to have the average American savings rate of 4.6% of his gross income, which is going to be about $321 a month. However, Manny knows I need to be saving 25% of my gross income. So Manny’s going to save 25% and that comes out to $1,744 a month. Now Brian, we assumed no pay raises, no significant changes in financial life. How does it stack up if one saves 4.6% starting at age 30 and the other saves 25% starting at age 30?

Brian: And the numbers were mind-blowing. Well, and I think this is look, I want to give us credit on trying to be somewhat conservative. We know that saving and investing 25% of your gross income, that is so aspirational. We didn’t even start this in the 20s. We could have really blown this out of the water even more if we’d have done this Allen versus Manny in the 20s. But we said, “No, let’s go ahead and punt.” This is from age 30 to age 65. But guys, look at this. Manny ends up with close to it is over $4 million. Meanwhile, average Allen doing what typical Americans, by the way, typical Americans don’t even end up with the $736,000. So, even this falls apart. The average American is not even doing this consistently.

Bo: Now, you said something right there, Brian. You said 25% is aspirational. And you may be sitting out there listening right now saying, “Guys, it’s just unrealistic. Housing is expensive. Groceries are expensive. Life is expensive. I can’t do 25% right now.” And that’s okay. What we would encourage you to think about is what can I do tomorrow that’s better than today? Maybe I can’t go from 4.6% all the way to 25%. But maybe I can go from 4.6% to 5.6% then from 5.6% to 6.6% because you would be amazed at how much just a little bit extra can do. And if you don’t believe us, go out to moneyguy.com/resources and check out our deliverable that shows what 1% more can do for you. And what we’ve laid out is at every age, how much of your retirement income can you replace just by increasing your current savings rate by 1%. If you’re early, if you’re young, if you have a lot of time on your side, small adjustments now can have huge impacts later on in life, but you got to start today.

Brian: So, don’t sleep on what 1% more can do. But I also think if you get a pay raise this year, how about giving us 60%? Put 60% more towards your savings and investment of that new pay raise. And I think you’ll be shocked if you just consistently every time you get a pay raise start stacking more and more of the money working for you. You will end up in a much better place. It is really the culmination of those small decisions building on top of each other.

Decision #2 – Buying a Car (7:28)

Bo: All right, Brian, let’s talk about the second decision that a lot of Americans face and frankly a lot of Americans get really wrong. And I’ve heard you refer to this before. You say that this is literally napalm for your personal finances and this is buying a car.

Brian: Yeah. If you’re trying to blow up your finances, do this mistake. And this is one, you know, when I wrote Millionaire Mission and I’m having a chance to make some updates right now on some things. More to come on that. But this is the section I’m trying to really tighten up even more because I want people to know this is the biggest mistake I see. I have so many people in my life as they come out of college, the first mistake they make is they go buy too nice of a car and I don’t literally want to see you driving around your wealth because when you get to retirement age or the ages you want to start working less with your back, your hands and your brains. This is the biggest mistake. I was about to say decision, but it’s not a decision. Biggest mistake I see people make.

Bo: Now, don’t mishear us. We’re going to talk about what it looks like to buy a car, but I think we had to level set because sometimes we get a bad rap on this. We love paying cash for cars and we think that realistically if that’s an option for you, it’s most likely the best option to take. However, a lot of people just can’t do that. We need a responsible automobile to be able to get us to our job so that we can create the income that allows us to build for our future. And so oftentimes we’re not able to pay in cash. But if you can pay in cash, we love that. Don’t mishear us. And so every year, Brian, we do an annual survey where we ask our clients, “Hey, what do you do? How do you buy cars?” And what’s really, really interesting is when we look at our millionaires, only 40% of them finance their current car, the car that they’re buying right now. Only 40% finance. That means 60% end up paying cash. But I feel like that only tells part of the story.

Brian: Oh, yeah. Definitely. Cash is king on car purchases. That’s what financial mutants do once they’re established. But if we pivot the question and say, “Hey, yeah, that’s fine, but we have to meet people where they are.” And we know we have a lot of people who come to the Money Guy show who are brand new, freshly minted financial mutants or aspiring financial mutants. What do you do when your biggest wealth creation tool is actually going to your J-O-B? You need to have reliable transportation. So, your first car out, more than likely, you need a bridge that will allow you to have responsible, reasonable, and reliable transportation. And we found out when we asked our own millionaires, their first car that they ever purchased for themselves, 72% of them financed it. I resemble this. Bo resembles this. We want to make sure we compare and contrast what millionaires do once they’re successful, but also what did they do at the beginning of their journey.

Bo: And so if these are millionaires that obviously had to finance at the beginning part of their journey, but now are able to pay cash, there must have been a right way to do it, a responsible way to finance an automobile. We believe that if you have to borrow, there is a right way to do it. And that’s how we came up with our 20/3/8 car buying rule. Whether you’re buying a new car or a used car, we want you to put 20% down. We want you to finance no longer than 3 years or 36 months. And your total car payment cannot exceed 8% of your monthly gross income, 20/3/8. Now, there are two small caveats. Do not buy a luxury car with 20/3/8. If you’re buying one of the luxury brands, we want you to pay cash for that or at least have it paid off inside of a year. And as a litmus test to whether you’re making good decisions, we never want your car payment on a monthly basis to be more than the amount that you are saving for the future. If you are saving less than your car payment, there’s a good chance that you’re doing it wrong.

Brian: Well, it’s easy because we’re about to compare and contrast this to what the average American does. But here’s guys, the why is very simple. We know cars depreciate like a rock when you buy them. So that’s why we give you let’s get ahead of this, put a 20% down payment. We know a lot of people what dealerships are doing to people in the auto industry is that they’re saying, “Hey, you can finance anything at a few hundred a month if we just expand out the amortization of how long you can pay for this.” So, we keep your eyes and your wallet and your purse in check by making sure you don’t finance this for longer than 3 years because then that will make you be very honest with what your car payments can be. And then we wanted to put some guard rails of well, how much is too much? So that’s why we said, “Okay, let’s do 8% of your gross monthly income.” There’s a lot of things vying for your monthly cash flow that’s coming in and out. Let’s try to give you some guard rails so this doesn’t get out ahead of itself. Now you’ve heard the why. You’ve heard the context. Bo, share with them what the average American unfortunately is doing.

Bo: Yeah. When we look at the average American buying a car right now, we know that right now the average car payment for a newly purchased car is $772. If we just stop there for a moment and think, okay, well, $772 and the car payment can’t be more than 8% of my monthly gross income. That means you would have to have an income of almost $116,000 for a $772 car payment to make sense. And we know that the average American does not make $116,000. So, right out of the gate, we’ve kind of blown it up. Well, we continue going down. The average loan term right now almost 70 months. It’s like twice what we said. Literally twice.

Brian: People literally are not buying cars they can afford. The only way they can afford them is to pay for them for literally forever. And you realize guys, the thing that while we’re bringing all this to light, we’re going to do a compare and contrast of what the opportunity cost is. But your time is the most valuable thing. You’re going to see a consistent trend here. And to see that you’ve now delayed this by almost double is horrible. And then you think about the fact that interest rates are as high as 7% right now. The loan amounts are up to $44,000. You can see how this thing literally, as I said earlier, you are driving your wealth instead of actually building that wealth so you don’t have to work so hard.

Bo: All right. So now let’s see. Okay. What if we stack up Average Allen versus Manny the Mutant? How does this compare? Well, if we assume that Average Allen is going to do what the average American does, he’s going to go out and finance a new car for $43,759. But Manny the Mutant is going to be a little more responsible. He’s going to go out and buy a used car and he’s going to follow 20/3/8. Allen is going to have a 69-month loan term, and he’s going to have a payment of $772 a month. Manny, on the other hand, is only going to have a 36-month loan term. And because he bought a less expensive car, his monthly payment is only going to be $554 a month, which means right off the bat, he’s able to invest $218 a month that Allen is having to put towards his automobile. When you look at Allen’s additional margin for saving and investing, he has none. All of his money is going towards his monthly car payment. But Manny, after he pays off his car in 36 months, now he can invest the entire $772 a month. So you think about these two individuals over 69 months, they have the exact same capital outlay. They’re both spending or consuming $772 a month, but they are putting them in very, very different places. So when we stack them up, Brian, after 69 months, they both have a paid-off car. Check. Excellent. However, because Manny was able to begin saving and investing and he was able to get that car paid off after this 69 months, Manny has been able to accumulate $42,500 in addition to having a paid-off car. Allen has to show for his $772 a month is just a paid-off car, no additional assets.

Brian: What I think is interesting is that I think about my younger years, without a doubt, nobody was ever asking to go ride around in my car like when you’re all going out to eat or doing something. So you do hope that you have a friend who’s making the Average Allen mistakes because they sure do look cool and it’s nice to ride in those cars when you go out as a group. But I think the point I have is that we’re going to show you just like this shows right here is that Manny at the end of this term of 69 months, he not only, yes, he’s driving around in a car that’s not as cool, but he’s got $43,000 in his army of dollar bills. Now, you’re like, “Okay, well, $43,000. How does that change your life in the long term?” Well, here’s what we did. We actually if we grew this because it’s not just that period of time that you’re driving the car. It’s the opportunity cost of what that $43,000 could become with 30 years of growth or 35 years of growth. It’s close to $700,000. And a lot of you are like, okay, well, but maybe I’m willing to pay a $700,000 premium to be cool and fabulous in my 20s or early 30s. But I want to remind everybody, we’ve done research on this and it’s back to behaviors of what people who actually have money, who are building wealth versus those who just want to look rich. And we found that in our own surveys of ownership, 84% of our millionaire clients are driving their cars for seven plus years.

Bo: I love that. Check the box.

Brian: So, compare and contrast that to, we found this from, I believe it was from Yahoo Finance, 65% of Americans drive their cars for 5 years or less. So this is not a $700,000 once-in-a-lifetime mistake. This is a twice a decade disaster that the average American’s doing. So if you look at it in those terms, this isn’t $700,000 of opportunity. This is multi-millions of mistakes that people are making. And do you see why when I if I could get in the room with a bunch of 20-somethings who are freshly minted and ready to start jumping on their career and start saving for the future. Don’t go buy a fancy car. That is a disaster. The only people who are going to smile are the people at the dealership and the auto manufacturers and the banks. All of those people are going to be smiling. You’re going to be the one who’s sad at the end of the road.

Decision #3 – Buying a Home (17:53)

Bo: So obviously buying a car is a very expensive decision that can have huge implications down the road. But there’s actually another decision that we see people making. And for most people, this is the single largest financial decision that you will ever make in your lifetime. And so as you can imagine, the single largest decision you might make could have the largest impact to your financial life. And that’s buying a home.

Brian: Yeah. I mean, once again, this is showing it’s not the latte effect. I mean, that’s important. I want you budgeting. I want you being good with money, but man oh man, do you have to watch these big life decisions. And a lot of you, if you hang out with us, we’re going to give you some rules on how to do house ownership or rent very well. But if you just get some level set of what’s the context of what the typical American’s doing so we can know what average is. You can see the average American ownership is putting them at 33.5% of their income is going towards housing in their mortgage.

Bo: Yeah. You can imagine if one-third of your income is going towards housing that doesn’t leave a whole lot of room for other stuff like living life today and enjoying the present and saving for the future and building wealth. And a lot of folks fall into this trap. And again, we think when it comes to making these consumption decisions, there’s a better way to do it. That’s why we came up with our 3/5/25 rule, which says if you’re buying your very first home, you don’t have to put down 20%. We’re okay if you only make a 3 to 5% down payment. But before you buy that home, we want you to make sure that you believe that you will be in this house for at least 5 years. Homes should be long-term decisions, not short-term decisions. And when you look at your total mortgage payment, when you add up the costs that go into the housing, we want your total mortgage payment to be less than 25% of your gross income. So that’s the rule. And yet, we know that most Americans are spending 33% of their income on their housing. That’s 8% that’s not going towards other financial goals like building towards financial independence. You can see when you do this, when you put yourself in this position, especially if it’s a 30-year mortgage, that’s an additional 8% for 30 years that you’re not going to be saving otherwise, it puts you in a very precarious position.

Brian: Well, a lot of you are probably starting to catch on. Look, we’re giving you some boundaries. Once again, when car buying, we’re talking about 8%. With house buying, we’re talking about 25%. It’s because we’re trying to make sure you still keep some margin in your life, not only for living your life, but also for saving for the future. That whole concept of deferred gratification. If you go out there and just let the market or the consumption society we live in have its way with you, you will spend every dollar that comes into your household and you’ll be miserable. Now, yes, you might be driving a nice car. You’re going to be that commercial that we all remember, at least I do, from my childhood, of a guy who’s on the riding lawnmower in the front yard going, “Don’t you like my house? Don’t you like my car? I’m in debt up to my eyeballs.” That’s not the better way to do money. That’s the way. Like I said, book of regrets. This is the way. If you just go with what society tells you is going to be okay, you will have periods of looking back and going, “What have I done with all this opportunity that I could have been building wealth?”

Bo: So, if you want to do this right, if you’re looking for a tool to help you, you’ve decided, okay, it is time for me to buy a house. I’m at that stage, it makes sense. We have a tool out at moneyguy.com/resources. It’s our home buying calculator where you can put in this is my income. This is how much I have for a down payment. This is the interest rate that I can get. Here’s how long I’m going to borrow for. It will actually help you figure out, okay, how much home can I afford? If you use this tool, it’ll prevent you from being in that spot where you are house rich but life poor. So again, let’s look at how this might look different across two different individuals. Let’s go back to Allen and Manny, Brian. Let’s assume that Average Allen is going to put 3% down on a $415,000 home. Manny, on the other hand, goes out to moneyguy.com/resources, uses the home buying calculator, and he recognizes that he can buy a $332,000 home, and he’s going to put 3% down on that home. Because of Allen’s outstanding mortgage, he’s going to have a mortgage of $2,783, which is 33.4% of his income. Let’s just assume that both Manny and Allen have a $100,000 household income. So Allen is putting 33.4% of his income towards the mortgage. Manny, on the other hand, follows the Money Guy rule. He’s only putting 25% towards his mortgage, and that’s a mortgage payment of $2,083 a month. Allen, because all of his money is going towards his mortgage, he has no additional to save, no margin for building for the future. Manny, on the other hand, has an extra $700 that he can be saving every single month. Now, I can already hear people out there saying.

Brian: The trolls are crawling out from underneath the bridge.

Bo: This is real estate. Allen bought the more expensive home, and that’s leverage, and it’s going to make money. If the more expensive home goes up in value, it’s going to be better off. So, we said, “Okay, great. Let’s look at how that plays out. Let’s assume that on average, the homes increase by 3% in value.” Remember, Allen’s was more expensive, so it’s going to be worth more. At the end of this 30-year period, once the mortgage is paid off, Allen’s house is going to be worth a million dollars. Now, remember, he paid a little over $400,000 for it, and now it’s worth a million. Pretty solid ROI on that. Manny, on the other hand, bought a less expensive home. It increased 3%. His house is only worth $806,000. So, right off the bat, you’re saying, “Yeah, that’s why we love leveraged growth.”

Brian: But wait, there’s more. Because remember, Manny was saving and investing during this period. He was taking that margin difference and investing that $700 a month. Well, wouldn’t you know it, now that $700 a month has turned into close to $1.1 million. Now, look, Average Allen, congratulations. On paper, you’re worth a million dollars. But we all know you can’t eat your house. You have to make really difficult decisions. You either have to downsize, which is a lot of people I think you realize downsizing, especially if you stay in the same community, is a lot harder than it is to just say it out loud because housing is expensive. There’s all kind of things going on. Interest rates are much higher now than they were back then. And you don’t want to have debt when you’re retired. So, it’s hard to eat a house. But you have Manny, yes, their house is not worth what Average Allen’s is, but they have a million-dollar portfolio to live off of. So that’s why their net worth statement shows close to $2 million in assets versus Allen just having the seven-figure house. But here’s what I’m telling you. Once again, you can’t eat the house. Manny the Mutant, he has close to $44,000 a year forever that he can pull out just using a 4% safe withdrawal rate. That’s a lot. You add Social Security on that. Now you’re starting to see how just small decisions on just how you live can actually build your entire retirement.

Bo: That’s exactly right. It was a million dollar decision to just have the idea of instead of having 33% of my income go to housing, I’m going to have 25%. Just that one decision over a 30-year period made a million dollars of difference. Again, these small decisions over time can stack up.

Decision #4 – Waiting to Invest (25:49)

Bo: And Brian, these have been significant, right? So, savings rate has been significant and buying a car has been significant and buying a house has been significant. But I think the one that I see the most people fail on. And I think it’s the one that I see the most people fail the most aggressively on is decision number four, and that’s waiting to invest.

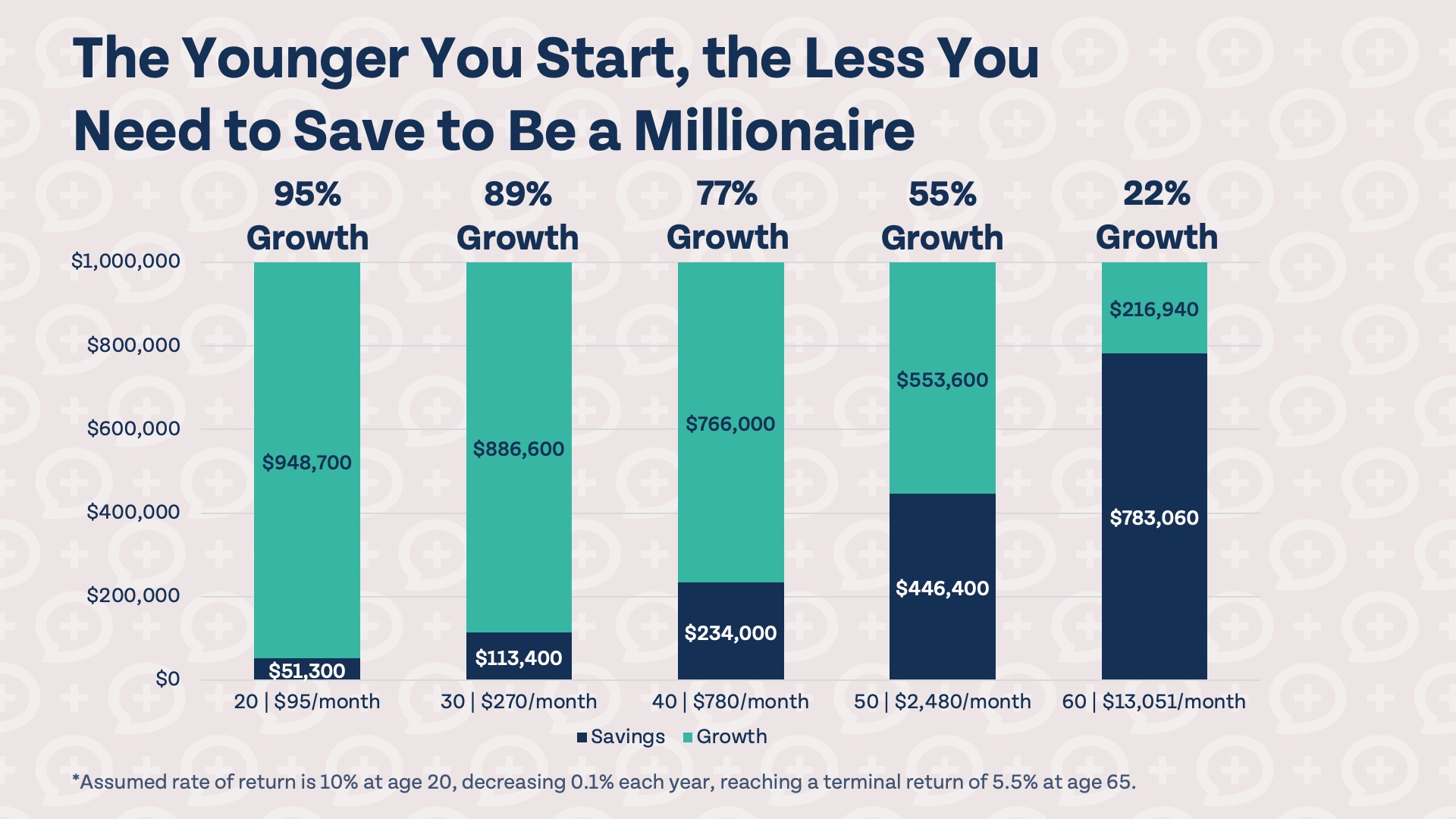

Brian: Yeah. I need everybody out there if you fell asleep during any portion of this or you need to scoot the chair closer to the TV screen, this is the one that’s going to be the biggest shock and a stat for you. Because this is the culmination of something we’ve been sharing with you guys. The most valuable thing you have going for you when you’re young, you’re a billionaire of time, is that component of time. And if you need proof of this, we have what we call our wealth multiplier. And we even talk about 88 times over. For a 20-year-old, literally every dollar that you come into possession of is worth $88 at retirement. But this is cruel. Like most things in life, it’s definitely not fair. So if you just wait and defer investing and turning your money into your army of dollar bills, by the time you’re 30, that same opportunity that could be at 20, 88 times over is now dropped down to 23. That’s right. So, you heard that it’s four times easier to build wealth when you’re 20 versus when you’re 30. If you fast forward to when you’re 40, now every dollar only has the potential to become $7 at retirement. You heard that right. We’re now talking about a factor of 10 for the 20-year-old over the person that’s 40 years of age. Guys, this is a scary thing. And then when we find out that the average American waits to start discovering the wonderful world of personal finance when they’re beyond the age of 30, we got a problem.

Bo: Now, I want to be clear, 30 is not as bad as it could be. It’s still young and you still have time to course correct. But again, if you start stacking these bad decisions, if you say, “All right, I waited till I’m 30. I’m going to start saving.” But all you save is the average American 4.6%. Now you’re beginning to stack these less than ideal decisions. And if you want to see how impactful that can be, let’s again, let’s go back to Allen and Manny. Let’s say that both of them wait until age 30 to start investing. And let’s say they both make the exact same income at age 30, $83,730. Allen is going to wait until age 30 and he’s going to say, “You know what? At 30, that’s when I’m going to start saving. I’m going to do what the average American does, but I’m going to go from 0 to 25%. I’m going to hit it running and I’m going to start crushing it.” Manny, on the other hand, says, “You know what? I understand that maybe I can’t do 25%, but I can just do something. If I can just start at age 20 and I can start saving 10%. And every year, I’m just going to get a little bit better and a little bit better and a little bit better. I’m going to increase by 1% all the way out until I get to age 35. And then I’m going to save 25% from 35 all the way to the end of my career.”

Brian: Hit pause because here’s something I need everybody to understand really quick. We just said Average Allen’s going to at age 30, he’s going to save 25%. That’s aspirational. That’s pretty powerful that he’s already at 25%. Meanwhile, Manny, because that’s such a big goal, he’s saying, “Nope, I’m going to make this digestible. We’re going to start at 10%.” And more than likely, your employer is paying for a good portion of this if you have a 401(k) at work. So, he starts at 10% at 20. Then he starts increasing at 1% every year until 25% at age 35. So if I’m doing this, if you do the math, he never catches up. At age 30, Allen is still saving more money. So this literally is going to show the example of somebody who just starts earlier, not more necessarily from a savings rate. I’d be curious to see how this plays out.

Bo: What’s really really interesting is we look at their two tracks. You look at their two trajectories over a working career from age 20 out to age 65. Allen still ends up with an amazing portfolio. Don’t mishear us. We’re not trying to poo poo on what Allen was able to accomplish. Because if you’re that 30-year-old that hasn’t started saving and you begin saving 25%, we love that. If you do that over a 35 year timeline, Allen ends up with a portfolio of $4.3 million. It is very very impressive. But Manny who figured out, man, time is my most valuable resource. When I can just start early and get a little bit better through time, Manny actually ends up with almost $7.3 million. It’s almost a $3 million spread just from starting early.

Brian: So then we were like, okay, let’s do some goal seeking because we already gave Allen’s doing 25%. What if he just because he deferred, he wanted to enjoy his 20s the most. What if he increased his savings rate at age 30 to 30% instead of 25%. Are you already seeing this on the screen? He’s still a $2 million delta between these. He even at 30% savings rate just because he started later is $2 million less. It’s $7.3 million versus $5.2 million.

Bo: He never got passed on savings by Manny. He always saved 30%. Manny only saved 25%. And so you would argue from age 30 till 65 Allen was the better saver. He was saving more money and still couldn’t catch him. But wait, there’s more.

Brian: You go to 35%. That’s a steep savings rate for somebody in their 30s. Still doesn’t catch Manny the Mutant who’s at $7.3 million. And then what’s the savings rate? Because like I said, we goal-seeked this. You’d have to save 42% of your income. Now, don’t mishear us because I agree most Americans don’t figure this out until they’re already beyond their 30s. I know a lot of our audience is in that key element between 26 years of age and 45 years of age. And you might have just come across our content. Get to 25% as fast as you possibly can because the longer you defer this, the more the weight falls on your shoulder and your savings and investment rate. We just want to highlight the fact that get in there early and often is rewarded. And that’s why we just want to draw light through mathematics and show you that you do have decisions not only with how you save and invest but also how you consume. And if you bring these small decisions together, you can change your life, you can change your children’s life, you can change the orbit of all those people that surround you. It is that important.

Closing – Success Creates Complexity (32:25)

Bo: What I think is so wild is these four decisions. How much am I going to save? What kind of car am I going to buy? What kind of home am I going to buy? And when am I going to start investing are decisions that most of you out there will make. It’s not like these are unique decisions that unique people are going to have to make. We all face these decisions. But if you can have the mindset of a financial mutant, if you can go against the grain, if you can think differently than the average American, you can have a future and you can have a financial security that does not look like the world around you.

Brian: So, we do shows all the time, we have collabs, we do other things. And what’s funny is we’ve been doing this so long since 2006 that we have you guys coming to us all the time that you started these simple decisions, but because of your success and your discipline, your life has gotten complex. And I feel so thankful that we get to be the educators that come into your house many times a week sharing the simple basic facts of how money, math, the intersection, how all these things work together. And then if you do this well and you do it often enough, success is going to find you and success is going to create the complexity that you realize, hey, I just don’t know what I don’t know. I don’t know where my blind spots are. I know I’ve only got one retirement and I don’t want to screw this up. We’ll leave the porch light on for you. That’s why we work with clients. By the way, we do need to correct the record. It’s not South Dakota anymore. We have one state that we’re missing. It’s the state of Vermont. That’s right. We have clients in 49 states. We’ll leave the porch light on for you. We love helping people master their money and really optimize their path so they get to do more of what they want to do and control their time and live their life how they want when they want and maximize all those key elements of life. I’m your host Brian joined by Mr. Bo. Money Guy team out.

Free Resources

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

Articles

How To Get Affordable Health Insurance in 2026

Health insurance premiums may make up a significant portion of your budget. How can you find more affordable health insurance? Is it ever worth going...

Articles

Millionaire Habits Revealed (2025 Client Survey Data)

Each year we conduct an annual survey of our millionaire clients. Some of the data is not too surprising. Yes, they have much higher than...

Articles

How Much Do You Actually Need To Retire?

Believe it or not, the concept of saving for your own retirement is a fairly recent creation. Brian, our Money Guy, predates the 401(k) plan....

Financial FAQs

Courses & Tools

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Recent Episodes

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

We Changed The 4% Rule!?

Retirement planning isn't as simple as following the classic 4% rule anymore. In this Live Q&A, we explain why the traditional retirement withdrawal strategy deserves...

Episodes

Is Aggressive Saving Derailing Their Short Term Goals?

High earners in their mid-twenties, cash poor, and a wedding 12 months away. In this episode of Making a Millionaire, we show Joey and Leah...

Episodes

Why This Money Advice Has EXPIRED

Traditional financial advice isn't always wrong, but some money rules simply haven't kept up with today's economy. In this episode, we reveal which classic money...