-

▼

-

▼

Skylar (23) and Milet (26) are already saving 25%, maxing out their Roth IRAs, and sitting on nearly $300,000 in net worth, all while Skylar works three jobs and lays 1,800 square feet of pavers in his backyard on weekends. The foundation is rock solid. Now it’s time to figure out if they can keep it rolling when life gets more complicated.

We walk through their sinking fund system, map their path to work optional by 50 to 55, and run the numbers on what their portfolio could look like at each milestone. We also uncover a solo 401k opportunity that could eliminate nearly $7,000 in annual taxes and break down why their new 457 could be one of the most powerful retirement tools they have for an early exit from the workforce.

Discover how two very different financial upbringings helped shape one financially aligned couple and why building strong financial habits early can create more flexibility for their wealth-building journey. Use our Wealth Multiplier calculator to explore how early habits could impact your own financial timeline.

Enjoy the Show?

Where You Can Watch and Listen:

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

- Episodes of The Money Guy Show every Friday

- Episodes of Making a Millionaire every other Monday

- Mini-shows every Wednesday

- Ask Money Guy Livestreams every Tuesday

- Tons of other fun content!

0:00 — You Can’t Plan Everything

Preview: We’re so focused on what’s happening tomorrow and right now. We’re not thinking like one, two, three years in the future. So let me ask you this question. There’s a whole lot of life that’s going to happen between now and the time that you guys turn 50 — job changes, family changes. We so desperately want to have the entire plan planned out. If something were to deviate, if something were to throw you guys off of your plan right now, how would you handle that?

0:26 — Meet Skylar & Milet

Brian: How old are you guys?

Skylar: I’m 23.

Milet: 26.

Brian: 26. How long have y’all been married?

Milet: August of 2024.

Bo: So about a year and a half. Awesome. So we’re still kind of in the early stages of this thing. How’s it gone so far? Year and a half in — for those that are getting married or about to get married, any words of wisdom you’d share about what’s worked well for you guys?

0:48 — Communication, Money & Getting on the Same Page

Milet: Communication. We just have conversations about everything. At the end of the day it’s like, how was work? How is everything? We want to know everything about each other.

Bo: When y’all started dating, were you on the same page about most things? When it comes to money and finance — were y’all already aligned, or did you have to get there?

Skylar: No, we were different. She had a car lease when we were dating. And I straight up told her, “You should pay that off before we get married.” Luckily she had the $10,000 in savings. She threw it at the lease, paid it off, and I was like, “Okay, maybe she’s serious about this. I can start introducing the other topics.” And then everything after that was pretty easy.

Milet: He’s the one that got me to do my first Roth IRA. He said, “You better start this account — this is what good financial people do.” And I’m like, “Okay, I’ll look into this.” He introduced me to all the financial things.

Brian: But I heard she had $10,000 already saved. So there were good behaviors there. This was not a fixer-upper. It sounds like the foundation was already in place on good financial management, at least in discipline.

1:48 — Two Very Different Financial Upbringings

Bo: So how did you know that? Did your parents teach you about personal finance?

Milet: Completely opposite, actually. My family — I grew up with a lot of credit card debt and struggling. So I was kind of seeing that and thinking, I want the opposite of that. I went the hyper-savings route. I would save like 50% of every single paycheck. I don’t ever want to not have money. So I went the opposite route.

Bo: They set an example of what not to do, and you noticed that.

Milet: I noticed the struggle and I’m like, I don’t really want that for myself. I always saved my money. So when he said, “Hey, you’ve got $10,000, you can probably pay off the lease now” — if you have the money, you might as well. So I clicked the button and paid it off that day.

Bo: What about you, Skylar? You obviously knew enough about personal finance to share it.

Skylar: My parents are very well off. They split when I was around 10 years old, but luckily both my mom and dad had a very good grasp on finances. I kind of leeched off them and took on their behavior — but for opposite reasons. They never showed that they had money. I always thought we were poor until I finished high school. They had a very, uh, frugal mentality.

Brian: He said the not-good word and you threw in the good one.

Skylar: I followed a lot of the same savings habits as Milet but for different reasons. Just a scarcity mindset — never enough, got to hold on to everything, never want to let any of it go.

Bo: Did they talk to you about money, or did you just observe the habits?

Skylar: I saw the habits. They never really talked about it. But slowly after I graduated high school, my mom started to open up — here’s what I invested in, here’s why you got into college. And it’s a lot easier to talk to my dad now because we work in the same field. He’s like, “Here’s what I did, here’s what you should do with your retirement accounts.” It’s getting a lot easier to talk to them. But in the beginning it was very silent. I kind of had to figure it out myself.

4:06 — What They Do for Work

Bo: You say same career field — what is it you do for a living?

Skylar: I’m a civil engineer. I currently work on airports — I do the designs and drawings for runway and taxiway projects. But I’m currently in a transitionary period. I’m switching from the private sector for airport design to the public sector for flood control. So I’ll be working on dams, channels, and floodgates.

Bo: So what made you decide to make the change? Walk us through the shift.

Skylar: There are two routes — public versus private. I’ve always wanted to try both before I settled in. My dad did both and ended up liking the public sector better. He’s always tried to push me that way, but I needed to try it for myself. An opportunity came up and I had to jump on it because I knew I’d regret it if I didn’t. And the money made sense — the base pay is about the same, but the government benefits are a little better. I’m more in it for the experience. The more experience on different types of projects I can put on my resume, the more hirable I am in the future. Plus I’m in the process of getting my California professional engineering license, and once I get that, I’ll get like a $40,000 to $50,000 bump.

Bo: Just from getting one license, you get a $40,000 to $50,000 pay raise?

Skylar: Yeah. Then I’ll be able to stamp my own drawings — that’s where the money’s at.

Bo: What is it you do professionally?

Milet: I’m an office assistant for the state.

5:56 — Net Worth Overview: Nearly $300,000

Brian: You guys are doing pretty good as it stands. You shared a net worth statement, and for two folks just starting out, it’s incredible. You guys have a total net worth of almost $300,000. You said you’re 23 years old, and you said you’re 26 years old, and you guys have $300,000 net worth. You realize how unique that is in the world in which we live. We’ve got a little under $60,000 in cash — checking account, emergency fund, some sinking funds. And then you have about $126,000 of investment assets, which is awesome. And you guys are homeowners. You have a home that’s worth $565,000 with a mortgage of about $456,000. So tons of equity in this house. I think there’s a lot of 23 and 26 year olds looking at this saying, “How could I be in their spot?”

Brian: How did you buy that house? Because I see the interest rate is also 3.99%.

6:48 — How They Bought Their First Home

Skylar: We bought the house in July of 2025 — we’re almost a year in. We put $100,000 down. The reason we were able to get such a low rate is we financed directly through the builder. It was a new construction community, so they were throwing all those incentives. It’s always been my dream to own a house since I was 18. So I’ve always been piling money into a brokerage account since I knew what I was doing. When we got married in 2024, we put our foot on the gas. I was living at my mom’s house — she was only charging me $500 in rent and split utilities. We were really taking advantage of that with our combination of good jobs and low expenses, shoving five or six grand a month for about a year. Then we looked at our accounts and said, “Hey, we have enough — why don’t we go start shopping for houses?” It was a complete surprise. We were just driving through the neighborhood, saw a for sale sign, went to check it out, and the lady said, “Oh, by the way, we have this cool intro rate of 4%.” And we ran the numbers against your 25% rule — it worked. So we moved in.

Brian: Is it a 30-year mortgage?

Skylar: It’s a 30-year FHA.

Bo: What made you decide on such a big down payment for the first house?

Skylar: We were just drilled on the 20% — this was before I found you guys with your lower rule. Starter homes in our area are about half a million, so automatically that’s $100,000 down.

Milet: We always had that number in mind. We started our marriage with maybe $50,000 in savings, but in those first six months we really buckled in — no-spend months, putting five to six thousand a month into savings. That’s really how we built up the down payment. And a lot of it was him investing since he was a teenager into an actual brokerage account. He had a brokerage account when he was 18. So that was a lot of my contribution to it.

9:00 — Savings Rate & the Sinking Fund System

Brian: What I want to know is the savings rate, because I want us to know how extreme we’re going into this — because every indication is y’all are hitting on all cylinders.

Skylar: We’re currently at 25% with just the retirement contributions and investments. But on top of that, we have a lot of cash in our sinking funds because we have all these little buckets we like to save for bigger expenses.

Milet: Yeah, we do the sinking funds. When I was single I had my little buckets — $100 for entertainment, $100 for the car, whatever. As we got married, we combined the buckets. We have about eight of them: saving up for a new car, car registration, annual subscriptions, car insurance, house maintenance, house improvement, entertainment, and then we have a little bucket for each of us — the Skylar fund and the Milet fund. That’s just money we can spend on whatever we want, like our hobbies.

Bo: Do you ever actually spend the money?

Skylar: I try to save mine up in my “I want” bucket. But then whenever she sees something nice I’ll buy it for her and say happy birthday.

Bo: So you spend your bucket on her.

Skylar: Yeah, my bucket pretty much goes to her. But occasionally I’ll get a new tool or a car part. Cars, mechanics — I fix my own car. That’s one of the ways we’re able to save a lot of money.

10:51 — Making Memories in Nashville

Brian: Y’all came to Nashville to record this show and you packed three trips into one visit. You went to Gaylord, the Grand Ole Opry, Broadway, the honky tonks, the Country Music Museum — y’all did everything. Is that just y’all’s personality?

Milet: I’m very much a planner. I need to know what we’re doing each day. I even like to know where our money is going — we made a budget for the trip and made sure everything was allocated appropriately.

Bo: How do you track your spending and budgeting?

Skylar: We have a spreadsheet template through Google Docs. Over the last five years I’ve molded and tailored it to something that works for us. After every time I buy something — even while I’m checking out at the grocery store — I enter it into my spreadsheet.

Bo: Have you ever thought about automating that with something like Monarch?

Milet: No, because I like the act of actually doing it.

Skylar: We actually started the same template at the same time, kind of separately, but doing the same thing.

12:11 — Household Income & Future Goals

Bo: Right now your total household income is $173,000. You just said your pay is going to go up by $40,000 to $50,000 with the certification. So we’re talking about a very young couple making north of $200,000 a year. Where are you guys going?

Brian: What are the goals? What are the struggles? What are you hoping to get out of today?

12:43 — Three Jobs and the Work-Life Tradeoff

Skylar: One thing on why the income is so high — I work three jobs. On top of civil engineering, I do private piano lessons, pulling in about $25,000 a year. And I also work weekly at a church — they pay me about $200 a week to play piano for the worship services. So I’m working maybe 55 to 60 hours a week between those three jobs. One of the chinks is I feel like I work a lot and don’t get a lot of time to just sit and relax or hang out with Milet. I’d like to come down on the working.

Bo: What stops you from cutting back?

Skylar: We only meet the 25% housing rule if I keep that up. Because of our monthly mortgage — it’s $3,360 a month.

Brian: But you’re counting those sinking funds in that number, aren’t you?

Skylar: Yes. Yeah.

Brian: I think you’ve got your thumb on the scale on the pressure you’re putting on yourself. 50 to 60 hours a week working — what do y’all do when you’re not working?

Milet: Since we got a new construction house, we’ve been working on the yard every single weekend. He’s putting in 1,800 square feet of pavers by himself, building retaining walls, adding water lines, installing gutters — and he’s just YouTubing it as he goes because he didn’t want to pay the contractor quotes. He said, “I could save so much money if I just invested the difference and did it myself.”

14:43 — Planning for Kids & the Next 10 Years

Bo: I want to think about the next 10 years. What does your life look like differently 10 years from now?

Milet: Hopefully we’ll have kids.

Bo: Want to plan for a family? How many kids do you want?

Skylar: I would like two. So it’s easy to go on the rides at Disneyland.

Brian: Who would have thought they planned that through? I’m a fellow Disney fanatic myself.

Milet: That was one of the first things I saw when I watched one of your episodes — the partnership stuff. I loved it.

Bo: When you have that family, will this house still work for a family of four? Good so we don’t have to worry about that.

Brian: What do you think will change when you have kids?

Milet: I’m hoping to not have to work, at least for the first three to five years of the kids’ life. The goal is for Skylar’s income to go up enough to cover mine.

Brian: I heard from a bird that he might make $40,000 more a year once that certification comes in.

Bo: But if we add $40,000 and take away the piano lessons and the church — does he have to keep working three jobs for that to work?

Skylar: The goal is no. If I cut back the extra jobs, just focus on the primary, and she stays home — we go down to one income. I’d probably be hovering around $140,000 to $160,000.

Brian: When do y’all think you want to have kids?

Skylar: Three to five years. We’re still young, we want to travel first and enjoy a little more of our 20s, then hit closer to our 30s.

Brian: If money wasn’t an issue, would it still be three to five years?

Skylar: Yes, for sure. I’ve always said I want to have kids around 30, and I’m 26, so that’s why I’m thinking that window.

Brian: How close together do you want to have them?

Milet: Two to three years apart. That’s the gap between me and my brother, and me and his brother. As adults we’re great friends. We grew up together almost at the same time. I like that relationship.

16:54 — Enjoying Life Now

Bo: You said one of the things you want to do is enjoy your 20s before you have kids. Do you feel like you’re doing that now, or does it feel like you’re nose to the grindstone every single weekend laying pavers?

Milet: I think we’re easing up this year. Last year was very strict about saving money — we had to get the house. We got the house, and now it’s like, okay, we have to finish the house. But now that the house is almost done, I’m like, maybe we can start doing more trips. We already have a couple planned this year. All our money was going to the house. House is done. Now we can start living more.

Bo: What trips do you have planned?

Skylar: We’re going to Japan for my brother’s graduation trip — a big family trip. And I want to go to Mexico to visit my family, maybe twice this year.

Milet: And there’s a friend’s bachelorette trip in Utah next month. These are things that in the past we’d have said maybe, maybe not. Now it’s like, yeah, we have some money to spend. Let’s just do it.

Bo: Are Japan, Mexico, and Utah things you have sinking funds for, or are you just doing them out of cash flow?

Milet: We have a sinking fund for that — it’s one of the eight buckets.

18:22 — The Sinking Fund Logic

Bo: Did I hear correctly that one of the buckets is car registration?

Milet: Our cars are so old so it’s not that expensive, but since it’s an annual expense I put like $11.36 every month into it. And because all of those buckets are in a high-yield savings account, they’re making money. It’s just somewhere to pull money from so we don’t have to stress about it month to month.

18:56 — Where They Clash: Impulse Buys & Clutter

Brian: What do y’all fight about?

Skylar: Not really huge fights. What are we eating tonight? Where do you want to go?

Brian: Let me tell you — that one doesn’t change. What have you figured out so far? What is it that you do that drives her nuts?

Skylar: I think a lot of the impulsive purchases sometimes.

Bo: Hold on — you’re the impulsive purchaser?

Milet: Yes. Earlier this year we went to Vegas, stayed at an Airbnb that had a water softener. He loved that water softener so much that the next week he paid $1,800 to get one installed at our house. That’s the kind of impulsive buy he does.

Brian: Y’all know what the definition of an impulsive purchase is, right? This is golf clubs. It’s an exotic sports car without talking it through first. He bought an appliance for the house.

Bo: Was it the fact that y’all didn’t have a conversation about it, or was it just that he experienced it and wanted it immediately?

Milet: We had talked about doing it — we said we were going to save up for it after the backyard was done. But after that Vegas trip, within a week it was installed.

Skylar: We always talk about big decisions like that, but how long do we wait before we actually make them? That can be a point of conflict sometimes.

Bo: So what happened in that specific case — you basically said, “We have money in the house improvement sinking fund, let’s just do it now”?

Skylar: Right. We had about $2,500 in the house improvement fund. The water softener was about that much. And I found our neighbor — he works as a plumber, does great work, and charged us $250 less than the quotes. Then we just cash-flowed the rest because we have quite a bit of discretionary income left over each month.

Brian: All right. What is it you think drives him nuts?

Milet: I do a lot of little purchases for my hobbies. We live near Disneyland, so I like to go there a lot. I also like the little trinkets — the pins, the collectibles. Right now I’m really into plants since we have a house. I’m buying pots and soil and learning how to repot everything. And he’s seeing another plant come in and asking, “Where are we going to put this?” It’s starting to look like Rainforest Cafe in our living room.

Brian: Is it the spending or the clutter that’s the issue?

Skylar: I’d say it’s more the clutter. It’s never an issue of whether we can afford it — we know we always can. It’s just, do you need another one?

Milet: He’s very minimalist. I have a lot of clothes, shoes. I see a purse I like, let’s buy it. But he’s like, I don’t need another shirt, I don’t need shoes. He has the same three pairs of shoes since college.

Brian: So far, y’all are like the ideal star students. I’m trying to figure out why you came on Making a Millionaire. I actually read in the notes — you want to be a millionaire by the time you’re 30. Is there a “why” behind that?

23:54 — The Millionaire Goal & Work Optional by 50–55

Skylar: No, that was just like — okay, that’d be cool to hit this number. But after I submitted that question, I started running the numbers and realized that’s not going to happen unless we were saving like 80% of our income. So I’ve kind of gotten away from that. I know it might not happen by 30, which is fine. I’m not planning to retire at 30 — I’m just getting started in my career. But our end goal is to be work optional around age 50 to 55. That’s where a lot of our questions come from. We want to know if we’re on the right track based on our current investing and savings rate. And the unfortunate thing is there’s not a lot of people around us we can talk to. The people in similar financial situations are a lot older. The people my age are still trying to figure out what alcohol they’re buying this weekend. We don’t know if we’re behind the curve, on the curve — that kind of thing.

24:57 — How Much Do They Actually Need?

Bo: Let’s talk about this. If we think about work optional life around 50 to 55 — how much money do you need to be able to spend at age 50?

Skylar: We’d like to be at $120,000 after-tax take-home per year.

Bo: How’d you come up with that?

Skylar: $10,000 a month. I based all my calculations on having about $3 million invested.

Brian: But y’all don’t spend $10,000 a month. You spend currently somewhere between $5,000 to $6,000 a month if you take out the sinking funds.

Skylar: That’s true. But we don’t want to stop the sinking funds, even after we stop working — it’s just how we’re wired. If I have $10,000 in my entertainment fund, I can plan a big trip with that money. We keep adding to those buckets every month and as they grow, I can see more opportunities.

Brian: Do y’all ever worry about fatigue? I resembled y’all a lot early on. But I’ll tell you — as you get into your 30s and 40s, you’re not going to want to track every dollar forever. Do you think you’ll always want to stay on such a tight budget system versus a more automated approach where the money is going where it needs to go and you just live your best life with what’s left?

Milet: I’ve never really thought about any other life without spreadsheets. I’ve been doing this since I was 18. The spreadsheet is kind of like a security blanket. I make sure the money’s there — we have $500 left at the end of the month, cool, we put it toward the brokerage account or more savings. It’s a security I didn’t grow up having, and now I see it like, we have money left over at the end of the month? That’s crazy.

27:25 — Can They Do It on One Income?

Bo: If the goal is work optional by 50–55, you want $10,000 a month after tax, you’re going to have two kids about three years apart, and you’re going to drop from three jobs down to one — can you do that on $140,000? At that income, if you save 25%, is that going to get you to the goal?

Skylar: We haven’t actually run the numbers yet on that new income. Everything we’ve run is based on right now. I guess that’s kind of our downfall — we’re so focused on what’s happening tomorrow that we’re not thinking one, two, three years into the future.

Bo: Let’s say we did the numbers for you and ran it and said, “Hey guys, it doesn’t get there — you’re going to have to keep working three jobs until you’re 50.” How do you feel about that?

Skylar: Then that’s what happens. I make the rules. I just follow them.

Bo: What I’m trying to illuminate here is that there’s a whole lot of life that’s going to happen between now and when you guys turn 50. Job changes, family changes, unknown unknowns you’re not even prepared for. We achievers and planners so desperately want to have the entire plan mapped out. But what we say on the show all the time is that when you’re early on and just starting out, it’s more like throwing horseshoes — you’re not trying to be laser precise, you just want to get in the general direction. And most folks, if you can save 25%, you’re going to be in a great spot. What I worry about is: if something were to deviate from your plan right now, how would you handle that?

Skylar: The first thing that would probably change is our lifestyle — stop saving so much into the extra buckets. That’s where most of our margin comes from, and I think that’d be the easiest thing to trim down if something affected our income.

29:34 — Walking Through Their Financial Order of Operations

Brian: Talk to us about where your savings are going on a month-over-month basis right now.

Skylar: I have 9% going into my 401k with a 3% match. Both of our Roth IRAs are getting maxed out every single year. And on top of that, we’re putting $1,000 a month into a regular taxable brokerage account. We originally earmarked that as a pay-off-the-house-early fund when the balances meet up, but now we’re starting to think it’ll be a bridge account. Since our interest rate is so low, we’d rather just hang on to the mortgage.

Brian: That’s music to my ears. And that makes sense at least until you’re over 45, because with kids, you’re going to want that margin.

Milet: Through my job I have a 457 account — I put in $250 per paycheck, so $500 a month. And then I have a pension through my job because it’s a state job. I put in 8% through my paycheck, but I get reimbursed 3%, so it’s really 5% out of my money.

Brian: Are you sure they’re not also putting more money into the pension on their side?

Milet: I don’t think so. It’s a very entry-level job and it’s only for three years, so my understanding is I put in 8% and they refund me 3%.

Brian: Usually government pensions — like where I used to work — the employees put in 8% but the government was putting in 11%, because the math requires you to pre-fund a ton of the assets when people retire at 50 or 55. You’ll probably want to find out the vesting schedule on that pension.

Milet: I have no idea. Okay, I’ll look into that.

Brian: On your 457, is that Roth contributions going in?

Milet: Yes.

Brian: Awesome. And on your 401k — when you switch to the new job, it’s going to switch over to a pension and 457 system?

Skylar: Yes. Same as hers — likely saving the same amount, probably around 12%.

Brian: You know what’s great about those 457s? If you retire at 50 or 55, there are no early withdrawal penalties.

Skylar: Really? We actually didn’t know the difference between the 401k and 457 — she just kind of rolled the dice on which one to choose.

Milet: We chose right, I guess. It was the same otherwise — there’s no matching.

Brian: Yeah, then that’s a great choice, assuming the investment options are solid.

32:32 — Questions for Brian & Bo: Rolling the 401k Into a Roth?

Bo: What questions do you have for us? What are some things that we can give you answers to?

Skylar: Since the profit sharing and employer match at my current job goes into a pre-tax bucket in the 401k — as I’m leaving, should I pay the taxes on it now and roll it into a Roth? Or should I leave it as is? I also don’t want to break the pro-rata rule, because I expect our income to go over the $240,000 limit where we’d need to do backdoor Roths. I’m really unfamiliar with those types of rules and tax strategies, and I want to make sure I’m doing it right.

Bo: The great news is right now you don’t have to worry about backdoor Roths, because your income is below the threshold where you can contribute directly. But if it does go up, you would want to keep that intact. One of the things you want to check with your 457 provider is whether they’ll accept rollovers from other retirement plans. Most will, but some have restrictions. If so, you could potentially roll your 401k from your old employer into the 457 at the new employer. That said, there’s also nothing wrong with leaving your 401k if your current company is with a good provider like Vanguard or Fidelity. You don’t have to move it.

Brian: On the Roth conversation — y’all live in California, so you’re in a relatively high income tax situation federally, and then you add the state piece. You’re probably somewhere in the 6 to 10% state bracket and the federal 22% bracket right now. It would just break my heart to watch 30% evaporate just for the sake of converting to Roth when y’all have the ability to fund Roth IRAs every year because your income isn’t that high. You could also look at whether they offer Roth options on the 457 — a Roth 457 would be pretty powerful too.

35:07 — Tax Planning: Side Income & the Solo 401k

Bo: On your side income — the income from the church, how do they pay you?

Skylar: I’m a W-2 through the church. The piano teaching is self-employed.

Brian: How much are you making through the teaching?

Skylar: About $24,000. I have around 10 students.

Bo: There’s some fun tax planning you can do given that it’s self-employed income. Do you currently owe taxes or get a refund?

Skylar: We actually had to pay a lot last year because I filled out my W-4 wrong when we got married — I didn’t do the extra withholding. We paid about $8,000.

Bo: Lesson learned. Make sure you’re paying at least as much as you paid last year — or once your income gets over a certain level, at least 110% of last year. If you were naturally getting pay raises and withholding was protecting you, there’s nothing wrong with writing that check in April as long as you’re avoiding penalties. The worst tax in the world is those underpayment penalties. It’s just giving away free money.

Brian: Y’all are doing so many things well that even for a financial planner, I’d send you back in the water and say you’re close, but you just need someone to do the math exercises with you and make sure you’re on the right path. And as success adds complexity, tax planning is definitely one area where someone could add real value. And this year is especially unique because you’re changing jobs, you contributed 9% to your 401k so far this year, and now with the new job you’ll have access to a pension and 457. Given the self-employed piano income, there’s even a potential to do a solo 401k. In future years — not this year, because you already contributed to a 401k — you might be able to make that entire side income essentially disappear from a tax standpoint. A 457 through the government job and a solo 401k through the side business exist under two different parts of the tax code, which is a completely legal way to double-dip on retirement savings.

Bo: If he were to shift that $24,500 into a solo 401k rather than showing $33,000 of taxable self-employed income, he’s only going to show about $8,500. Just doing that, he’d save almost $7,000 in taxes. It’s a great opportunity.

Brian: This year you want to be careful not to overcontribute between what you put in with your current employer and a new solo 401k — you’re still capped at $24,500 total across both. You’ll want your accountant to help you coordinate that. Yeah, that got real nerdy real fast. There’s some exciting stuff to do there. What other questions do you have for us?

38:41 — Are They Too Cash Heavy?

Skylar: Are we too cash heavy in the sinking funds? The likelihood of us using all that money at the same time is very low. I know cash isn’t making much money just sitting in a high-yield savings account. I want to throw it into the S&P.

Brian: Let me ask you this, because this is where I catch financial mutants who are fibbing on both sides. You said you want $10,000 a month in retirement. What do you actually spend a month?

Skylar: We spend $5,000 a month.

Brian: Do you see how unique that is? So emergency reserves wise, you’d probably be fine doing three to six months. I’d go a little conservative since you already have the cash. You have over $50,000, and $30,000 would cover six months. So yeah, you probably could simplify.

Bo: Sinking funds for big things — vacations, a new car — make total sense. But the $11 a month for car registration? We might be majoring in the minors there. I don’t want to break your system because it’s clearly working. But in reality, you probably could streamline, be a little more efficient. And when you add efficiency, you tend to add effectiveness — which prevents you from holding so much cash and gets some of that money working harder for you.

41:39 — What’s Actually Next

Brian: I see y’all as having enough assets that we ought to figure out ahead of the curve, behind the curve, or right where you’re supposed to be. And then after that, you’ll need a financial enabler in your corner.

Bo: Because if I could go back in time — life has turned out pretty good for me — but if I could change one thing when I was in my 20s, pre-kids, I’d have gone to more Tuesday night movies, more coffee shops, more of that little stuff. I was so tight and so worried about saving every dollar that I assumed those things were going to break the plan, when realistically the behaviors I had in place meant the plan was never going to break. I think I could have not focused so much on being perfect so early and still arrived in the same place. Sounds like you guys are already doing more of that — I just want you to recognize it as something worth protecting.

Brian: And I’d give you the guidance of doing a specific exercise as a couple. You’re a little different — you mentioned the trinkets from Disney. You don’t need a sinking fund for that. You just need to have a conversation that says: we’re going to make sure you get to do what brings you happiness without regret. And the same for you, Skylar — what are those things that, if they were on the table, would make you happy?

43:00 — Abundance Goals: Rally Cars, a Pilot’s License & Disney

Skylar: I’ve always wanted a play car — something I can mess around with.

Milet: He means like an RC car.

Skylar: No — I’ve never driven a manual car before and I’ve always wanted to learn. I’d need to buy one in order to do it. And our cars are old. We have a Honda Pilot with 300,000 miles on it and a Prius with 220,000. They’ve lasted this long because I take care of them, but eventually we’d like something new. I’d love a Honda Fit — those little rally cars — modified to drive in the desert. That’s not a daily driver, that’s a hobby car.

Milet: Another goal he has is a pilot’s license.

Skylar: Since I work in aviation — I’m always on airport construction sites, always talking to the tower and the pilots — I see those guys flying and think, that’d be so cool. But in California, it’s going to be $20,000 to $30,000 just to get a private pilot’s license. I don’t know where that fits in the Financial Order of Operations.

Bo: There’s no pilot’s license step — because those are abundance goals. Once you’re saving 25%, everything else is fair game. Honda Fit rally cars, a private pilot’s license — all of it is fair game. Once you’ve checked the box and done what you need to do, you get to spend freely. That’s the whole point of the 25% rule.

Brian: See, now we’re starting to get the real stuff out. And you don’t have to be bashful about it. If it brings you joy and happiness, it’s okay to spend this money. Sometimes with us financial mutants, we’re so good at saving and so rewarded by building these nice net worth statements that we need someone in our ear saying, “Do it — go enjoy yourself.” I want you to live this life with so much excitement and zeal that when you get to be my age, you look back and say, “Well done.”

Bo: Awesome. We’re excited to get to work. We’ll put together a plan and see what path you guys are on and whether it’s the path you want to be on. Thank you guys so much.

45:46 — Post-Episode Analysis

Bo: Brian, what an awesome conversation with Skylar and Milet. I don’t know exactly what to say, because man, they’re doing a lot of stuff really, really well.

Brian: This one threw me a little bit because I came in thinking I was going to bring some old-man wisdom — like, look at these young financial mutants, there’s no way they’re doing everything right. It’s not uncommon to see people who are so amped up about saving for the future that they’re doing it at the expense of building memories and enjoying today. But SkyleMiletllette are actually not only great at saving and building wealth — they’ve done a very good job of making memories too. Even when they came to Nashville, they had a hit list that took out the entire city in two days. Really impressive couple.

Bo: Yeah, they’re doing a lot of stuff right. But they still have some unknowns coming their way. When we broke down their savings strategy: Skylar’s putting 9% into his 401k with a 3% match. Milet’s putting money into her 457 on the Roth side. They’re both maxing out Roth IRAs. They have $1,000 a month going to an after-tax brokerage account. When you look at their savings rate, they’re currently saving more than 25%. And this doesn’t even factor in Milet’s pension. Even without the pension, the future looks pretty bright. At 23 and 26, I’d argue they’re kind of already in step eight of the Financial Order of Operations.

47:38 — The Solo 401k Opportunity

Brian: Let’s see if we can add some value to these overachievers. There’s a unique thing with the 457 on the table plus enough side income to where a solo 401k could be really powerful.

Bo: As Skylar changes jobs, he’s going from having access to a 401k to now a 457. And those exist in two different parts of the tax code. Some of his side income — about $33,000 right now — is all taxable. As a self-employed sole proprietor, he’s going to pay about $9,200 just in federal and state income taxes. But in future years, if he opens a solo 401k, he could defer $24,500 into it. Instead of showing $33,000 of taxable income, he’s only going to show about $8,500. Just that one move would save them almost $7,000 in taxes.

Brian: Not that they necessarily need to save more — but it is an opportunity to save on taxes. Now, this year he has to be careful because he’s transitioning jobs and already contributed to a 401k. He’ll have to coordinate with his accountant to make sure he doesn’t exceed the salary deferral limit of $24,500 across both plans. Another great benefit here is that because they’re so young and want to leave the workforce early, that 457 is not going to have early withdrawal penalties — so it adds real planning flexibility.

49:35 — Roth vs. Pre-Tax at Their Stage

Bo: They’re both doing Roth contributions, which we think makes a ton of sense for them. When we did a little analysis, it looks like they’re going to be in roughly a 28% total marginal tax bracket. So they kind of fall in that gray area where they could do Roth or pre-tax. If cash flow feels a little tight, pre-tax frees up monthly cash flow. But we do love loading up those Roth dollars at their ages.

Brian: In that gray zone, I’d still probably lean more toward Roth personally. I think they’re going to have even bigger peak earning years in the future, and you’re only in your 20s once. You can really lean in heavily on that compounding growth and the wealth multiplier right now.

50:25 — Running the Numbers: What Their Future Looks Like

Bo: So what kind of trajectory does this put them on? If they continue saving at their current clip — a little under $44,000 a year, starting right now at an average age of 25, saving 25% of their gross income — the numbers get really exciting. Assuming a 9.5% annualized rate of return, by the time they get to age 50 they have almost a $5.8 million portfolio. By 55, almost $10 million. By 60, over $15.6 million.

Brian: Even in today’s dollars, based on what they’re doing, they are well on their way to being work optional somewhere between 50 and 55. But we know life has a sense of humor and likes to throw curveballs. Could they still pull this off even if Milet stays home and income drops significantly?

Bo: I think even if the side income went away and Milet stayed home, I don’t see a scenario where they don’t save 25%. That’s kind of a given for this household. Even if the income dropped to $140,000 a year and they were saving 25% — which is $35,000 a year — they’re still in an unbelievable trajectory. Almost $5 million by 50, a little over $8 million by 55, $13 million by 60. They’re still looking at work optional right around that magical 55. If they can just keep the good decisions they’ve been making rolling forward, the future is very bright.

Brian: If you do it right early, you can do it light. That is the big takeaway from today’s show. I know the audience is going to ask, “Where were the warts?” But here’s the truth: you get away with a lot when you start early and do it often. Lots of grace in your great big beautiful tomorrow.

Bo: But we also don’t know what could change — kids, family, job circumstances. What I love is they’ve made the hard decisions to put themselves ahead of the curve. Now they’ve got to finish the drill. But because they’re doing so well so early, they’re going to be able to handle whatever life throws at them if they can keep that mutant mindset moving forward.

Brian: So if there are other financial mutants who want to come on Making a Millionaire, where do they need to go?

Bo: If you want to be a guest on Making a Millionaire, go to moneyguy.com/apply. Or if you want to check out any of our free resources and tools, go to moneyguy.com/resources.

Brian: Skylar, Milet — you get a gold star. You rocked this thing. Thank you so much for coming on. I’m your host Brian, joined by Mr. Bo. Money Guy team out.

Free Resources

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

Articles

The Best Tools for Filing Your Taxes in 2026

Have you filed your taxes yet? You still have ample time left until the April 15th deadline, but it’s probably best not to procrastinate too...

Articles

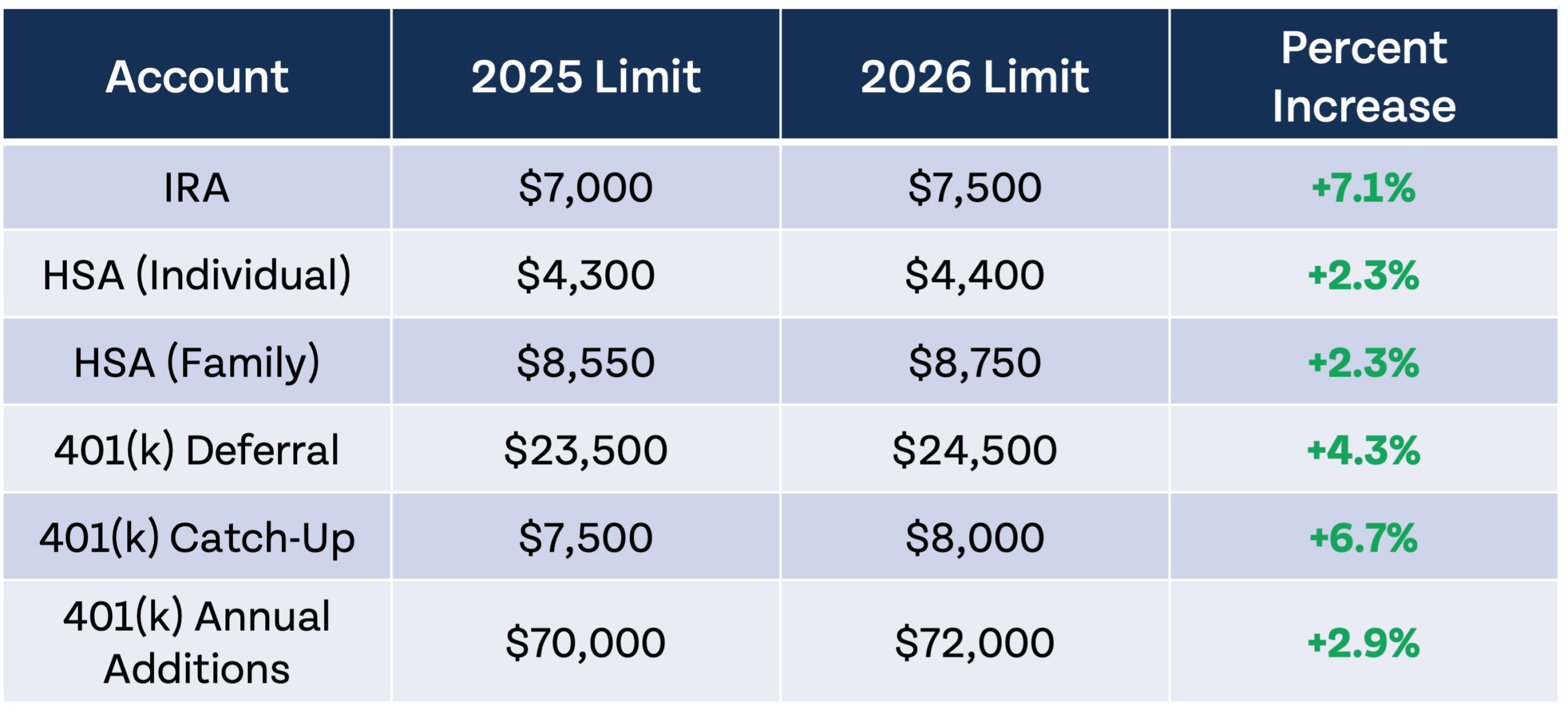

The IRS Just Announced 2026 Tax Changes!

Each year, the IRS adjusts retirement account contribution limits, standard deductions, marginal tax rate brackets, and more for inflation. I’m happy to announce that it...

Articles

The Best Tools for Filing Your Taxes in 2025

I don’t know if there’s anyone out there that looks forward to tax season. The average American certainly doesn’t, and it’s the least favorite time...

Financial FAQs

Courses & Tools

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Recent Episodes

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

Financial Advisors Correct the Internet (Part 2)

Is viral financial advice doing more harm than good? In this react episode, we correct the internet once again and separate the news from the...

Episodes

These Money Moves Feel Like Financial Cheat Codes

Want to build wealth faster without taking unnecessary risks? We break down seven financial "cheat codes" that can dramatically improve your long-term finances and help...

Episodes

Do You Really Have To Budget Forever?

Do you need to budget forever? Brian explains when to graduate to cash flow management & focus on what can help you move the needle...