Change your life by

managing your money better.

Subscribe to our free weekly newsletter by entering your email address below.

Subscribe to our free weekly newsletter by entering your email address below.

With new tax legislation looming, now is the time to understand what’s real, what’s hype, and what you can do about it. We walk through the key changes being discussed in Congress from adjustments to the standard deduction and SALT caps to updates to the tax brackets and child tax credit. We also tackle financial mutant questions about managing debt, mortgage prepayments, and 401(k) strategies. Whether you’re a financial mutant or just trying to stay ahead of tax changes, this episode will help you prepare confidently and wisely.

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

Brian: I don’t know if you guys have heard, there is a tax bill that’s floating around out there. We needed to tell you what’s noise and what do you actually need to know.

Bo: Brian, I am so excited to talk about this because we know that the financial landscape is ever changing and there are only a few certainties in life, death and taxes. And this is super interesting because right now it sounds like there may potentially could be some tax changes coming down the pipe, and we want you to know what they could be and how they might affect you.

Brian: Now, I’ll throw the dash of moneyism out there is that we typically don’t like to cover anything until it comes through both sides of the legislative process, both the House and the Senate, but there’s so much out there in the news media. I told the crew, I was like, “Look, we got to cover something just to let people know.” So, just so we can express the fact that this still is only half baked. We’ve got to get it through Senate. There’s going to be horse trading. The political process is always a mess. But I needed you guys to at least know some of the broad themes that are going on so you can go ahead and start preparing yourself because it will move fast. Once the Senate and the House start doing their negotiations back and forth, it will start moving faster. And we want to kind of give you the overarching parts that you can start planning for your personal finances.

Bo: And don’t you worry, when we actually have law, we’re going to cover that. We’re going to do a deep dive to let you guys know what’s in there. But as we were thinking about this legislation, we’re thinking about what’s okay, what would be an interesting way or an easy way to sort of lay it out for you. And we thought about the personal income tax return. And when you think about your personal income tax return, there are really sort of four sections if you want to think about how it’s broken down. You have the money you make. That’s like all the income sources you have. Then you have the part where you get to reduce the money that you make or at least what the IRS recognizes as the money you make. Then there’s a calculation that takes place that determines, okay, how much tax do I owe? And then there’s a part of your tax return where you can actually reduce the amount that you owe. That’s where credits come in. And so we thought about, okay, if these are sort of the four broad sections, very generally speaking, of a tax return, how do some of these tax changes, potential tax changes hit each one of those sections?

Brian: Now, the first one is the money you make, gross income. We don’t really have a slide on this one other than the headline because this is where you see everybody talks about is tax tip income going to be taxable? Is social security going to be taxable? Remains to be seen. Like I said, we’re only half baked. We’ve got the House bill. We do not have the Senate bill. I will be curious to see, but we didn’t want to put any additional slides on this until we got the full details from the Senate once they get through the negotiations.

Bo: So then when you move down from gross income, you get into, okay, well, how much income does the IRS recognize? Because it’s given us some things that will allow us to decrease the amount that our taxes are computed against. And so one of the big things and a lot of what this bill is is there was some tax legislation that came out in 2017, the Tax Cuts and Jobs Act. And a lot of what this legislation is is it saying, “Okay, are we going to allow things that changed in 2017 to expire or are we going to allow them to remain?” And one of the big things that’s going to hit a lot of households is the standard deduction. And then for those of you that don’t know the language, when you fill out your tax return, you have two choices. You can either take the standard deduction or you can itemize your deductions where you get mortgage interest and state income taxes and other types of items where you can create your deduction list or you can just take the stated standard that the government allows each year.

Brian: Now look, we’ve pulled the stats. 90% of taxpayers actually use the standard deduction. So this is a big deal. The big driving factor for why we even need updated tax legislation is because you see look at what happens to the standard deduction is it basically gets cut almost in half if we don’t bring back you know or make these changes permanent because they all sunset which means they go away at the end of the coming year of this, it’s actually this year, that’s right. So I always been for years I’ve been saying 2025 is when this, well here we are living in it. So that’s why we know that something will happen is because you know politicians they know that you know taxes going up is less than ideal for getting elected. So that’s why I think that you will see bipartisan they will want to do something just because they want to keep the people happy.

Bo: So, if the legislation passes, it does seem that the standard deduction will increase for single individuals from $15,000 to $16,000, for married filing jointly from $30,000 to $32,000. And there is an additional senior standard deduction that is currently a $2,000 addition that if this passes, it’ll go to $4,000. Now, it is important to note that this increased standard deduction, the little cherry on top, is only set under the current proposed legislation to go from now until 2028. So, they’re kind of even kicking the can down a little bit further in terms of when they’re going to lock in.

Brian: But long term, this would make those changes permanent. So, the standard deduction would stay at current levels instead of sunsetting like it’s done in the past. But, they put a little juicer in there probably for political purposes.

Bo: That’s right. So now that’s the standard deduction. Well, then there’s another part of the population that itemizes their deductions where essentially they calculate some of the allowed expenses that you’re able to deduct against your income. And probably the most significant change that has been talked about that will likely be in the bill in some form is the salt deduction.

Brian: Yeah, for those that don’t know, you know, years and years if you live in a high tax state, you know, the only consolation prize you got was, hey, at least it’s deductible. You know, so a lot of people then the tax bill came out in 2017 that actually now put a cap and it said, look, you only get to deduct the first $10,000. And this is not just your state income tax. It’s also your property taxes and all your local taxes. So, you can imagine this made some waves if you lived in one of those high tax states. And it doesn’t, by the way, it doesn’t even have to be high. You could just be in a high property tax state. And all of a sudden, this you get captured where you’re limited how much you could deduct. Well, they’ve listened to some of the criticism and they’ve actually expanded this under the proposed legislation to $40,000 cap with the caveat that it starts phasing out once your income is over $500,000 back down to that $10,000 cap. So, this will allow people to expand that if you live in one of these higher tax areas or you pay high property taxes. It looks like the salt deduction is going to get expanded to a degree.

Bo: And so then the next change, if we think about working through the tax return, you have the income you make and then you have the income that the IRS allows you to recognize. Well, then you actually have the tax computation. How are they calculating what you owe? And one of the again significant things that has been talked about is whether or not tax brackets are going to change. And as a reminder, the brackets did change with the 2017 legislation. And if that legislation is allowed to phase out, they will revert back to the rates that were in place prior. But if the new legislation passes, it’s going to lock the current rates in. And what that means is that the highest marginal tax bracket’s going to be capped at 37% as opposed to 39.6%. But even inside of how they expand the tax brackets, there’s going to be a change each year.

Brian: Yeah. I mean, this is the one if you take into account the standard deduction and the tax brackets. This is the one that’s going to capture the majority of taxpayers. Plus, we’ll get into credits in a minute with the child tax credit. But this is the stuff once again. It’s the theme of this legislation is to make this stuff permanent if they actually make this happen.

Bo: And so now we’re going to move to the last section. So it’s income that you make, it’s deductions, it’s then how you calculate it, and the last thing is how you actually reduce your tax bill. And one of the most significant tax credits that a lot of American families are able to take advantage of is the child tax credit. And there is some proposed legislation inside of the bill suggesting that there will be a change to the child tax credit.

Brian: Yeah, this was, child tax credit, you know, is pretty much been doubled. I mean, you can see if it phases out, it goes back to $1,000. It’s currently been $2,000. Now, once again, under the new bill or the proposed bill, there is a sweetener in there that’s going to phase out in 2028, but the overarching theme for long term is just to make the doubling of the child tax credit permanent. You know, and I thought that the other interesting thing if this legislation passes, it is going to make these child tax credits now index for inflation after 2028 once they lose that sweetener on there. But I think a lot of taxpayers, this impacts a lot of your taxes. If you have kids, you know what a big deal this is because credits are different than deductions is that these are not you get a deduction, you know, and say a deduction gives you 30% off or even 50% off, you still pay taxes on the other 50% or the 70% depend upon what the deduction and your tax rate is. A credit is a dollar for dollar reduction in your taxes. So, these things are actually bigger impacts on how much in taxes you pay because that’s a literal $2,000 reduction in the taxes you pay. So, you can imagine if you’re a parent, this is something you’ll want to pay attention to.

Bo: So, what should you change? How should you alter your financial plan today? Well, realistically, it might be a little premature because again, we don’t know what the final legislation is going to have in it. But we do want you to be aware that these are the areas that are most likely to be impacted. So if you are someone who would be impacted in one of these areas, we just want you to pay attention. We want you to recognize that changes could be coming down the pipe and we want you to be prepared for them so that you can either plan for them or position yourself in such a way that you can take advantage of them.

Brian: Don’t worry, we’re going to give you the full details and I mean get all into the nuts and bolts of this once we actually know what the real consolidated bill from both the Senate and the House. We’ve only got the House to this point. That’s where we’ll be able to talk about the tax on tips, the Social Security. How about these savings accounts? I mean, that we’re talking about putting $1,000 for all newborns. I mean, it’s almost like somebody woke up. I don’t I’m not getting into the policy idea, but it is one of those things where if you go to moneyguy.com/resources, we do have a resource on how powerful is your army of dollars, is essentially a wealth builder by any age and for a newborn you only I mean if you look at how much you have to put in there every dollar you put in for a newborn is 647 times you know that’s incredible. It’s pretty powerful stuff if they did. But I’ve never realized I’ve lived long enough through politics that you remember how it was under I think President George W. Bush that they talked about turning a portion of social security into private industry and index funds. So that might be something that we’ll it remains to be seen on what actually comes out. A lot of it is conjecture until we get the actual consolidated bill.

Bo: But we love that we get to speak into this stuff. We love that we get to stay abreast of what’s going on out there in the financial markets and hopefully communicate it in a way to you that’s easily to digest, that’s easy to understand. And we love that we even get to do that when it comes to what’s going on in your personal life. It’s why every single Tuesday at 10 a.m. we are here live answering your questions. So, if you have a question you want us to answer, something you want us to weigh in on, make sure you get it in the chat right now because I have the team out in the wings collecting your questions because we believe that there’s a better way to do money.

Bo: So, with that, creative director Rebie, I’m going to throw it over to you.

Rebie: Yeah, I’m going to kick us off with Garrett’s question. You talked about this in your most recent making a millionaire episode. Thanks for watching that by the way. The rule of thumb for saving for your next home is to not put extra money towards your mortgage. Can you elaborate? P.S. Awesome episode. So, can you guys elaborate on what to think about when you’re saving for your second home and whether or not you should put extra money on your current mortgage?

Brian: Well, let me I’ll let you give some additional nuts and bolts, but the most recent making a millionaire was a couple that was 25 years of age. And they made the mistake that I see debt crusaders do all the time is that, you know, you’re so used to getting you come out of school with whether it’s student loan debt or you immediately run out and get some credit card debt. And so we help people learn how to overcome some of those high interest debts, but then it feels so good when you vanquish that bad debt that a lot of times young people will then get, you know, they’ll get excited about how good it felt to pay off that credit card that they’ll start paying off a mortgage. And I’m always like, I love paying off a mortgage. I want you to be completely debt free. But there’s a time and a place because when you’re 25 years of age, I mean, the wealth multiplier, and I’ve got it right here in front of me, for a 25-year-old is 45, 44 times over. So, you can quickly realize, if you want to know yours, go to moneyguy.com/resources. We you can pull up your age as well, and it just bothers me when somebody is not funding their Roth IRA, who is not saving and investing 20 to 25% of their gross income and is immediately trying to pay down a mortgage debt. You have to get it’s more of the make wealth before you get to maintain wealth behaviors. And that’s the thing the mistake that we got on to them about.

Bo: And I think one of the things that Garrett because I remember and by the way if you haven’t checked out Making a Millionaire, make sure you go check that out. If you’ve not subscribed, make sure you subscribe so you know when we put brand new episodes out. I think one of the questions or one of the ways that Garrett it says, “Okay, I’m planning for the next home, right? And so should I just begin prepaying that mortgage because essentially I’m going to lower that debt and then when I sell that house, I’m going to roll it into this next house.” And while that sounds good in theory, one of the reasons we don’t love prepaying mortgages early is because especially if you’re going to make a big life change like buying another house, moving to a different community, moving to a different part of town, it gives you maximum flexibility when you save that money outside of your mortgage. Once you put money into the house, once you have money on that mortgage, it’s kind of locked in. Now, sure, you can do a refinance or do a home equity line, but we don’t love that. So, once you put it in there, it has served one purpose. It has now vanquished whatever that debt is you had in that mortgage to that extent. If instead you can put that and if this is a short-term thing, not something that’s like five, six, seven years out, but this is in the next two or three years and you can just save that money in a high yield account right now earning 3, 4%. Yeah, that might not be quite as high as your interest rate on your mortgage, but what it’s going to give you is flexibility. Because what happens if your house doesn’t sell as quickly as you thought it was going to? or what if there are additional moving costs that you weren’t prepared for that you need that liquidity for before you actually sell your other home. So that’s why we don’t love putting all of your eggs in prepaying that mortgage basket because sometimes you might need those eggs as the recipe changes.

Brian: Well, the contrarian wealth opportunity also is when you’re a young person, sometimes you have to make just like this couple, they had to move across to a different state for their career opportunities. And I can’t tell you how many of you who have come and done studio tours where you’re achievers. You’re so good at being financial mutants, you’re used to being rewarded for making it through all of your goals as fast as possible. And one of the first things I try to tell young people is deep breaths, slow it down. You don’t have to do everything as fast as possible. Don’t feel like you have to go buy a house when you’re 25 years old. Don’t feel like you have to, you know, do all these different things when you don’t have other components of your financial life figured out. I mean, I’ve shared before, I had an attorney in here, 25 years old also, who had gone out there and house hacked into like a duplex, but yet he felt like his career opportunities might be in a different state or a different city in the state. And I was like, look, that’s a problem. You’ve kind of got yourself in this pickle because you pushed a life decision a little too fast. The contrarian wealth building opportunity when you’re young like that is the additional flexibility. That’s why Bo is spot on sometimes building up even if it’s cash assets which seem like they’re underperforming that additional flexibility so you can focus on some of the key elements of your financial foundation of your success which is getting the job, the opportunity. So then you can let all the other puzzle pieces fall into place. Don’t force it. Because that’s what I see a lot of really smart people force it and lock themselves into things that’s much harder to unwind and get out of.

Bo: If you are someone who’s in the market and you’re thinking about buying a home, we have an entire home buying hub out at moneyguy.com. We have a home buying checklist to tell you the questions to answer before you purchase a home. We have the home buying calculator to help you figure out affordability. So, we have a plethora of resources out there because for most folks, buying a home is the single most expensive thing that you will ever spend money on. So, you want to make sure you make that decision the best that you can.

Brian: By the way, if y’all haven’t gone out there, just go to moneyguy.com/resources. You’ll see a drop down of ultimate guides. It’s kind of mind spinning how many ultimate guides. If you have any big decisions you’re trying to make financially, we probably have you covered.

Rebie: Yeah. Lots of topics out there. Moneyguy.com. Just click on resources and you’ll see all of that good stuff that we made for you.

Rebie: And another thing that we make for you are money tumblers. And that is today’s a tumbler day. It’s a tumbler day. And so since we answered Garrett’s question on the show, we would love to send you a tumbler, Garrett. Just email [email protected] and we will work on getting that sent. And we’re even using them in two different forms. I’m using mine as the koozie. I’m using mine as the tumbler. Great. What a great example. Look at that. Just I love that.

Brian: Do you think that when you announce it’s tumbler day, do you think the volume of questions increases or do you think it’s pretty standard throughout?

Rebie: I will say our people like to talk personal finance. So you think we get a bunch of questions either way?

Brian: I think so. Awesome. But I mean, prove me wrong. Let’s bring on the questions. You might win a tumbler.

Rebie: All right. Donald writes, “Hi guys, I’m 31 and my employer has a 401(k) match at 50% up to the legal limit, which is $23,500.” I know that’s pretty good. He says, “I’m currently maxing this out, but I do not have a fully funded emergency fund. Would you recommend reallocating?”

Brian: Yeah, I mean, you got to have an emergency. I mean, well, I mean, that’s oh, god. See, that’s because he’s you can’t say it too fast. You see, hey, he put, look at Donald. So, look, he put leaves over that trap and he almost just walked right over. I mean, Donald brings up a solid point is most people, you know, you’re capped once you put in 3%, 4%, 6%. I mean, this is what we see. Donald has this unique thing where his employer is just so generous offering essentially a $12,000 benefit if you can put $23,500 into it. It is hard to get away from that, but and I don’t I’m not rewriting millionaire mission, but this is one of those things where I think you have to figure out the balance. If you can’t fill up that emergency reserve naturally within the next four to six months, you’re going to have to figure out because you’re running a risk that if you had a life emergency, I mean, you don’t want to take I mean, do you do a loan at that point? I mean, if they make that option, I mean, it’s a pickle of a situation.

Bo: Yeah. I’ll tell you what I if I said to you, Donald, hey, I got a bag of money sitting in my office, you just got to come get it. You’d come get it. But then if I was like, “Hey, I’m going to put like a 30-inch box and you got to jump over that box to come get this money. Would you do it?” You’d probably still come get it. I said, “Okay, well, I’m going to put a 30-inch box and then I’m going to like dig a hole and you got to jump over the…” What I’m getting at is there’s a lot of things that you would be willing to do to get to that free money. I think that this is no different because here’s what I don’t want to say. I don’t want to tell you not to go get that free money, not to take advantage of that 50% match, but you have to have an emergency fund. Like, it’s just it’s a non-negotiable. It’s something that has to be there because all the savings in the world doesn’t benefit you if you have a catastrophe that literally takes your financial life just off the rails. So, I would figure out how creative can I be? Can I eat, and again, I’m not advocating for this because it’s a horrible health decision, but historically Publix sells cereal for two boxes for $5. Can I eat cereal for every meal for a little while?

Brian: You can do peanut butter and jelly, too, by the way.

Bo: Can I not eat out? Can I, you know, can I cut out my subscription? What things can I do to get my living expenses absolutely as low as possible so that I can still take advantage of getting that full 50% and get the emergency fund? Because here’s what I’m going to tell you. If you can’t at least get the emergency fund built up, I think you’re just living way too far out, too much risk, because even though you’re putting that money into the retirement plan, even though you’re technically following, we hold that thing up because we have a nine-step tried-and-true process, even though you’re following the financial order of operations, you’re doing step two, you are now captivating those dollars in such a way that you cannot get to them. You have to have something to at least be able to get you out of that pickle. So, I would figure out how can I get my expenses absolutely as low as possible so that way I can do both. And then once you have that emergency fund fully funded, then you can breathe a sigh of relief and know you’re in a great spot letting those dollars continue to work for you.

Rebie: What if he can’t cut expenses anymore? Because like that’s a lot of money because he could just do a very short amount of time where he pulls back from the 401(k) slightly but doesn’t miss out. Like when is that a good option?

Bo: Yeah. So again, you cut off the again, you have all year most plans. Now, some plans work this way where you have to in order to get the employer match, you have to contribute each pay cycle. But some have what’s called a true-up provision where even if I don’t contribute each pay cycle, so long as I get X dollars in by 12/31, I’ll qualify for that match. So maybe, you know, you’re someone who’s a December bonus payer, right? Like I get a year-end bonus, it’s going to be whatever. Okay, I might decrease my 401(k) contribution right now so that I can fill up that emergency fund bucket, but then when my bonus comes in or at the end of the year, I at some point if you want to be able to do both, if you want to be able to get both of them done, you’re going to have to make the hard decisions where you like cut down to the quick. But man, 50% free money.

Brian: Well, you bring up a good point. I mean, if you have year-end bonuses, a lot of times your employer will let you be creative on that bonus payment versus your normal pay. I’ve done that for employees when they tell me that they want to go and allocate more to the 401(k). I’ll make exceptions for them because I want to encourage that financial mutant behavior. So, but you got to I completely agree with you, Bo. You got to get the emergency fund. The ideal is to figure out a creative way so you get to do both. And maybe you play the way you squeeze the balloon on making that happen is play with the timing of the way the cash flow comes in. Maybe you dial down temporarily now, but then you catch it back up with year-end bonuses or other things that are coming down the pipe because I got to think an employer that’s doing that type of funding, this is probably a high-skilled career where part of this is golden handcuffs, but part of this is because it’s a very profitable industry and I bet there’s some opportunities to get the best of both worlds.

Bo: I’m just thinking of if expenses are so low because I’m I’m like if I were in this situation, what would Bo Hanson do? Like how would honestly because once you fill up your emergency fund, you’re done. It’s not like something has to continue. You’re going to keep funding, saving in your 401(k). Hopefully, you do this over and over and over and over again. I’m sitting here thinking, man, I might go drive Uber. I might go pick up a side gig. I might find something on nights and weekends just to satisfy this one goal so I don’t miss out on so unique. 50% on that money is pretty powerful.

Brian: It’s insane. I mean, it’s that’s an unbelievable match. I would figure out what creative thing could I think we gave Donald enough whether it’s a cash flow management and timing issue or it’s side hustling. We’ve thrown enough breadcrumbs out there that I bet Donald’s going to come back and there are ways to do both.

Bo: That’s right. And both are important. Both are important.

Rebie: No, I loved what you guys were saying. I think there was just a piece of me since I am a proud member of the messy middle. I’m like if Donald’s single then yeah, but what if he’s like married with three kids? Like that just changes the conversation. So like what other levers can you pull? So that was a great answer.

Bo: Every financial decision we make has an opportunity cost right there. There is a cost associated with any decision we make no matter what decision that is. And as well personal finance is very very personal. And his personal situation he’s going to figure out which one of these things is actually possible and plausible for me to be able to execute.

Brian: And you look you don’t have to get it perfect. I mean look I’ve written the book on all the mistakes you can make and still end up in a pretty good place.

Bo: That’s right. Love it.

Rebie: All right, Donald, since we answered your question, just email [email protected] if you would like a Money Guy tumbler. I was like, thank you.

Brian: And by the way, kudos to you because I’m sitting here, I’m like, wow, I’m such a financial mutant. I was like, how can we get him that 50% guaranteed rate of return? No, I respect that. But man, oh man, we got to respect having that emergency reserve so you don’t make desperate decisions.

Rebie: Yeah, for sure. 50%. Woo.

Brian: Okay, go hug your employer today. Oh, well, let’s don’t I mean, maybe I mean 50, I like to think we’re generous around here with our 8%, but I mean that’s a pretty incredible benefit that that employer’s offering. That’s awesome. Hug your employer. I didn’t say kiss.

Bo: You know what? Hey, let’s just side hug. Let’s high five. Side hug.

Brian: Okay. Fist bump. I’m not even a hugger. I know that’s the hug that he’s recommending. The employees just came. I don’t know what happened in my childhood. I don’t like to hug.

Brian: I think who’s a hugger if y’all were curious.

Bo: I am. It’s true. You know what? At the office, at the office, I high five. That’s what I do.

Brian: Oh, because you’re the employer.

Bo: That’s right. That’s right. I agree with that. Smart choice.

Rebie: All right. Ready for the next question? Still Mutating has a question for you. I like that. I like it. And in light of his question, I like it, too. It says, “My net worth is $450K and it’s all tied up in our SoCal home. We have $15K in credit card debt at 19.75%.” I know. I hate that. Should we use a HELOC at 6.75% to pay the credit card off? He’s still mutating. So, what should he do to get himself back on track?

Brian: I mean, we don’t look, this is one of those things we’re going to have to paint by the numbers a little bit. We don’t have enough variables. I’d love to know what his emergency reserves are. I’d love to know does he have a health savings account? I mean, we just we don’t have enough variables to know what all sources he could go pull this money out of. But I will say I don’t like 19.75% on a credit card. That’s why it’s step three of the financial order of operations is because if that’s twice the rate of return you’re hoping to get in a good year, we’ve got an issue.

Bo: Yeah. But I think and this is some like general guidance that you should really really think about and this is something that you kind of we learn early on in like becoming a financial advisor. When you have not all debts are created equal, right? So you might be thinking about in terms of like interest rates and that sort of thing, but what I’m talking about is some debts are collateralized and backed by a thing and some debts are revolving and they’re not collateralized. So, one of the things you always want to be very very careful of is taking a non-secured debt, something that at the end of the day ultimately if you don’t pay it, it’s going to make your life tough and difficult, but they can’t come like take something away from you and replacing that debt with something that if you cannot make the payments on that, they can come take it. So, if you take a non-secured credit card and you pay it off using a home equity line and now all of a sudden you cannot pay off that home equity line, you cannot make payments, you go into default, well, now you’ve actually put your primary residence at risk, you’ve now put yourself in a situation where literally your very home is now on the table for this debt that you’ve incurred. So even though the interest rates are there, there’s a huge arbitrage situation there, you have to factor in the total risk. If I take out this HELOC, I am now taking debt and I’m putting my house up on this debt. And that’s just an aggressive…

Brian: Well there’s also aggressive too much of the easy button and the behavioral issue might not have been addressed is that if you have you have this house that’s obviously driving your entire net worth success and we know you can’t eat a house. I mean, you have to go take down debt exactly what you’re considering. And that’s the easy button because you’ve obviously there’s some behavior going on in the background that’s run up a credit card debt at this level. If you immediately hit the easy button and go do this home equity line, I’m worried. And look, I’ve fallen into this trap. You know, and I know I’ve talked about it earlier, but in Millionaire Mission, I talk about my access to cash trap where I had a home equity line because I had a house with multiple, well I had over six figures of equity and I did this I went and did the home equity line and what’s funny is that we did a we were doing some show research and I went and pulled all those old statements and I found out that you know it started off as such a just benign simple thing is like kind of like your situation whereas you know it just seemed like a no-brainer. The banks were giving away free home equity lines. They were doing prime minus a half at the time so the interest rates were super low. By the way, home equity line interest rates right now are not, well 7% it’s still not great, but it’s better than 19%. But what I found in my own behavior is that it was too easy. They gave me a credit card. They gave me a checkbook and what it all of a sudden became the easy way instead of making the hard discipline decisions of life to maybe this month I need to budget better and actually restrict where I was spending money. It just seems so easy to just go transfer it from the home equity line. So I worry, still mutating, if we gave you the easy button before you address the behavioral and the discipline issues, we might actually be giving you a path that actually digs you this hole deeper instead of getting you out. So, I would first before you go do something like a home equity line that first of all has friction costs, but also all those security and risk factors that Bo talked about with you. This is the house that you live in and do you want to put that in jeopardy? Have you gone through the exercise of looking at your budget to figure out, hey, can I cut subscriptions? Can I go do the $200 bucks with a few phone calls type endeavor, you know, exercise that I have in Millionaire Mission? Are there other things I could do that could help me accomplish this before I just go and let this home equity line be the solution and the solve all for this moment in time?

Bo: The other thing I think and when you hear these stories of people that paid off a tremendous amount of debt and you ask them, “How’d you do it?” A lot of it is like, “Hey, I budgeted it. I cut down my expenses. We lived on this.” Another thing that people do and this is like a painful thing to do, but it’s a really healthy thing to put you in the situation never do this again, is start selling stuff. Hey, are there things, are there assets that I own in my house? Are there things that I’ve spent money on previously that I might be able to go round them up and hey, I you know, I don’t use this thing anymore. I’m going to I’m going to sell my PS4. I’m going to sell my whatever this thing is. I’m going to get rid of I’m going to sell the car and I’m going to get rid of the car payment and I’m going to buy a less expensive car and I’m going to take that difference and I’m going to go extinguish this debt. You might need to make some really extreme decisions like that before you start taking again like hitting the easy button and just say, “Oh, well, I’m just going to replace this one debt with another debt.” You haven’t really addressed the problem.

Brian: No pain, no gain. Look at that. That’s not mine.

Rebie: No pain, no gain. Brian Preston. On that note, still mutating.

Bo: Great question. Keep up the mutating. Benjamin Franklin like I think Nick, that was Benjamin Franklin that said that, right?

Rebie: Sure, sure.

Rebie: Sure. Well, hey, Still Mutating. If you would like a Money Guy tumbler, we appreciate you being here and asking your question. Just email [email protected] and we’ll send one out to you as a thank you. All right, Ruben F has a question next. How should teachers think of the recent 401(k) by age episode? 10% of my salary goes to the pension. It’s vested. I have $36K in my 403(b), maxing out my Roth IRA with a 21.5% savings rate without the pension and I’m on step seven. So, it sounds like he’s got a lot of good things going on, but I think this is a good kind of nuance to… We talk a lot about the power of the 401(k), but he’s a teacher.

Bo: Ruben’s asking for somebody else because Ruben’s crushing it, right? Like how should I think about my Ruben, you’re killing it. You don’t think about it at all because you are literally knocking it.

Brian: But I see what Ruben’s asking is because we, you know, we talk about you don’t count employer contributions if your income for a single individual is over $100,000 and for a married couple over $200,000 because you get over that social safety net and more of the discipline when you actually start go to use these assets falls on your shoulders. So that’s why we even have this caveat out there. Well, and teachers typically don’t make a ton of money. So but Ruben, you’re proving the point that there’s categories of people by occupation that typically do really well at becoming millionaire status. As a matter of fact, I’m recording a mini show today and I threw a little caveat in there and winked at the teachers because y’all, a lot of you do show this high discipline function with savings and becoming millionaire status with lower incomes. So kudos to that. But to answer your question, I don’t mind people counting that 10% because there might be another teacher out there who is unfortunately not able to save 21% in addition to the 10% that they are forced to take out of their pay. Because realize here’s the other part of Ruben’s thing is when your employer makes you take 10% out for your pension, what the other part is they’re probably putting in at least 10% if not even 15% on top of that as well. You get to count a lot of that and because teachers we often say this is that pensions don’t show up on your net worth statement unless they have an option to where you actually can roll the money out into an IRA later. So you’re going to have both those options typically and usually the pensions coming from government institutions like education are some of the most lucrative out there. So without a doubt, you know, you can count that in your savings rate. But Ruben, I like your ability because teachers, the other cool thing about teachers is they typically hit 30 years so fast that a lot of them retire in their mid-50s, early to mid-50s. The more you save when you’re younger, as long as you’re not sacrificing memories, is going to give you additional flexibility to live that great big beautiful tomorrow moment that I know you’re building for.

Bo: That was what I say. I love that the 21.5% in addition to the pension is really just giving you more options down the road. I don’t know how old Ruben you are, but likely if you’re doing this for a majority of your career, you’re going to be at a place where you get to write your ticket much earlier in life than a lot of other folks because you have that wind at your back with the pension. So, I love it. I think flexibility is on your side and I think you’re thinking about it great.

Brian: Look, I young people, I know you’re typically without resources. You don’t have money, but your time is so valuable. Do you know how dynamic it is for a young person that is disciplined? Because you take this element that’s why we spend so much time talking about the wealth multiplier is because I get, you know, you don’t have much money, but a little goes a long way. So every little bit, as long as you’re not sacrificing memories, I don’t want your 50-year-old self to be wealthy, but go, man, why did you waste your 20s? Why did you squander your 30s? But if you feel like you’re living your best life, but you still have this discipline function where you’re able to save, knock it out. Because I will tell you some of my best I feel like some of the best success moments I’ve had in my life now that I am post 50 is that I can’t tell you which dollars I saved have turned into this. But I’m so glad because I was at that element when I was in my 20s that I was going to save so dynamically so that I could retire at 50. And then I get to 50 and I’m like there’s no way I’m retiring. I love doing what I do. I feel purposeful when I wake up. But I realized that all those decisions were the culmination of why we get to do crazy stuff like buy more equipment and all this other stuff is because it doesn’t have to be tied to does it generate money is because the why became the flexibility gives us options to do things an unorthodox way. Love it.

Rebie: I love it too. Well, Ruben, thank you for the question. We’re really glad you are here.

Brian: Do you know how hard it was for me not to pop that thing? No. No. It was sitting here. I came really close, but I was like, “We don’t pull the same trick twice.” I do it all the time, by the way.

Rebie: Does everyone actually hear it when Bo puts it over here? And I bet they heard it. You held it pretty far away from your mic. I don’t know. Let us know. I’m curious now because we always notice it.

Brian: Thank you for not doing it while I’m in mid-sentence. That is not always the case.

Bo: You taught me my lesson last week. It was sitting right here, too. But that was good. I mean, I did it way over here. I mean, whatever.

Rebie: Oh, I was going to give Ruben a tumbler. That’s what I was going to do. Ruben, email [email protected]. We’d love to send you a tumbler since we answered your question on the show. All right. Ready for the next one?

Brian: Indeed.

Rebie: Leah writes, “My husband and I, we’re 31, are over the income limit for Roths. Our account structure isn’t ideal for backdoor. Aside from HSA, is there another way to fill that bucket? It feels like we’re missing out.”

Bo: So, is there another way to get money in Roth? Yeah, sure. I mean, one of the ways that a lot of people get money into Roth is they can do Roth 401(k) or Roth 403(b) contributions. A lot of people don’t realize that for most retirement plans, you have two different ways. Well, actually three, but two that most people know. You can do a pre-tax contribution where you get a tax deduction this year. When you pull the money out in retirement, you pay tax on it. Or you do a Roth contribution. You put the money in, you don’t get a tax deduction this year, but it grows tax-free, assuming when you distribute it, that’s a qualified distribution. So, yeah, you could do Roth 401(k) or Roth 403(b) contributions. But if you’re someone who is in a high enough tax bracket that you’re now above the ability to even do direct Roth contributions, I’m going to bet that that pre-tax benefit of putting pre-tax contributions in your 401(k) or 403(b) or 457 is pretty valuable. And so it’s probably still going to make sense to do pre-tax. Well, a lot of people find themselves in this situation. And I’d be curious to know why your account structure doesn’t lend itself to that because maybe you have, for you have retirement plans, but maybe they’re not good. Maybe they’re really really expensive and very limited investment options and they’re just not awesome. So, it doesn’t justify moving IRA assets into those plans. Well, if that’s the case, then right now do the best you can, the best that you can and continue to build money on a pre-tax way and then continue to think about building money in an after tax way if you don’t have any other tax-free options. And likely if you’re only 31 right now, later on at some point in your life, you’re going to have an opportunity to start building Roth assets. Whether that be through job changes where you get access to a better 401(k) and then you can start doing backdoors or maybe you retire before traditional retirement age and you’re able to start doing Roth conversions just like we did a making a millionaire episode walking through what that could look like and how even Roth conversions in your 50s and 60s can lead to like millions of extra dollars in retirement if you think about it well. So just because you can’t do it today doesn’t mean that you’ll never going to be able to do it. Agree? Disagree.

Brian: I think you nailed it. And that’s why I’ll just close it out with the quick checklist for homework is just go once again look at the structures of your employer plans because obviously the way you since you said it’s not you can’t do backdoor that means you have an IRA, rollover some assets and you’ve decided you shouldn’t roll that into your 401(k). Make sure you go through that exercise again because maybe you misunderstood, you didn’t realize because if you work for a Fortune 500 company or a big company that has just like we’re a small company. We have a great 401(k). Just once again, go look and figure out why you’re not rolling those assets into 401(k) so that they’re gone. And then if you look at it and it just doesn’t work out, then I would ask yourself, y’all need to make look at lifetime planning things like, hey, we live in a state where there’s a very high state income tax plus our federal tax bracket. Our marginal rate is at this level. We’re crazy not to take this tax deduction right now. But then ask yourself, hey, are we going to retire in this state? Because if we’re not going to retire in this state and you know, we’re saving so diligently now. Maybe we’re going to go from this high tax state to a low tax state in retirement. There’s probably going to be some unique, you know, arbitrage situations where you’re going to have Roth conversions as well as be tax smart. But I would I always like having the plan so you can think about those things now, daydream, figure out a path forward. And then I think you’ll be in a great place because you know and that also gives you the dynamic if you look at it you can figure out use that decision matrix that you just did to figure out should all this go to traditional because of our tax rate or maybe this means that because we maybe you’re in a low income tax state and you’re barely over 30% or maybe you’re 28% on your marginal rates and you say well maybe we should do money to Roth because we’re so young, too. So, it at least gives you the decision guidelines and variables so you can start making the better path forward choices for yourself.

Rebie: Love it. That’s great.

Rebie: Leah, thank you for the question. Just email [email protected] if you would like a Money Guy tumbler.

Brian: It’s Leah right? Hey, it’s fun to clarify what God doesn’t give you, you know, he gives you something else. If you saw my SATs, you know why I say that. Very good at math.

Rebie: You guys are funny. We got lots of comments saying they hear the can opening loud and clear, just in case anybody was wondering. There is no question about it. Somebody even said it was part of the show now.

Bo: Oh, don’t encourage that. Quick poll there. Quick poll there, Nick. Do you like the can opening or do you not like the rude ask is it do y’all consider it rude that Bo answers it in mid conversation? He opens it while you’re talking.

Bo: You know what I’m going to start doing? I’m going to start doing it like right like while he’s talking, literally have a fist fight.

Brian: And remember, you only get to hit me once, buddy.

Bo: All these comments I’ve been getting lately, I don’t think I want the smoke. I don’t think I want the smoke anymore.

Brian: This is like me on a golf course. I look like I can golf, but I don’t know how to golf.

Bo: Benjamin Button, aging backwards. I don’t want that.

Brian: I’m putting my money on Bo if we got in a fight.

Bo: No, not a chance. I don’t know. It’s not as clear anymore. It used to be, but not anymore.

Brian: I do. You know what’s funny is I have my next door neighbor is Bo’s age, and he’s super successful, too. And I try to humble Bo by bringing him when I came to work and I said, you know, my next door neighbor is doing jiu-jitsu now. And I was like, when are you going to start? And he hasn’t taken up.

Bo: I don’t like, I never like wrestling and all that kind of stuff. It was just never my thing. I was always like the sports that I did were always like ball sports, right? So like baseball, like that kind of stuff and swimming, avid swimmer very much so. And but like the thought of someone like elbow me in the face I just I don’t like that.

Brian: Oh he does. I mean, I’ve seen black eyes. And the last time I saw him, his toes looked horrible. Yeah. Like it is, but he loves it.

Bo: I think it’s awesome. And people that do jiu-jitsu, I think it’s a super super cool thing and they love it. I just recognize probably not for me.

Brian: By all those things that I mentioned, when you do get injuries, it’s not like the people are super aggressive. It’s just that when you’re in close quarters, you catch elbows, you catch other things. I have no desire. I just like hanging out with people who can defend themselves. That’s my strategy on most things in life is I just put myself in proximity to others who can do the things that I’m not. Remember I’ve done one of the well I shouldn’t say it was one of the more popular shows. One of the shows I’m more proud of was I used to do a historic show on financial mistakes you hope your friends make. Yeah. And but it did okay. But I always like if you could find a friend that buys not just a boat but a lake house. I mean those are great friends to have because you just…Yeah. If you know, go get a friend. RVs. I mean, these are great things you hope your friends do so that you can go get the benefit without.

Bo: So, you’re saying jiu-jitsu is one of those things. You hope your friends do?

Bo: Yeah. I mean, I would say I would put jiu-jitsu in that category because then you feel very confident that your friend could defend you, but you don’t have to go do all the exercise and work that goes with that. I mean, do you have any desire to do jiu-jitsu?

Brian: I’m too old. I’d be I’m always worried at this age. I’m in decent enough shape. I worry about injuries. Yeah. So that’s why I pick on you all the time when you’re doing all that heavy Olympic lifts. I’m like, Bo, you’re getting to the age. Nah, be careful. It’s the injury that gets you. It’s not you’re in great shape, but it’s the injury that you have to worry about. That’s I get it. There’s some life advice for all my 40, 50-somethings. You know what I’m talking about. No, you mess up your knees. You mess up your ankles. No, it is true. How many people do we know that are successful have back problems and the pain is a legit issue as they get older.

Bo: To put your mind at ease. I try to put myself in position when I don’t do the crazy stuff anymore. Like I think I keep it very much inside the realm.

Brian: Did y’all not hear him talking about throwing around 100 pound dumbbells this morning in the team meeting, in the content meeting? Sounded when I heard 100 pound dumbbells I was like he’s not smart yet. He’s not smart yet.

Bo: Someday. Still working. Still mutating over here. Still mutating.

Rebie: All right. Ready for another personal finance question? Yeah. Before we have zero people watching the show. Well, this one is from Michael C. It says, “How do I determine the right down payment? Do I buy once I hit 5% versus continuing to save? I plan to stay in this area for the long run. Thank you.” And something I appreciate about the money guy is that you guys give some flexibility, right? On that first home purchase, you could put 5% down and still do it in a smart way, but is that always the smart way?

Brian: I mean, look, the 5% is meant to I mean, the ideal is still 20%. Let’s never forget that. That is the ideal, but I just know that if you go like some of the other financial gurus, which by the way, I kind of I smile as a lot of them have changed that update is because I was like, we never had to change our rules. We’ve always been super flexible on this, but it is the ideal is 20% just because you avoid PMI. It allows the likelihood that you’re keeping that you’re getting a nicer house and still respecting the 25% of what your expenses are. So I consider it a balancing act. If you’ve had to forego saving and investing 20 to 25% for the future because you were saving up to get to this 5%, the 5% now allows you to still make sure you’re getting the Roth, you’re getting to do your 401(k). But if you find out that you’re already doing 25% and you’d like to now go to a nicer house, but you’re going to be putting in jeopardy that 25% towards housing, then yeah, let’s put a bigger down payment down.

Bo: Yeah, I think that’s the answer is how do I know when the down payment’s right when I’ve done the mathematics to recognize that whatever the mortgage is based on my down payment, I’m going to stay below that 25% threshold. That’s the thing most people when they make this decision, it’s less about like, well, how much do I want to put down? It’s how much is necessary so I make sure the house is inside the realm of affordability. Okay, if I do 20%, my mortgage is going to be less. I’m not going to have PMI, there’s these other costs I’m not going to incur. Or man, if I try to wait for 20%, the house prices in my area, they just keep going up and up and up and up and I’m at 5% right now, but if I wait till 20%, the house is literally running away from me more quickly than I can catch up to it. This is where personal finance is so personal. You have to determine for you and your situation, what’s the best answer? What’s the best scenario? And a lot of times, it’s not just you. It can also be your area. But we happen to live in an area where home prices just continue to move further and further and further and further and further away. So a lot of people even though they would desire they want to put down 10%, 15%, 20%. They’re having to make the decision so long as it still is in the 25% to put down less just so they can get on that side of home ownership because they know that they want to be here. They know that they have they’re going to be here for at least five to seven years. They know that their vocation is secure. They’re doing it just so they can stop that train from moving away from them. You have to assess in your circumstances what’s the best decision based on the goals that I’m trying to achieve.

Rebie: I like that. I love it.

Rebie: Michael C, great question. Thank you for asking it. Just email [email protected] if you would like a Money Guy tumbler. 83% say yes. They like it when Bo pops open the can of sparkling water.

Bo: You know what I don’t even do it on purpose. It literally I just this is what I like to say in polling. You have to be careful with how the question was answered.

Brian: Oh, we if we asked do y’all consider it rude that Bo opens this in the middle of Brian speaking.

Rebie: I’d like to know how that I would also because this was from our YouTube live stream. I’m also curious what the audio podcast listeners would say because we also release this on audio. Interesting. And if you can’t see it, how do they think it’s funny, too? I don’t know.

Bo: To be clear, I did it. I would love to know. You can comment down below. And she has not said that it was rude at all. Not even bringing it up.

Brian: I mean, I’m just here’s a personality issue. I’m the same person. If you eat macaroni and cheese around me, it bothers me. Those smacking sounds. Don’t y’all hear people chewing? So, it’s even I thought he had a problem I’m not going to give too many clues. Other foods that can make because these are people we socialize with all the time. But there are certain people that it’s hard to be around them when they’re eating because they just they chew with their mouth open and it bothers me.

Bo: I do I do not disagree with that. That bothers me. But you’re saying so the can popping for me is the equivalent of eating with…

Brian: I’m an open book to you guys. I tell you how it is and I just some people fortunately I will tell you everybody in this room I eat around you all the time. Nobody here is a weird. I literally was like, “Okay, here’s dude in this room.” So nervous. It’s more of somebody in my orbit in life that when my wife says, “We’re going out with so and so.” I’m like, “Oh, please don’t put me across the table from him.” Wow. We really have those conversations.

Bo: All right. Well, you don’t eat mac and cheese in front of Brian.

Brian: No. I say that because in college I had a roommate and every time he would eat macaroni and cheese and I could be in the room trying to study or something and I hear him over there just smacking going to town and I was like there’s something not right about this.

Bo: I for the record I don’t eat cereal anymore but when I did I ate it very quietly with my mouth closed. So I was a very clean eater.

Brian: You’re a clean eater. Yeah. I’ve never noticed you eating.

Rebie: What a compliment.

Brian: When I and I don’t think I’m that odd in that. I mean I just think that some people they just I don’t know. Some people have weird in that. I mean, does that make me weird?

Rebie: I think it just depends on the person. I don’t like my fingers being messy. It’s like just a thing, right? This is my wife. I do not. So, like if I’m ever out like if I’m out on like a double date or whatever, like I will not get hot wings. I will not get ribs.

Bo: No, I’ve seen you eat wings because we’re practically family, right? Like it’s different. But if I’m out with people that like I would not eat that around folks that are not like inner circle because I don’t…

Brian: Okay, I’m willing to put an asterisk next to everything I just said about wings. I think me and my family go eat wings. I’m counting on us all to be a little gross while we eat. So, it doesn’t matter if you eat mac and cheese one way, you’re out. But that type of food, it’s okay that you’re getting in it because the food is that good.

Rebie: What about spaghetti? Possibly. Spaghetti specifically.

Brian: What’s funny is we went to this awesome restaurant that had a James Beard award. We didn’t even know, stumbled into this place. This was this past weekend. Yeah. Down in Winter Park and so you know it was a noodle bowl. Okay. So I think you’re supposed to make some noise when you eat a noodle bowl with broth and all the other stuff.

Bo: I don’t supposed to seems aggressive. I don’t know that you’re supposed to make a noise.

Rebie: Huh? It’s polite. Yeah. See is like enough that kind of I know where you’re from. You don’t know the answer. It’s polite to make a noise when you eat noodles. Yeah. In a culture. That’s what we’re saying for like Asian culture.

Bo: Know nothing tonight. Hey, you learned something new today. All right. Well, I know what I’m having for lunch today. We’re going to get a noodle bowl and I’m just going to be it’s going to be great.

Rebie: Have we exhausted that time? I think I’m ready to move on. Let’s go back to personal finance. The four people here really love that conversation. All right. John has a question for you. I’m 37 years old and my company was bought out and they paid out the ESOP shares. You say that ESOP, right? That’s right. Okay. I always second guess myself. The money was dispersed to a 401(k). Should I move that to a Roth IRA over 10 years slowly? The amount is over $250k.

Brian: This is totally it depends because it look this is the same you could ask this question. Should you do Roth conversions? We’d have to know what his income is, what the goal long term because the whole reason you do Roth conversions or you convert anything that’s pre-tax into Roth is really because you’re thinking about how you’re going to use this money in retirement and then you’re seeing if there’s a tax arbitrage opportunity because you have to make the choice, do I pay the taxes now or do I pay the taxes in the future? And if you think taxes are going to be higher in the future, then sometimes it makes sense to forego some opportunity costs of what this money could become because you’re paying the taxes now. But I would I mean 37 is still so young that the wealth multiplier for a 37-year-old is pretty strong. I mean it’s still 10, 10.1. So I mean every dollar you have is going to have a 10-fold multiple. Now, if you don’t if you have low taxes, that’s a for the Roth conversion because you could every dollar you put in there could have a 10-fold multiple with no taxes. But if you’re in a high tax situation, I would hate for you to lose 40% of that money to taxes. That’s really I just gave you the answer with the way I just went through that analysis.

Bo: What’s interesting to me is this is like one of those test questions where they throw stuff in there that doesn’t matter. The actual ESOP part of the question doesn’t matter. I recognize the reason you’re saying that is because the ESOP funds rolling into your 401(k) is something you can roll out even while you’re in service. It sounds like that’s the way that your plan was structured. So, you probably couldn’t do that with your other 401(k) assets. But for a 37-year-old, whether or not you should do Roth conversions is the real question you’re asking. And it’s exactly what Brian said. It kind of depends on your circumstance. And I would contend there’s probably a really good chance at 37 years old between now and the time that you hit 75 when your RMDs are going to start, you’re probably going to have a chance to do Roth conversions at some point. So I’d figure out based on my income now at 37 versus based on the income I think I’m going to have at 74, are there going to be some chances there that I’m going to be able to convert dollars to Roth at a lower tax bracket than I would be able to do them today? And if the answer is yes, then I’d probably wait to do that. I don’t think that it makes sense to accelerate that simply because you can right now.

Rebie: Great answer. Jon, thank you for being here. Thank you for asking your question. Just email [email protected] if you would like to cash in on your very own money tumbler/koozie.

Brian: I had one other thing I was going to share. I waited until the end of the show because I realized nobody came up to me at Epic Universe.

Bo: I can’t honestly I thought it was going to be after the first question.

Brian: Usually at Disney I usually have a few financial mutants that come up. Nobody at Epic Universe. People were asking about how was it? Give us the so, so I’m just assuming none of our audience goes to Epic, you know, Universal. They’re all Disney people. There’s no Universal people in there. But I will tell you guys, hat tip to Universal for being able to come up with because I think sometimes the whole realize there hasn’t been a new theme park like opened this century like I mean well you I mean it’s a lot of money. It’s billions of dollars. And I feel like even if you think about other parks that have opened, I mean still even now decades later they’re like a half a day park. Universal actually opened a brand new park that is a full day experience. I mean with multiple shows because they have a How to Train a Dragon show. They have a Harry Potter show. And then they had multiple thrill rides. It was impressive. I mean, I think we at the end of the night, we were trying to we, by the way, we got there because my family stayed in the Helios Hotel that night and so we got early park entry at 9:00 a.m. So, we got in the park about 8:45, 8:50 is when they released us to go in and we were there until after the park closed at 9 p.m. And it was a full experience that month.

Bo: So, you could do everything because you’re there all day. Like, is it something you could have done everything?

Brian: Now, and I’ll go ahead and tell you, and I think it’s money well spent, Universal, another thing that they do different than Disney is that you can do what’s called a VIP tour. That’s just an add-on to your normal ticket and it’s a few hundred, but if you know the pricing of doing a private VIP tour versus a group VIP tour, it is if your time’s worth a lot, it’s well worth it because that was the only way that you were because the Harry Potter ride Ministry of Magic 3 hours, four hours sometimes the queue. So, but if you did the VIP add-on, it was not a private tour. So, they don’t feed you and it’s only for a few hours. It you got on that ride immediately. They did that with so I thought it was well worth it. If I here’s some tips because that’s just the way my brain works.

Rebie: Here we go. Write this down.

Brian: If you stay at the Helios or I think any of probably I don’t know if it’s all the parks around there, all the hotels around there, you get in an hour early, take advantage of that because they, by the way, it scares you at first because they let everybody in the parks at 9:00. But they are doing a good job of making you show the hotel room key to actually get on the rides early. Because I remember I was like, “What the heck are they doing?” Because you see all these other people running around the park and you see them literally sprinting. They’re just trying to get in to get in line is all they’re trying to do. You actually get to go ride the rides. Set your VIP tour if you buy those tickets for a few hundred more, you’re a financial mutant, your time’s worth a lot for 10:00 a.m. and then you can you get to take advantage of the hour, go ride some rides first, then do the few hour excursion that they do. You’ll load it up. It’s pretty cool. That’s the hack. So, it was awesome. Recommend. Was definitely. Now I don’t know if we’re headed back because it’s still they don’t offer a season pass on Epic Universe yet. We even because we have Universal season tickets too and I couldn’t I was like when are you going and they’re like probably not in 2025. That’s nobody knows though. But it was epic. It’s well-named. And now look there’s no shade. I picked on my wife. She doesn’t watch this so it’s okay. She bought an umbrella to walk around with, you know, it’s specifically designed to keep the and it was brilliant, you know. So, I will tell you there is no shade hardly in Epic because all the trees are so young.

Rebie: Oh, like an umbrella for shade.

Brian: So, I would say do that. Do the personal advance because by the way, Florida right now is scalding hot. It is the face of the sun. It’s humid. It’s hot. So you need it actually was I thought it was a crazy thing for her to show up with it but it was actually and I had one of those fans around my neck that you charge somehow those things I don’t know how they work all day but they do and it just blows air on you all day. I look like a straight up tourist.

Bo: Fanny pack?

Brian: No fanny pack.

Bo: Cargo shorts?

Brian: I don’t do cargo. You know I have these everybody makes fun of me because I look I don’t get paid for this but they should pay us for this. During the summer, the licensed to train shorts from Lululemon are actually spectacular because they have zippers on the sides and on the back. So everything is zipped up so you can ride it on rides and they stretch out. Now you look like a complete bozo walking around with pockets that are, you know, protruding 8 inches all the way around you. But I do that. I can put sunglasses. I can put cameras. I can put anything in those pockets. During the winter, Vuori has some I can’t remember what those pants are but they have zippers. Just look for the Vuori jogger pants that have zippers on the sides and the back because that’s the problem with most athletic stuff is they don’t have enough zipper pockets. That’s the hack for theme park wear.

Bo: Vuori, Lululemon, if you’re looking for sponsorship opportunities, you can write info at money. I’m just kidding. Let’s go. Actually, you should support moneyguy.com. Thank you. Okay.

Rebie: Well, that was fantastic. We got some theme park advice. We really dug into how people feel about the can popping.

Bo: I can’t believe you held that to the end.

Brian: I didn’t want to run off. I mean, I knew I didn’t want to run off the audience for people who don’t care. You have to really be part of the money guy mutant family to want to know about theme park stuff with us.

Rebie: I love it. Fair enough. Well, I enjoyed it. I’m glad you had a great time. And we also did have a great time. Maybe not quite as epic, but also an epic time here today on the Money Guy Show. We’ll be back Tuesday 10 a.m. Central every week talking personal finance with you and trying to just help you feel a little more confident in your finances so you can focus on what really matters. Moneyguy.com is full of all of our episodes, all of our free resources that we made just for you. So, be sure to check that out to just dive a little bit deeper as you continue on your financial journey. Thank you for being here for real.

Brian: So you just said so you can focus on what truly matters. And I love that’s why I got to do the theme park because it was great family memories. And that’s why it’s just worth remembering that money is just a tool. It’s not the goal. So make sure you’re doing the why so you enjoy your 20s, your 30s, your 40s, your 50s, and live your best financial life. I’m your host, Brian Preston. Mr. Bo Hanson, Money Guy Team out.

Free Resources

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

Have you filed your taxes yet? You still have ample time left until the April 15th deadline, but it’s probably best not to procrastinate too...

Articles

Health insurance premiums may make up a significant portion of your budget. How can you find more affordable health insurance? Is it ever worth going...

Articles

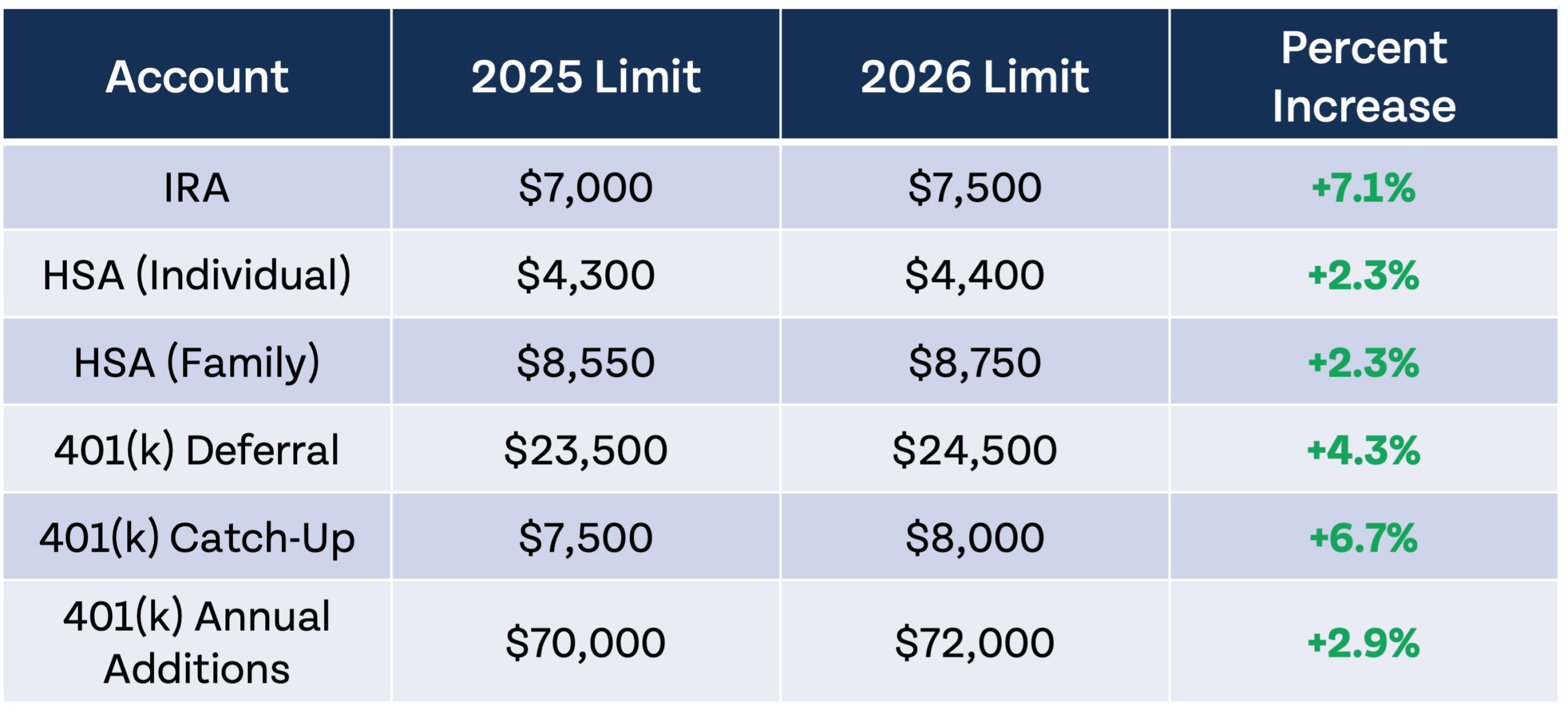

Each year, the IRS adjusts retirement account contribution limits, standard deductions, marginal tax rate brackets, and more for inflation. I’m happy to announce that it...

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

What do real millionaires actually do with their money? We're back with our annual classic where we break down real data from our Abound Wealth...

Episodes

Hidden fees, forgotten accounts, and a Roth surprise could be costing you trillions in retirement. Bo breaks down five 401(k) truths and what you can...

Episodes

Free money AND financial wisdom? We break down how $1,000 compounds over time and answer your money questions with the opportunity to win $1,000!

Subscribe to our free weekly newsletter by entering your email address below.