-

▼

-

▼

What’s a better way to build wealth across every decade of your life? The answer comes down to three tax buckets and knowing which one to fill first. We walk through the tax-free, tax-deferred, and after-tax buckets and show you exactly how to use them at every age and stage. We follow Manny the Mutant from age 25 to retirement at 65, watching a $50,000 salary and a 25% savings rate grow into lasting wealth, with the majority sitting in a tax-free account. Whether you’re just starting out or entering your peak earning years, this episode will show you how the Financial Order of Operations can turn actionable insights into wealth that lasts.

Enjoy the Show?

Where You Can Watch and Listen:

Subscribe on these platforms or wherever you listen to podcasts! Turn on notifications to keep up with our new content, including:

- Episodes of The Money Guy Show every Friday

- Episodes of Making a Millionaire every other Monday

- Mini-shows every Wednesday

- Ask Money Guy Livestreams every Tuesday

- Tons of other fun content!

Introduction – The Three Tax Bucket Strategy (0:00)

Brian: So, here’s what you need to do. Grab yourself a bucket, maybe three, because on this show, we’re talking about the tax bucket strategy.

Bo: And Brian, I am so excited because today we get to talk about a wealth building strategy that not only gives you guidance on where to deploy your next dollar today, but it has massive compounding effects that will likely be felt throughout your entire retirement.

Brian: So, I’m Brian. This is Bo, and we’re financial advisors here to walk you through the three bucket strategy by age. With that, let’s dive right in.

Bo: So, Brian, there are really three different distinct tax buckets that you can put money into and pull money out of when it comes to building towards financial independence. Those are the tax-free bucket, which are like your Roth accounts or your health savings accounts. The tax deferred bucket, which is like your pre-tax 401(k), IRAs, other employer sponsored retirement plans. And then there’s the after tax bucket. Those are like your after-tax brokerage accounts or trust accounts. And each of those buckets works a little bit differently, but I would argue they’re all pretty important when it comes to building your financial life.

Brian: You know, our favorite tradition is actually doing and preparing a net worth statement. Good news for you. If you use our net worth tool, if you go to learn.moneyguy.com, you can get your own. And that’s the exact same net worth tool that we use for ourselves. You actually, we track the three-bucket strategy right there. And this is what I love about this is this is going to, as you know, we have built the financial order of operations so you know what to do with your next dollar. Guess what? The financial order of operations has the three bucket strategy built into it, but that doesn’t mean you’re off the hook because 20 year olds, you look at this differently than 30, 40, or even 50 year olds. So, we’ve built that into today’s show.

Meet Manny the Mutant – Our Case Study (1:54)

Bo: So, what we’re going to talk about is what you should be thinking about at each age and stage as it relates to these three distinct tax buckets. And to do that, we are going to use a case study to kind of build throughout each of these decades. We’re going to start with our favorite financial mutant. We’re going to start with Manny. And let me lay sort of the groundwork for who Manny is and what this illustration is going to walk through. We’re going to assume that Manny starts investing 25% of his gross income starting at age 25 and he does it all the way until age 65. We’re going to assume that starting at 25, his salary is $50,000 a year and he gets an annual raise of 5%. He is also a true blue financial mutant. He’s going to follow the FOO. He gets an employer match on his retirement plan contributions where if he puts in 6% he gets an employer match of 3%. Manny’s going to prioritize the Roth 401(k) over the pre-tax until his combined marginal tax rate crosses from 25% over 30%. So he’s going to do Roth, Roth, Roth and then he’ll switch to pre-tax and we’re going to assume that he can use the backdoor Roth strategy but he does not have the ability to do mega backdoor. So he’s going to start pretty simple. Complexity is going to find him and he is going to follow the financial order of operations all the way from age 25 to age 65.

Brian: There is one more key thing that we use as an assumption. We used, his rate of return is going to change by year. For when he’s 25 years of age, it’s going to be 9.5%. But every year he ages, it’s going to drop down by .1%. For example, when he’s 30, it’s going to be 9%. When he’s 40, it’s going to drop all the way down to 8% and so on. You’re catching on all the way until you retire, which is 5.5%.

Bo: And remember, he’s a financial mutant. So, the fact that he’s saving 25% now for the future lets you know he already has a fully funded emergency fund. He has no high-interest debt. He’s done the things that he’s supposed to be doing to be able to be at the place where he can start building towards his great big beautiful tomorrow.

Brian: I know we’re about to jump into the 20s, but I think it’s worth repeating that because you’re going to see, because this is tax favored the way the financial order of operations, he is going to have access to liquidity because of what you already said. That emergency fund is going to be the margin in case life happens for that reason.

Your 20s – Tax-Free Bucket Takes Center Stage (4:21)

Bo: So, let’s start at the very beginning. In your 20s, likely the bucket that’s going to get the most attention, the one that’s going to get the most love and the most resources pushed towards it is your tax-free bucket. And this is an exciting decade for retirement because in your 20s, these dollars that you save at the beginning of your journey will likely be the most valuable dollars that you have in your entire army of dollar bills when you get to retirement. So, as we think about that tax-free bucket, we want you contributing to a Roth IRA, even if you cannot max it out yet, we want you to think, okay, I’ve already gotten the employer match. I’m now in step five. Brian, will you hold the thing up for me? I’m now in step five of the financial order of operations. I’m going to start doing something, just something into my Roth IRA.

Brian: Well, I even think because we think about this, we know step two is getting that free employer matching. You already shared Manny the Mutant is going to get, he puts in 6% he’s going to get 3%. So he’s going to put 6% in. You can choose. The majority of the plans out there actually allow you to choose Roth contributions. So I think it’s important. Let’s level set. Why do we love Roth accounts? We actually created a slide so you could see all the things we love about Roth accounts. And a lot of times we like the low fees and expenses especially if you’re using the Vanguards, the Schwabs, the Fidelities because we’re big index investors. We love the tax-free growth and then not only the tax-free growth but the tax-free distributions. You can potentially be a 7 figure tax-free millionaire. And then a lot of people when you’re dealing with Roth IRAs and then hopefully with even your Roth 401(k), large selection of investments. If you don’t have a large selection of investments in your 401(k) you might want to talk to your plan administrator or HR. And then I like that we have flexibility with the contributions.

Bo: Yeah, with a Roth IRA, one of the lesser known little tricks about a Roth is that you can always get access to your contributions tax-free, penalty free. Now, we never want you to do that, but it is something you should know about. It’s one of the reasons why if you’re trying to decide, do I prioritize the Roth 401(k) or the Roth IRA, oftentimes we’ll err towards the Roth IRA after you’ve gotten your employer match because there is that break glass in case of emergency provision. So, those are your Roth accounts, but Roth accounts are not the only tax-free accounts that you might have access to in your 20s. You might also have access to a health savings account, assuming that you’re covered under a high deductible health plan through your health insurance.

Brian: Now, look, we love Roth, but the health savings account is pretty magical because guess what? It offers triple tax advantage. There’s actually a quattro potential opportunity as well. And what do I mean when I say triple tax advantage? Look, with Roth IRAs, Roth 401(k)s, the big trade-off is yes, you get tax-free growth, but you don’t get a deduction on the front end. Guess what? With health savings accounts, even your contributions create a tax deduction for you. That’s pretty powerful. Second, they grow tax deferred, meaning as the investments, assuming you don’t just use it as a clearing account, if you put your money into a health savings account and then even invest that money into the health savings account, it grows tax deferred. And then if you use it for qualified medical expenses, you get to pull it out completely tax-free.

Bo: But wait, there’s more. There’s actually a fourth advantage that if your employer allows you to deduct your HSA contributions from your paycheck, you may even be able to have contributions that are exempt from payroll taxes. So, there are four distinct tax advantages to the HSA. So, if you’re in your 20s and you have access to a high deductible plan, we love the idea of you taking advantage of HSA and we also love the idea of you contributing to your Roth IRA. For most people, this is where the majority of your savings is going to happen inside of your 20s. What’s likely not going to happen is a ton of tax deferred savings, except for remember if you’re following the financial order of operations and step two is employer match. Your employer match is likely going to come into the pre-tax side of your 401(k). So, that bucket may not be growing a ton at this stage, but that’s okay. It is still growing and there are still dollars going into it.

Brian: Yeah, this is one. Now, look, it’s a change. I mean, there’s been tax legislation that even this could be Roth down the road, but still for the majority of you out there, you’re going to see that your employer match is in traditional tax deferred type of accounts. But I don’t want you to feel like you’re pressuring yourself because like I said, there’s a time and a place. That’s what I love about the Financial Order of Operations. We’re going to be loading up a lot of that tax-free account. The tax deferreds are going to get a little love. Then you notice, hey, there’s a third bucket. This is the after tax. And that’s why I want to remind everybody, you have emergency reserves that are outside of this, but we’re not going to be giving a lot of love on after tax because that’s really going to start building when you get to step seven of the Financial Order of Operations.

Bo: And don’t allow yourself to go out of order of the Financial Order of Operations. It becomes so enticing. Oh, I’m going to go open that Robinhood account or I’m going to go open that brokerage account. I’m going to start playing with individual stocks. Be very careful. We believe that there is a better way to do money. If you don’t believe us, go to moneyguy.com/resources. Download your free copy of the financial order of operations and make sure you use it as a guide to make sure your dollars are going in the places where they should be going.

Manny’s Results at Age 29 (9:49)

Bo: So, Brian, let’s go back and check out our case study. Let’s see how Manny is doing. And as a reminder, these are the assumptions we’re using. Manny starts investing 25% at age 25. He makes $50,000 a year. He gets a 5% annual pay raise. He follows the FOO. He gets an employer match where he puts in 6% and his employer matches 3%. So where is he at the end of this decade? Well, you can see his portfolio because he’s been diligently saving from age 25 to 29 is now worth almost $91,000 with the vast majority of that being in the tax-free bucket.

Brian: Yeah, it’s kind of amazing if you think about, we always say let’s give you a check number to look for because you really haven’t had a lot of time to start building wealth. And by the time you’re 30 you’d like to have one times your income. Well, if you look at Manny the Mutant, his income as he closes out this decade is right there a little under $61,000. But yet his investments, $80,000 in the tax-free bucket, close to $11,000 in that tax deferred because of all the employer contributions. He’s got one and a half, $81,000 worth of assets that are working for you. And he’s only been working for four years. This is pretty exciting territory if you are a financial mutant.

Bo: So, when you think about some of his benchmarks that he’s hit, he’s getting his employer match. He’s maxing out his Roth IRA, and he’s almost maxing out his HSA. Other than money contributed by his employer, there’s nothing going into the tax deferred account. So, all of his money is going into the tax-free accounts. And even though he didn’t start investing until 25, you know, he didn’t start at age 18. He didn’t start at age 20. He didn’t even start at age 22 when most people graduate because he had to knock out those first few steps in the financial order of operations. Even starting at 25, just four years into his journey, he is an average accumulator of wealth. As a reminder, the way we want you to calculate this, you take your age times your income, divide it by 10 plus the number of years until you’re 40. If you do this for Manny, you can see he’s already an average accumulator of wealth, well on his way to becoming a prodigious accumulator of wealth.

Brian: And the goal is to hopefully get you to prodigious accumulator, which means you’re two times that calculation that you just shared. But well done, Manny. I mean, you got to think about this. Crossing over the average accumulator of wealth in the first few years shows that discipline was doing a lot of work as Manny was building this journey. And I’m so excited because he is well on his way to becoming a 7 figure tax-free millionaire.

Your 30s – Navigating the Messy Middle (12:24)

Bo: All right, Brian. Now, let’s talk about the next stage. Let’s talk about what the three buckets look like in the 30s. And for most folks, the 30s are a unique time because this is likely when you are either in or might be entering into the messy middle. This is a financial stage where life looks a little bit different. All of a sudden, you have neither disposable income left over nor disposable time. You feel like you’re being stretched a thousand different directions in a thousand different ways. And it’s hard just to make sure that you’re doing the things you’re supposed to be doing from a financial planning standpoint, those commitments because you think about all the things with the family planning, the buying the house, you’re going to feel somewhat overwhelmed.

Brian: And look, we are an optimist type. We give optimistic advice, but I think it’s important to show these stages of life so that you can know that you’re not having to face this alone. We’re all in this together. A lot of other people, you’re not unique. A lot of other people have gone through the exact same messy middle journey. Stick with it. Don’t let this serve as a distraction where you say, you know what, I can let my foot off of discipline. I can quit worrying about margin because it’s okay just to give in. No, I want you to stay the course. Know it’s going to be hard. Yes, the days are long, but I promise you the years are short. Respect the FOO, and you will come out the other end that much better.

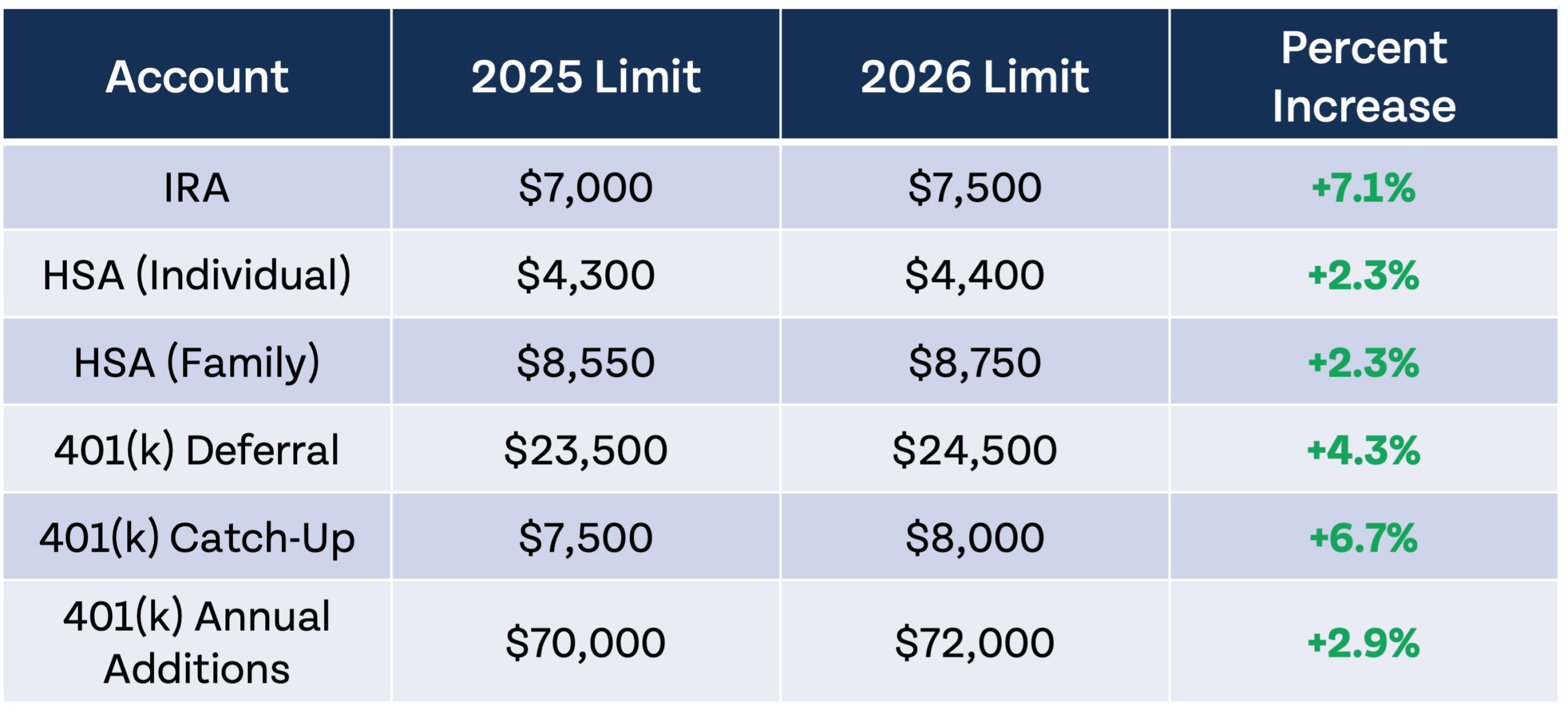

Bo: And so, if you can keep your focus, if you can continue to keep your eyes on what you’re supposed to be doing, there are things you can be thinking about as you are thinking through your tax buckets in the 30s. One of the unique things that might be happening is as you get into your 30s, as you get into some of the better earning part of your career, you may no longer be eligible to make direct contributions to a Roth IRA. The income phase outs in 2026 are $153,000 to $168,000 for a single person or for married filing jointly, it’s $242,000 to $252,000. If you make over those income thresholds, you no longer can contribute directly to a Roth IRA. But assuming your account structure will allow you, meaning you don’t have any other outside IRA assets, you can do backdoor Roth IRA contributions where you contribute to a non-deductible traditional IRA. You then convert that money to Roth and you have thus put $7,500 in your tax-free account. And that’s exactly what we’re going to be doing for Manny in the case study.

Brian: Well, and also this might be the decade, especially in your latter 30s when, as you said, you start getting some traction on your career. If you blow through the tax rates, it might make sense to transition from making Roth contributions on your employer plan to traditional. More to come on that, but it’s definitely important. And then the other thing that’s life planning wise, when you think about tax-free accounts, we think about those health savings accounts. We love the health savings accounts, but remember you have to have access to a high deductible health plan. Well, when you’re looking at your employer benefits when it’s open enrollment time, if you know you’re doing family planning, like you’re going to have a kid this year or you have other things coming your way, it might make sense to hit the pause button on that high deductible plan and also the health savings account and go with the Cadillac options of a PPO or other things. Make sure you’re not skipping that financial mutant step of looking at your health insurance options and choosing what fits in this upcoming year.

Bo: Yeah. Even though we love the tax benefits of the HSA, we don’t want to let the tax tail wag the financial planning dog. We want to make sure that we’re still making the most sound decisions available, even if it means walking away from a specific tax benefit. Now, Brian, you’ve already alluded to this. One of the things that might also be changing in your 30s is that your tax deferred bucket might become a bigger planning tool where in your 20s and you were in a lower tax bracket and it made tons of sense to go Roth, Roth, Roth, tax-free, tax-free, tax-free. As you get into your 30s and as your income increases, now you may want to consider pre-tax 401(k) contributions. If you’re someone whose marginal tax bracket, when you add up your marginal federal and marginal state bracket is greater than 30%, every dollar that you put into the 401(k) on the pre-tax side could save you 30 cents in taxes. You can think about that like a 30% imputed rate of return. That becomes so attractive of a benefit that it’s difficult to walk away from. So, you’re going to want to make sure that you reassess this in your 30s to make sure that you are putting your money when it relates to your 401(k) in the right tax bucket.

Brian: And then that last tax bucket is the after tax. Now, look, I don’t want you to get discouraged. This one might not get filled up, but it might have a little bit. You might actually get a piece of this in your late 30s because remember to get beyond into the after tax, you need to be having a savings and investment rate that’s exceeding 25% and you need to build this up. That’s not going to be the easiest thing to accomplish, but you might catch a portion of it right here in the after tax. More to come on that as you’re going through. And it’s okay if you don’t reach this bucket in your 30s. There’s going to be time in your 40s. That’s when I think you’re going to see we catch a lot of traction, start thinking about what does it look like when we retire, and that three bucket strategy really starts to focus on filling all three buckets up.

Manny’s Results at Age 39 (17:42)

Bo: Okay, so let’s check in with Manny and see where he’s at. As a reminder, Manny started investing at 25, saving 25% of his gross income. His salary when he started was $50,000 and he’s gotten a 5% pay raise every year. He follows the financial order of operations and if he puts in 6% to his 401(k), his employer will match 3%. So when we check in here at the end of the 30s, he has now through consistent and disciplined saving accumulated a portfolio of almost $530,000.

Brian: Do you see the magic of compounding growth? And then just being consistent early and often really does create a reward. Because here’s somebody that their income is right under six figures, $98,997, but they have investable assets that are right under $530,000. Now, look, yes, $466,000 is in those tax-free buckets. Oh, whoa, that is going to be awesome down the road as compounding growth keeps building. And then, yes, those employer match contributions are going to be a little under $64,000. Still impressive. Early and often wins.

Bo: Yeah. And what’s wild is if you think about his income, he started at $50,000. He’s gotten these pay raises. His income by the end of his 30s is right at $99,000, almost $100,000. And you know, when we think about our checkpoints, by the time you get to 40, we want you to have three times your annual income saved in investments. So for Manny, that’d be $300,000. You can see he is now well above that. He’s maxing out his Roth IRA. He’s maxing out his HSA. And he’s contributed even more to his Roth 401(k) now. So, he’s not quite maxing it out, but he is rapidly approaching hyper-accumulation. He’s still not yet hit the tax bracket where it makes sense for him to shift into pre-tax, but that’s okay. Those dollars are still going to be growing based on the employer match. And then now, he is beginning to get close to being a prodigious accumulator of wealth. That’s when you take your age times your income. And when you’re 40, you just divide by 10. You can see that where he started the decade with a portfolio of just over $90,000, as he closes out the decade, he has almost $530,000 saved up.

Brian: Powerful decade. I mean, a five-fold increase is just wowzer. You can start to see that discipline, giving yourself the margin of living on less than you make and just giving it that component of time really is powerful in the long term.

Your 40s – When It All Comes Together (20:13)

Bo: All right, Brian, let’s talk about this next decade. And this one’s interesting because this is one you’ve talked about and I think I’ve heard you say this. This is probably the first decade where it didn’t feel like you were just trying to make ends meet.

Brian: Yeah. This is when it all comes together because I mean you suffered in your 20s. You typically are not in your peak earning years. You’re not making a lot of money. Your 30s, then the messy middle kicks in and then your 40s, you’re like holy cow, wait a minute, there’s not as many distractions. Yes, you have kids and stuff but you’re also in peak earning years. It starts coming together. This is the one, if you’ve done everything you were supposed to earlier, you’re really starting to feel like you’re getting dividends from that early discipline. It pays off. But here’s the good news. Also, if you’re kind of a late bloomer, 40s still has a lot of oomph on the compounding growth opportunities that if you’re playing catch-up, this is your moment as well.

Bo: Well, and as you think about your tax buckets, if you’ve been doing what you’re supposed to be doing in your 20s and 30s, there’s a really good chance that your tax-free bucket’s kind of locked in now. You know if you should be doing a Roth IRA, you know if you should be doing a backdoor, you know if the high deductible plan is what makes the most sense for you. You’ve kind of got those pieces figured out. But one thing we do want to do is we want you to reassess when it comes to your 401(k) contributions every year when you go through open enrollment or before you get into the new year. I just want you to think through should I be doing Roth 401(k) or should I be doing pre-tax? Likely the other tax-free numbers are going to stay locked in. IRAs are going to get maxed out. HSA is going to be maxed out. But you may now in the 40s be making that shift from Roth contributions to pre-tax. We want to make sure you’re thinking through that.

Brian: And then let’s talk about the tax deferred account. Now remember, this is an account that’s primarily been funded through just your employer contributions. Then as your income went up, yes, you exceeded that 30% marginal rate between your federal and state, you started making pre-tax. But there is a dance that comes here is that I want you to realize that I don’t want you to be retirement rich, life poor because at this stage I’d love for you to be paying cash for cars and other things because you’ve been around the block long enough. You don’t need to be running up mindless debt for just lifestyle and then you find out that now yeah the tax savings with the financial order of operations was great but this is the time by the time you reach step seven of the financial order of operations. Let’s start thinking about how we’re actually going to use this money not only for retirement but right now for those big purchases like cars and so forth. I would like to start seeing some traction in your 40s where after tax accounts are going to start showing up because they provide a bridge of liquidity especially if you’re retiring early and they also provide just early access for lifestyle and for those people who need to retire and get access to money. This is going to be your bucket.

Bo: Yeah. And in your 20s and 30s, it’s about save, save, save, accumulate, accumulate, accumulate. As you get into your 40s now, you want to begin thinking about how am I going to use these dollars? When am I going to use these dollars? And what am I going to be using these dollars for? And the answer to those questions are the things that will dictate the way you want to think about your savings.

Manny’s Results at Age 49 (23:16)

Bo: So, when we come back to Manny, as a reminder, he started saving at age 25, saving 25% of his gross income, making $50,000 a year, getting a 5% annual increase, following the financial order of operations, and still getting his 3% employer match if he put in 6%. Well, he’s done that through the decade of the 20s. He’s done that through the decade of the 30s. And now, it’s pretty remarkable. He’s done it through the decade of the 40s. So, he’s gone for 25 years now. And as he closes out this decade, his portfolio is now worth almost $1.7 million. He is now officially in the two comma, almost multiple million club.

Brian: And look at his income is $161,000. I did think it was interesting. Tax-free is almost a million and a half dollars. The tax deferred which is primarily the employer and then the portion when he switched once he was over greater than 30%. But it’s a little under $200,000. There’s only a sliver of the after tax. He barely touched it. Like $7,000, $6,700 actually showed up in the after tax. I’m curious to see what happens in the decade of 50s and beyond because we’re really going to be loading up that after tax bucket because he’s going to want to land the plane of retirement and have access to that bridge account. It’s going to be interesting to see how it plays out, but well done on the 40s of following the FOO to a tee and building up 7 figure tax-free assets as a financial mutant.

Bo: Yeah, when you think about his personal financial order of operations, he’s maxing out his Roth IRA. He’s maxing out his HSA. He’s maxing out his 401(k). And now he’s in that hyper accumulation phase where he’s starting to save to the after tax account. Based on his tax rates, he’s still prioritizing Roth over pre-tax since when you look at it, his combined marginal rate is still 24%. So, it still makes sense for him to focus on the Roth. That’s all employer money that’s going into the pre-tax. And so, now when we look at, he is now officially and effectively a prodigious accumulator of wealth. Brian, we talked about this pre-show where you said, “Hey, most millionaires, they hit millionaire status around age 47 to 49, somewhere in that ballpark, usually inside of their 401(k).” Well, Manny is a shining example of that exact thing happening. You can see that he is now a prodigious accumulator of wealth that hit millionaire status inside of his 40s. And now here he is at the end of this decade with a portfolio of almost $1.7 million. He’s now at the point where now he gets to start talking about what do I want the rest of my life to look like?

Brian: I still think if you look at this journey and we covered it when he was approaching the 40s, he was a little over $500,000 of assets, but here he is closing out his 40s, soon to be 50, and he’s got close to $1.7 million of assets. He’s not done yet either. That’s wild. That shows you the power of compounding is that we have gone from $500,000 to close to $1.7 million in that decade. You’re seeing some really powerful stuff. And then if you start thinking about what this money can do for you in the future, you’re now well beyond the point where your money is working just as hard as you. But the job is not done. This is going to be exciting to talk about the 50s and beyond where we bring this plane down for a landing to live your best retirement life. Let’s see how this develops.

Your 50s and Beyond – Fine-Tuning Your Plan (26:50)

Bo: Yeah. At this stage, you’re beginning to now fine-tune. You want to fine-tune not just a generalized plan, but your specific plan. And what’s interesting is that we talk to retirees and folks in financial independence, they always tell us as it relates to the tax-free bucket, I always wish I had more. I wish this bucket was bigger. I wish I would have started sooner. So, one of the things we want you thinking about in your 50s, okay, are there ways from a tax efficient standpoint that might make sense for me to begin increasing this bucket? Should I begin looking at actual Roth conversions if I’m someone that’s going to retire early? Maybe based on my unique plan and what I’m trying to do, maybe even though I received the tax benefit in my 30s and 40s, now I want to switch to Roth contributions because it makes sense. We want you to make sure that you’re thinking through, okay, what is the ultimate use of these dollars going to be and how do I need to fine-tune my plan in this last decade of accumulation?

Brian: I want you to even look at the tax rate as you enter retirement because you might want to choose that yes, your combined marginal rate puts you in the point where you ought to do traditional because we know we’re going to be able to flip the switch to a much lower tax rate as we go through the threshold of retirement. And that’s going to directly impact that tax deferred account because this account has probably hit critical mass from the standpoint we’re trying to figure out now how we’re going to get those assets out. Just like you talked about, this is going to be prime category for Roth conversions, especially if you’re part of the FIRE/FINE movement where you’re moving on to that next endeavor and your earned income drops drastically as you are approaching retirement.

Bo: But as it relates to this tax deferred bucket, you do need to recognize in your 50s, this is expensive money to access. If you try to pull it out before 55 from your 401(k), you’re going to get hit with ordinary income taxes and a 10% penalty. If you try to pull out of IRAs before 59 and a half, you’re going to get hit. You have to make sure you wait till after age 59 and a half to access these dollars. And even then, the pre-tax bucket you still have to pay ordinary income tax on. So, you want to make sure you’re factoring that in when it comes to, okay, I’m going to retire. Where am I going to pull the money out of? Which buckets am I going to deplete first? And what you may find in those early years of retirement, this is where the after-tax bucket can be so valuable.

Brian: Yeah. And I love, I love this as an accounting term. And we put this into the way we wrote it. We call it a LIFO method. Is that you’re going to find the last thing we filled up was the after tax. So it’s last in but it’s first out. And if you think about what has been the history of what we’ve tried to do on accumulation is that we funded the Roth accounts first. They also were slightly being funded with the pre-tax because of that employer match and then the last account to get filled was the after-tax. That was the bridge account. But guess what? In retirement, we’re going to do it in the exact opposite way. We’re going to do de-accumulation. And we’re going to go through after tax first, then we’re going to touch the pre-tax. Hopefully, we can do enough Roth conversions and be very optimized with the way we do the tax rates that that doesn’t even have a lot of pain. The last bucket you’re going to want to touch, what’s the first that you funded, the Roth, because these things not only are tax-free growth, they’re great legacy building opportunities for what you want to pass on to your heirs.

Manny’s Final Results at Age 65 (30:00)

Bo: All right, so let’s see where Manny is at retirement at age 65. Remember, he started saving at 25, saving 25% of his gross income. He had a $50,000 salary where he got 5% annual pay raises. He follows the financial order of operations. He had an employer match the whole time. Well, when you look at his three buckets, Manny has a huge portfolio now. He has a portfolio worth almost $6.4 million. $4.6 million of that is in tax-free. A little over a million dollars is in pre-tax. And he has $635,000 in his after tax bucket. Now, when you look at his income, his income is at $352,000. You may say, “Guys, that’s unreasonable. That doesn’t make sense. That’s too high of an income.” Remember, this is 40 years in the future. And so, we brought this back to current dollars. This is someone who started their career at 25, making $50,000 in today’s dollars. And you fast forward 40 years into the future, it’d be the equivalent of someone making $107,000 at the end of their career. That does not seem crazy to us. $50,000 beginning of the career, $107,000 end of the career. That seems very, very reasonable.

Brian: This also should wake you up to the fact that because of inflation and other things, you need compounding growth to work for you because it’s going to be expensive to let your army of dollar bills replace your brain, your back, and your hands. Get to it because this is what’s powerful if you can just set it and forget it. Slow and steady wins the race. And it’s amazing because we started off pretty reasonable there. $50,000 a year with decent but modest pay raises. You can do this, guys. It’s pretty amazing to look at what the journey to retirement looks like. And I want to encourage you all if you look at what happened from age 50 to age 65, what was actually going on in the background as we start talking about safe withdrawal rates and what can this produce for the future.

Bo: Yeah. So, as Manny sits here at 65 with this $6.4 million portfolio, he now has enough to replace 72% of his final salary with a 4% withdrawal rate. Incredible. If he had a 4.5% withdrawal rate, he could replace 81% of his pre-retirement income. If we factor in social security, which will likely be there for Manny that he’ll be able to pull off of, well, now with a 4% withdrawal rate, he could replace 98% of his pre-retirement income. Not pre-retirement expenses, pre-retirement income. That means that likely because he was such a diligent saver, when he retires, he actually gets a pay raise. He gets to increase his standard of living. Or if he had a 4.5% withdrawal rate, it would be 107% of his pre-retirement income. The vast majority of his assets are tax-free. So that means when he goes to pull out his money, he gets to choose what his tax rate is. He gets to efficiently and effectively manipulate the tax code to pull out the money that he wants without losing a ton of it to taxes. And he was already at this point, but Manny is indeed a prodigious accumulator of wealth. To remind you, he started at age 49, the beginning of this final phase with a little over a million and a half dollars. And as he continued to work hard from 49 all the way to 65, he now enters financial independence with almost $6.5 million dollars saved up.

Keys to Manny’s Success (33:19)

Brian: So I think as we close out, it’s important to talk about what were the key elements of success for Manny. I mean look, don’t sleep on the discipline. Manny had margin. He lived below what he made his entire career. And that margin has shown up in now his net worth statement. It’s not just what he made, it’s what he owns. And that’s a powerful tool that you can also work to your favor as well.

Bo: He also started early. The earlier you start, the better. The absolute best time to start investing was yesterday, which makes today the second best. He started at 25. If you’re not 25 yet, that’s okay. Start today and your future self will thank you.

Brian: And then he had a better mousetrap. I mean, we believe that there is a better way to do money and that’s what the financial order of operations can do for you. But don’t fall in the trap of thinking a lot of people think it’s just going to be a walk up the mountain with all the stairs of life. But no, we know that the FOO is an all-terrain vehicle, all season type system to where no matter what life throws at you, it’s going to have some ups and downs and you’re going to have step backs, you’re going to have step forwards. We’re going to be there with you. That’s why we created the Financial Order of Operations. It’s not only tax optimized, it’s life optimized because it’s there for you no matter what’s going on. We’d encourage you, look, if you’re just starting out and you just want to get inspired on what to do, go check out our resources at moneyguy.com/resources. We will help you accelerate your journey to building success. But here’s the catch. When you reach success, you’ll realize no matter how simple you want your financial life, complexity will be waiting for you. And when you create a complex life through success, that’s when you’re going to say, “Hey man, I don’t know what I don’t know. What am I going to do?” We’re going to leave the porch light on for you. We work with clients all across the country. We’d encourage you and invite you to go to moneyguy.com. Check out the become a client section and we’ll be waiting for you. I’m your host, Brian, joined by Mr. Bo, Money Guy team out.

Free Resources

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Articles

Articles

The Best Tools for Filing Your Taxes in 2026

Have you filed your taxes yet? You still have ample time left until the April 15th deadline, but it’s probably best not to procrastinate too...

Articles

6 Financial Changes To Make in 2026

There is no need to wait until an arbitrary date on a calendar to make positive changes in your financial life, but if you are...

Articles

The IRS Just Announced 2026 Tax Changes!

Each year, the IRS adjusts retirement account contribution limits, standard deductions, marginal tax rate brackets, and more for inflation. I’m happy to announce that it...

Financial FAQs

Courses & Tools

How about more sense and more money?

Check for blindspots and shift into the financial fast-lane. Join a community of like minded Financial Mutants as we accelerate our wealth building process and have fun while doing it.

Free Resources

Financial Order of Operations®: Maximize Your Army of Dollar Bills!

Here are the 9 steps you’ve been waiting for Building wealth is simple when you know what to do and the order in which to...

Free Resources

Wealth Multiplier By Age

If you want to set yourself up for future success, find out how much you need to save every month to become a millionaire.

Free Resources

Car Buying Checklist

Here’s how you can buy a dependable car that won’t break the bank. Our free checklist walks you through the 20/3/8 rule and strategies to...

Recent Episodes

It's like finding some change in the couch cushions.

Watch or listen every week to learn and apply financial strategies to grow your wealth and live your best life.

Episodes

We Changed The 4% Rule!?

Retirement planning isn't as simple as following the classic 4% rule anymore. In this Live Q&A, we explain why the traditional retirement withdrawal strategy deserves...

Episodes

Is Aggressive Saving Derailing Their Short Term Goals?

High earners in their mid-twenties, cash poor, and a wedding 12 months away. In this episode of Making a Millionaire, we show Joey and Leah...

Episodes

Why This Money Advice Has EXPIRED

Traditional financial advice isn't always wrong, but some money rules simply haven't kept up with today's economy. In this episode, we reveal which classic money...